1/n long thread on Inside India's retail credit boom. The good, bad & ugly. My deep dive in @EconomicTimes @Magazin_ET Some imp takeaway. @kunalb11 @Gaurav1105 @desaisantosh @CRISILLimited @CIBIL_Official @RajeshMagow @creditvidya @mrinagarwal @trramach

economictimes.indiatimes.com/industry/banki…

economictimes.indiatimes.com/industry/banki…

A credit-averse nation is falling in love with it. Led by millennials, a generational shift in attitude has intersected with a big digital disruption in lending biz, causing capacity expansion & a drop in costs, allowing firms to bring more people into ambit of formal credit 2/n

Four discernible shifts. Lending is moving online—a person in need of a loan today is far likelier to fill up a form on a website than walk into a bank branch. Secondly, a raft of fintech firms have sprung up, offering convenience in accessing & democratising credit 3/n

4th, demand for secured loans—housing loan, loan against property - r seeing a relative decline even as unsecured credit, like credit cards & personal loans with high rates of interest, is booming. Fifth, demand for credit is increasingly coming from non-metro cities & town 4/n

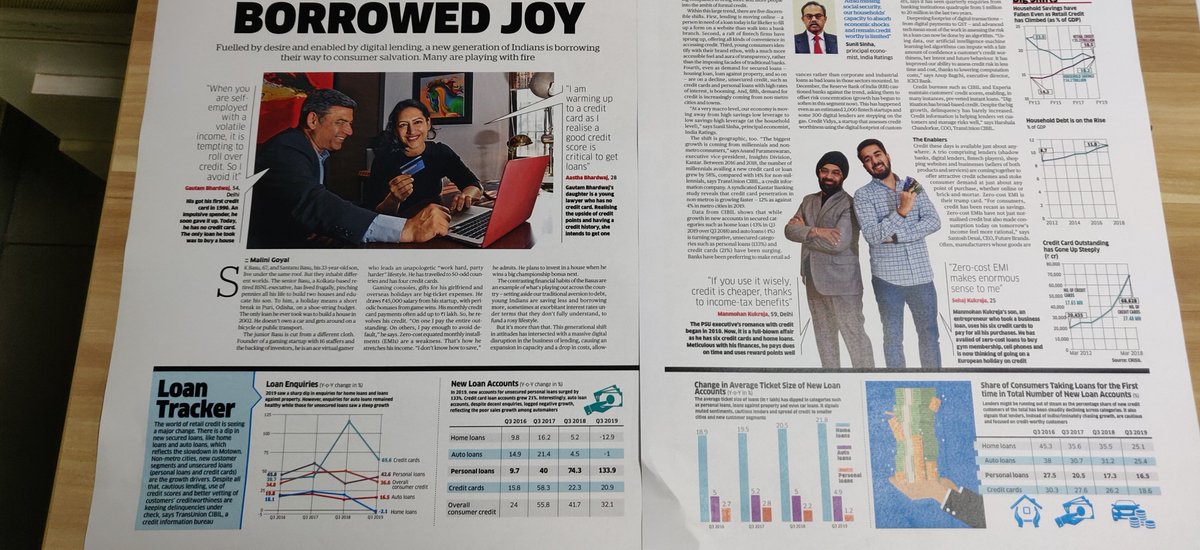

This has some very significant macro economic implications. India's household savings rate as %age of GDP dips, household debt is rising with unsecured loan like that of credit card rising steeply 5/n

Here's granular data frm CIBILTransunion to help understand what's going. Based on enquiries last 4 yrs (Q3) - homeloan dips as auto is ok, credit card & personal loan surges. Mystery is auto enquiries: data does not align with real sales which hav been dipping. But wait..!! 6/n

New loan accounts reveal things better. Home loan & auto loan see -ve growth. Personal loan surges 133%. Credit cards 21% 7/n

What is interesting to note is that average ticket size is coming down across the board, signalling muted sentiments, cautious lenders, spread of credit to smaller cities & new customer segments 8/n

Lenders might be running out of steam as the percentage share of new credit customers to the total has been steadily declining across categories. It also signals that lenders, instead of being indiscriminate chasing growth, are cautious and focused on credit-worthy customer. 9/n

New loan A/c from below-prime custmers is up in unsecured categories like personal loan, thks to big push from fintech & NBFCs. In secured credit categories like home loan, watchful lenders have tightened norms lowering share of BPL customer. Expect NPAs 2 rise in unsecured 10/n

This even as the base of credit-seeking customers in India is expanding briskly, signalling an attitudinal shift towards credit. 11/n

Because of all this, credit is becoming more consumption led in unsecured categories. The balance growth in secured categories like home loan and auto loans is slowing. Unsecured credit card loans and personal loans are growing the fastest 12/n

FOR NOW, cautious lenders & customers’ credit scores is helping keep delinquency range-bound despite big growth. But with whatever conversation i have had so far, with big push by fintech lender, my instinct tells me we hav a ticking unsecure retail credit crisis in works 13/n

