#AparIndustries

#Apar Industries is one among the best established companies in India, operating in the diverse fields of #electrical and #metallurgical #engineering.

@Raunak_Bits @Sachsharma12 @srslysaurabh @Agarwal_Ishu @Random_Gyan @drprashantmish6

#Apar Industries is one among the best established companies in India, operating in the diverse fields of #electrical and #metallurgical #engineering.

@Raunak_Bits @Sachsharma12 @srslysaurabh @Agarwal_Ishu @Random_Gyan @drprashantmish6

Raw materials:

Crude #oil & #Steel

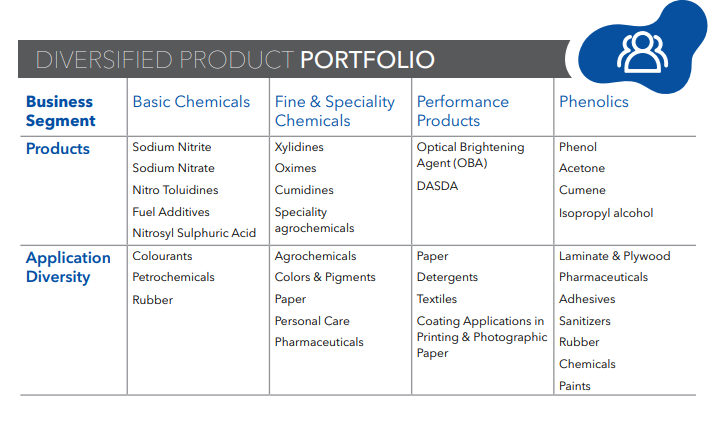

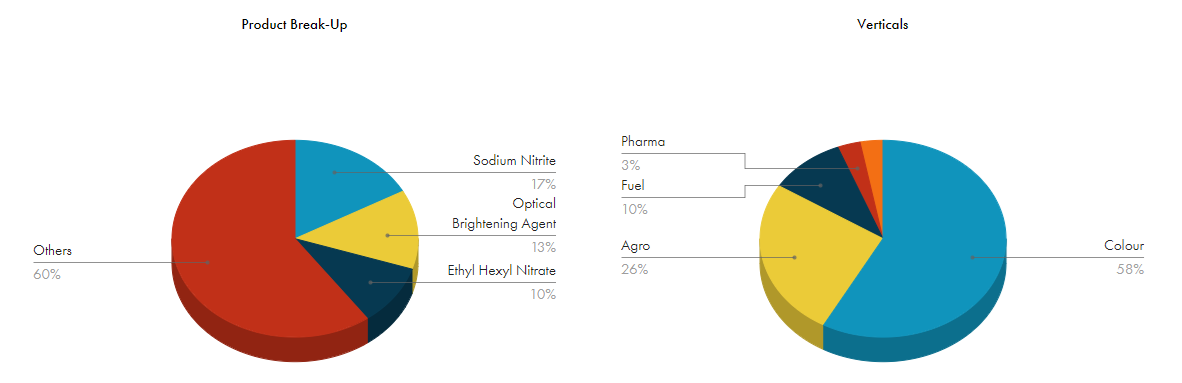

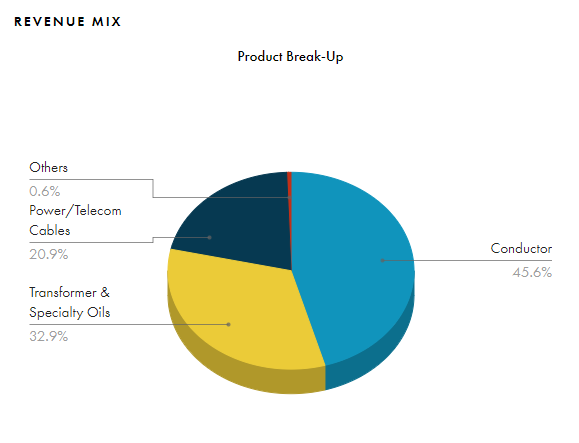

There are 3 segments: #Conductors, Transformer and speciality #oils & Power/Telecom #Cable. The revenue breakup is in the screenshot attached

Crude #oil & #Steel

There are 3 segments: #Conductors, Transformer and speciality #oils & Power/Telecom #Cable. The revenue breakup is in the screenshot attached

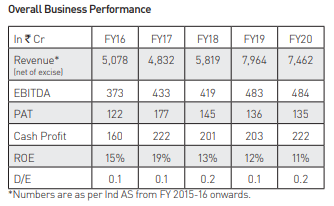

Domestic revenues decline 52% YoY with lockdown in April, lower scale of operations in May-June; #Exports up 11% YoY. Management focus is on improving revenue generation from high value products. Long time consolidation in financial parameters

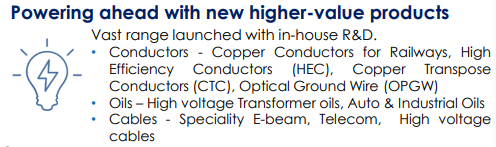

Conductors: High value products were @ 38% of total segment revenue and management is focusing on increasing share of these products; EBITDA Margin ~ 4-5%

INR 2,004 crore order book as on March 31, 2020

Customers: Electrification companies, Railways (Mainly)

INR 2,004 crore order book as on March 31, 2020

Customers: Electrification companies, Railways (Mainly)

