So the speedy swap lines did help soften the dollar strength, esp to those that got it. Look at Asian FX vs the USD in a 1 day move.

👏🏻👏🏻👏🏻

Some asked why swap lines matter & why this helped. I'll go through it soon 😎

👏🏻👏🏻👏🏻

Some asked why swap lines matter & why this helped. I'll go through it soon 😎

Statement from the RBA on the swap line (60bn): So the RBA can use AUD to get USD & then the RBA lends to local banks by taking in AUD-denominated securities & LEND USD (at a very good rate as it gets cheap USD supply from the Fed).

This is something I argued in the op ed.

This is something I argued in the op ed.

Key here is that the supply of liquidity the Fed injects is only "beneficial to those w/ access to it." So to overcome the operational & credit liquidity squeeze, the Fed has to up its operational game.

That's what it did last night by giving ACCESS of cheap USD liquidity to RBA

That's what it did last night by giving ACCESS of cheap USD liquidity to RBA

Since the Fed announcement of swap lines:

USD weakens; Risk asset improves a bit; & commodities feel a bit better.

In Asia, it's GREEN & not a blood bath, esp for Australian & Korean assets!!!

USD weakens; Risk asset improves a bit; & commodities feel a bit better.

In Asia, it's GREEN & not a blood bath, esp for Australian & Korean assets!!!

Guys guys, I kept saying to read that paper by the NY Fed & seems u don't so how swap lines work:

*Swaps involve 2 transactions - a foreign central bank (CB) sells domestic FX (RBA selling AUD) to get USD

*The foreign CB has to buy back the AUD at a future date at the same FX😎

*Swaps involve 2 transactions - a foreign central bank (CB) sells domestic FX (RBA selling AUD) to get USD

*The foreign CB has to buy back the AUD at a future date at the same FX😎

* Foreign CB (say RBA) then lend USD to their institutions starving of USD by buying AUD-denominated assets & lend USD at a certain rate.

*Foreign CB decides who gets access & collateral accept.

*Foreign CB has to pay back USD & carry the credit risk of domestic lending of USD!

*Foreign CB decides who gets access & collateral accept.

*Foreign CB has to pay back USD & carry the credit risk of domestic lending of USD!

Fed commits to holding the foreign FX at the foreign CB instead of lending to avoid reverse management issues. So at a future agreed date:

*Foreign CB pays the Fed back the USD w/ interests on the USD borrowed that is usually = to the amt the CB earned on USD lending operations

*Foreign CB pays the Fed back the USD w/ interests on the USD borrowed that is usually = to the amt the CB earned on USD lending operations

Why are swap lines necessary? Technically, CBs should be able to provide USD to funding banks in their system but because they either don't have enough reserves or reserves still not sufficient.

B/c of the role of the dollar in global finance, the Fed's lender of last resort.

B/c of the role of the dollar in global finance, the Fed's lender of last resort.

Also in times of stress, if the foreign CB have to sell their FX to buy USD in the open market, they would crowd out private transactions, making the liquidity stress WORSE as banks liquidity funding worse

Some people asked will the USD liquidity be completely solved by this? No

Some people asked will the USD liquidity be completely solved by this? No

That said, it is NECESSARY, but not SUFFICIENT to get rid of the global shortage - see op ed & research report on Asia dollar shortage on why - because w/o which, foreign CBs can't help their institutions from a massive dollar squeeze.

Fed is a de facto global CB & should lend!

Fed is a de facto global CB & should lend!

A few readings for you (please read primary sources such as the Fed!):

How swap lines work & what the Fed did during GFC:

newyorkfed.org/medialibrary/m…

My op ed to explain what happens to global balance sheets: ft.com/content/37f0e8…

My research on Asia USD. DM if u want access.

How swap lines work & what the Fed did during GFC:

newyorkfed.org/medialibrary/m…

My op ed to explain what happens to global balance sheets: ft.com/content/37f0e8…

My research on Asia USD. DM if u want access.