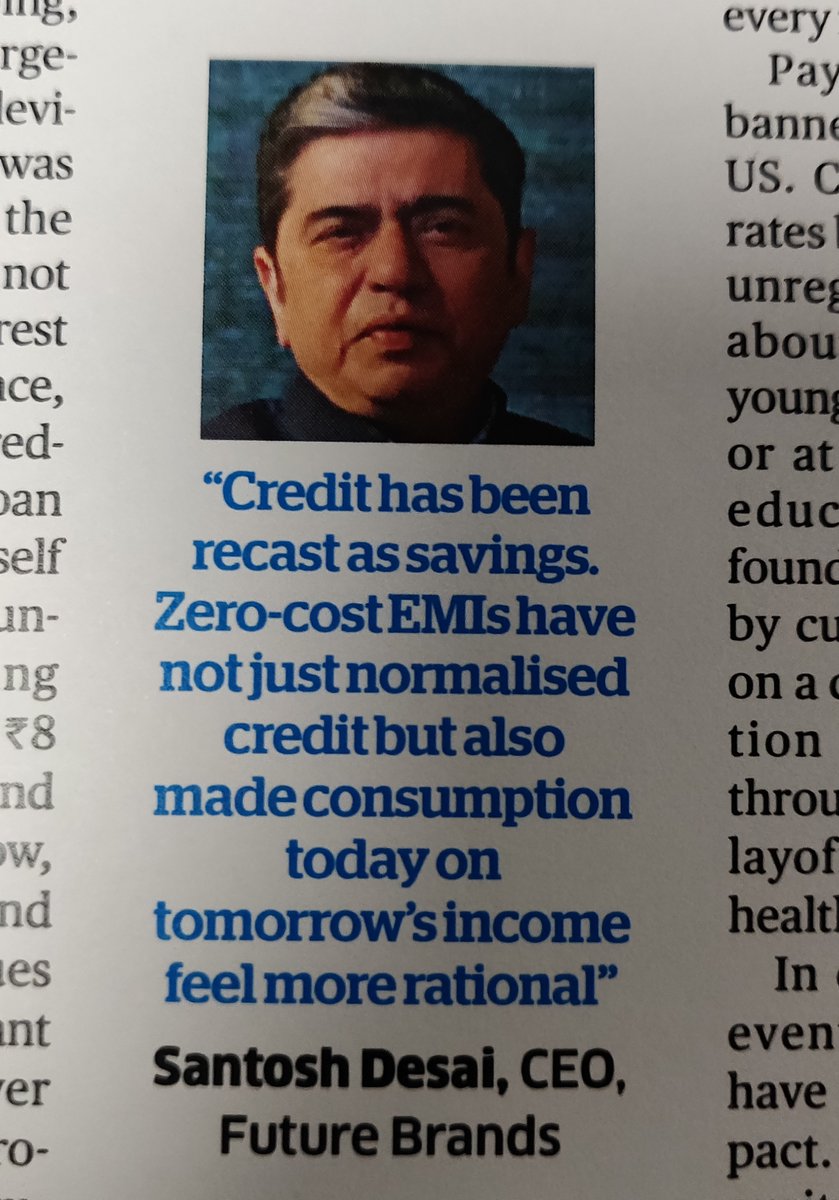

Zero cost EMIs is playing a big catalyst this time. Thanks to etailers like @AmazonindiaIn @Flipkart mfrs like smart phone sellers & NBFCs willing to partner.

Vikas Bansal of Amazon Pay, says: “Zero-cost EMIs is used frequently & has grown five-fold in two years.” 14/n

Vikas Bansal of Amazon Pay, says: “Zero-cost EMIs is used frequently & has grown five-fold in two years.” 14/n

Here's a smattering of a range credit customers who are entering the fray.

Aastha Bhardwaj, 28 - young lawyer does not buy on credit, has no credit card but is slowly warming up to it as she discovers the upside of credit points and having a credit history 15/n

Aastha Bhardwaj, 28 - young lawyer does not buy on credit, has no credit card but is slowly warming up to it as she discovers the upside of credit points and having a credit history 15/n

Kimberley rowe, 25, uses credit card for all her expenses but under the watchful monitoring of her dad who keeps track of expenses, due dates etc. 17/n

But som like Santanu Basu, an avid gamer, is struggling. His life runs on EMIs with 4 credit cards. He spends on overseas holidays, shopping for GF & gaming devices. "I don’t know how to save. To make my salary stretch, I buy on EMIs and revolve credit.” He is candid 18/n

Jahangir Aziz of JP Morgan, makes two imp pts: “In recent times, household credit has risen while it has declined for industry. Granular data is unavailable but I have a feeling consumer loan at least partly is disguised loan to MSMEs.” 19/n

He also makes another imp but unpopular point - He feels that Indian policy makers should rethink being so concerned about lowering savings rate and retail credit expansion. “I don’t agree that savings is good and consumption is bad.” 20/n

Aziz says till about 2012, amid strong global trade, emerging markets like India didn’t have to worry about demand. “They need to now. With weak export market, creating demand boosting consumption will become critical.” 21/n

But he alongside others like Sunil Sinha of India Ratings agree that poor social-economic security in India leaves many vulnerable. 22/n

Dark underbelly: Suddenly, a big population of unbanked and young, with no or limited exposure to formal banking, must learn to use credit products responsibly. Mouth-watering deals, easy credit, eager lenders and discounts clubbed with instant credit can be a perfect trap. 23/n

For many young millennials, debt-led life can often spiral downwards. With low economic growth and fraying social cushion, consumers’ ability to absorb shocks in difficult times will be limited. Expect debt distress to go up. 24/24

Thread ends

Thread ends