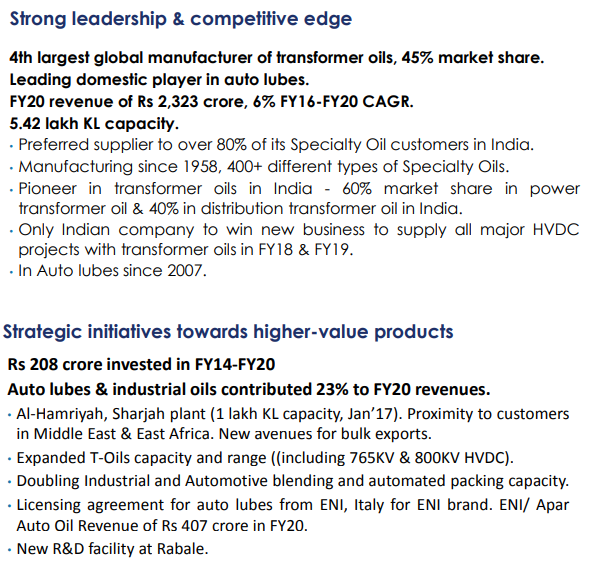

Speciality Oils: 37% revenue from #exports. Enough capacity with company so no need for any #capex for speciality oils. Expect Q2 to have better volumes and profitability. EBITDA Margin ~ 5-7%

Customers: #Auto (including tractors), Industrial & #agriculture.

Customers: #Auto (including tractors), Industrial & #agriculture.

#Cables: 27% revenue from exports. But recession in this segment. High competition & low demand from all sectors, only bright spot are demand for OFC cables post monsoon due to ‘work-from-home’ #bandwidth demand. EBITDA Margin ~ 10-13%

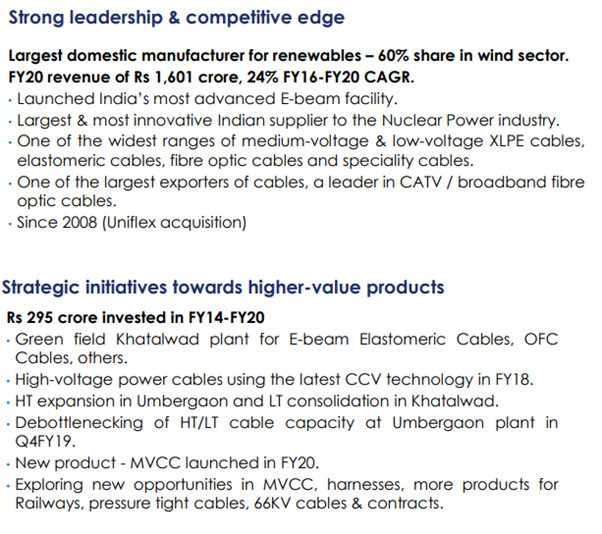

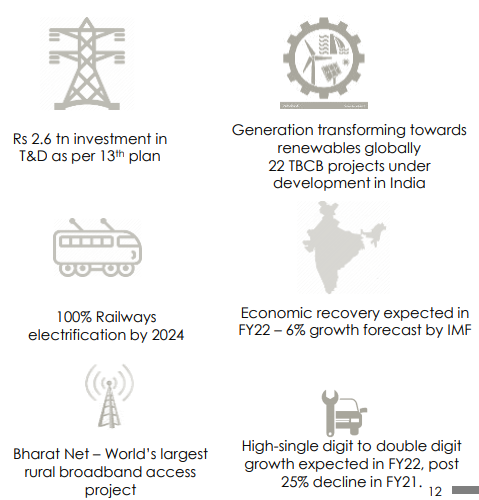

Positive headwinds are #government intervention in DISCOM’s and privatization of the same. So Strong medium term growth drivers.

Rs. 90,000 crore #bailout package for the stressed DISCOMs as a part of the #Atmanirbhar #Bharat Abhiyan is to tide the COVID19 pandemic

Rs. 90,000 crore #bailout package for the stressed DISCOMs as a part of the #Atmanirbhar #Bharat Abhiyan is to tide the COVID19 pandemic

Transmission & Distribution project executing companies are direct customers.

#Renewable #power sector projects are another positive for the company

#Renewable #power sector projects are another positive for the company

Negatives – The year 2021 is going to a year for recovery, amazing performance can be expected from last quarter of CY21 so it will be a long wait for any amazing gains; expect fireworks from H2 FY21 only. Company is focused on good customer profile so top line will be subdued.

Positives - Company has cash & cash equivalents of 165 Cr; No additional capex is needed. Headwinds from govt. policy perspective and there are ample of opportunities for the company. Aggressive railway electrification, Power for All and privatisation of DISCOM’s to name a few.

As soon as things return back to normal company’s profit margins will improve a lot since share of high margin products are expanding example (HEC revenue up 96% YoY with good execution, contribution to revenues at 18% compared to 9% in FY19.)

Company’s products are good and there is focus on R&D, good team and founders with a proven track record. Healthy #dividend payouts.

Promoters increased stake, MF have reduced stake & retail shareholders have increased stake. FII & DII also have presence in the company.

Promoters increased stake, MF have reduced stake & retail shareholders have increased stake. FII & DII also have presence in the company.

Strategy: Company is fairly valued so I have entered it @360 and I will keep on accumulating it for next 2 quarters, my target is 500 but it will take time so I will be patient with it and keep on reviewing it. Lifetime high is 850 and it is at 360 so it’s a contra call for me.

Please let me know if I have overlooked something or there are some insights that you guys have.

Hope this helps @sucrel @sureshg321 @aammiitt2

Hope this helps @sucrel @sureshg321 @aammiitt2

@threadreaderapp Please unroll.