Thread on why the role of the USD in finance & also the level of leverage we are in caused the violence in markets:

a) Too much leverage in the system, which means deleveraging coming

b) Role of the USD means the Fed has to act like lender of last resort

a) Too much leverage in the system, which means deleveraging coming

b) Role of the USD means the Fed has to act like lender of last resort

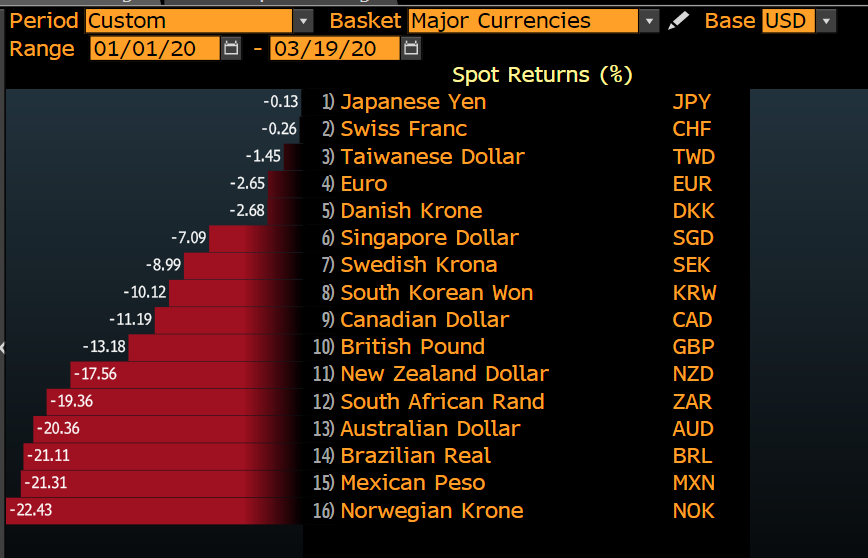

IDR is showing USD liquidity stress & spiking a lot - I lobby for Indonesia to get a swap line as well.

Our analysis shows that Indonesia is amongst the MOST AFFECTED by the dollar credit crunch, according to our analysis (AU, MYR & IDR most affected)

Our analysis shows that Indonesia is amongst the MOST AFFECTED by the dollar credit crunch, according to our analysis (AU, MYR & IDR most affected)

Spread widened in Asia & why the swap lines by the Fed to the BOK, MAS, RBA & RBNZ key to ease the dollar funding market 👇🏻👇🏻👇🏻

AUD/USD jumped almost 4% on that USD swap line w/ the Fed. Longer end of the curve moved lower as well as liquidity improved (note that after the RBA cut rates to 0.25% & did 3y cap of 0.25%, longer end bounced on weak liquidity).

Emerging markets face 3 problems: a) capital flows reversing so those more dependent via current account deficit + high dollar debt most impacted.

In this case, Indonesia tops the vulnerability on foreign capital as equity outflows accelerated 🇮🇩👇🏻

In this case, Indonesia tops the vulnerability on foreign capital as equity outflows accelerated 🇮🇩👇🏻

Another country that is vulnerable is Malaysia, although it has a current account surplus, capital outflows don't help as we need to also talk about the income side.

Look at the liquidation of equities by foreign investors!🇲🇾

Look at the liquidation of equities by foreign investors!🇲🇾

Asia capital outflow sharp (as mentioned, this impacts Indonesia the most given dependency to finance the economy & also high dollar debt)

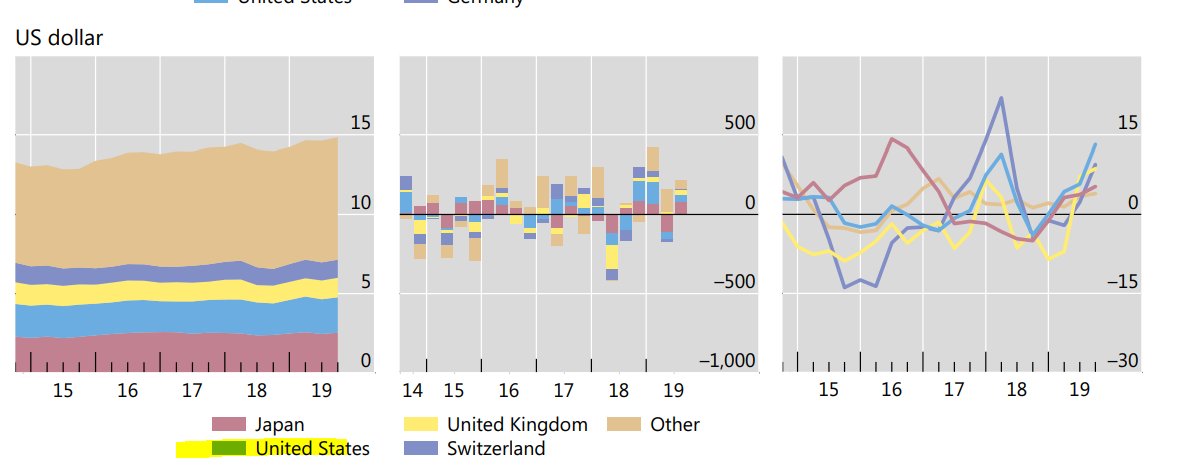

USD debt as a share of GDP (loans + debt securities). Look at the jump by Indonesia & Malaysia in the past five years.

Indonesia has a lot of debt to service (remember that we haven't talked about the income side & only the capital aspect, which is negative)

Indonesia has a lot of debt to service (remember that we haven't talked about the income side & only the capital aspect, which is negative)

So before we talk about income, I want u to know that most trade credit is in USD & trade invoiced in USD. On top of this, Fed low rate policy made it very lucrative to issue in USD & many EM did that, including Indonesia. So now it has a lot of USD debt that it has to service.

Now that u agree w/ me the capital side is bad (think VaR risk models telling people to not take more risk as risk assets falling). Not to mention these funds selling risk asset to cover their losses etc

On the income side (merchandise trade, tourism, remittances) also down but!

On the income side (merchandise trade, tourism, remittances) also down but!

Degree of dependency on income is very diff than the capital side.

What we did was we looked at commodities, intermediates & tourism & remittances.

Malaysia comes out most vulnerable for income (high commodity exposure + intermediate + tourism) & Thailand 2nd b/c of tourism

What we did was we looked at commodities, intermediates & tourism & remittances.

Malaysia comes out most vulnerable for income (high commodity exposure + intermediate + tourism) & Thailand 2nd b/c of tourism

Remittances tend to be sticky vs other income sources like commodity, intermediates & tourism. While the Philippines depend on tourism (Vietnam too), we don't think they are exposed via the downturn of income (meaning USD inflows).

Capital =Indonesia worst

Income =Malaysia worst

Capital =Indonesia worst

Income =Malaysia worst

Why does Australia top our rankings as vulnerable? Well, it's #2 for most vulnerable for capital &vulnerable for income.

Finally, if u look at how wide is the exit door (depth of markets), well, ASEAN bad, esp Malaysia, Vietnam, the Philippines.

Now u see why people want dollar

Finally, if u look at how wide is the exit door (depth of markets), well, ASEAN bad, esp Malaysia, Vietnam, the Philippines.

Now u see why people want dollar

If u want to think in terms of the IMF balance of payment (BOP) perspective, then we got stress in the CAPITAL account (more intense & emergency level & u see more in USD market) & also the INCOME account (trade of services + income)

Now u know why EM Asia needs swap lines🙇🏻♀️🙇🏻♀️🙇🏻♀️

Now u know why EM Asia needs swap lines🙇🏻♀️🙇🏻♀️🙇🏻♀️