,

71 tweets,

19 min read

Read on Twitter

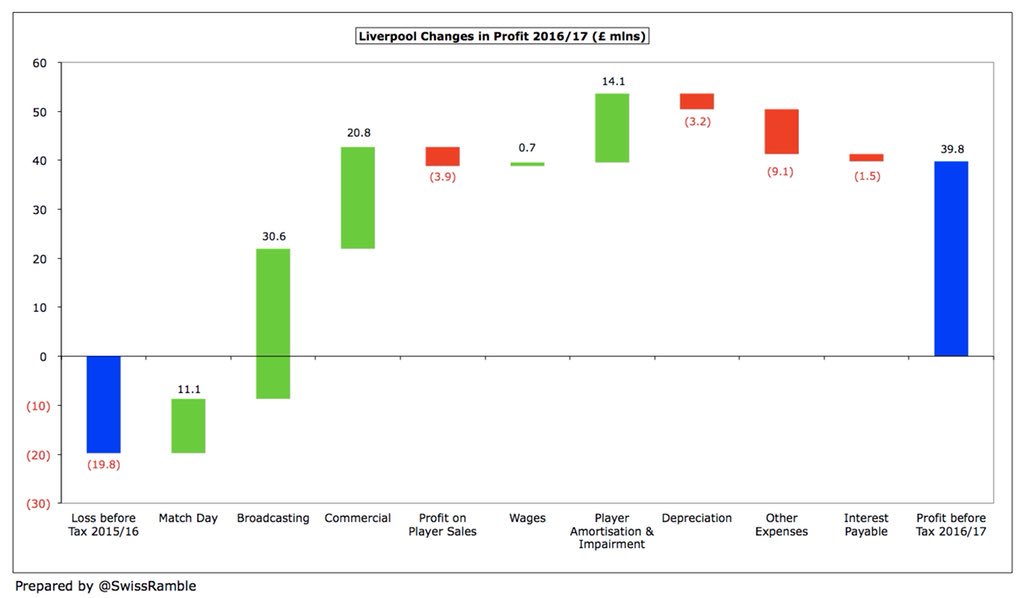

Lots of tweets with "FSG only interested in profit". If so, they're not very good at it. +£20m losses in 4 of 6 FYs since #lfc takeover.

The more serious point is that they're interested in #lfc as a long-term investment and (a) that's not a surprise and (b) isn't a problem.

There are now very few, if no people/investment groups who buy top-flight football clubs with simply pure and noble sporting objectives.

MCFC/CFG? In part arguably the furtherance of the UAE's political objectives to create the impression of a progressive, modern gulf state.

See, for example, here, for further discussion of Man City (and of course much of what David Conn has written). theguardian.com/football/2013/…

FSG are accused of taking money out of #lfc (with no evidence), yet at MUFC sums taken by Glazers may be +£1bn. independent.co.uk/sport/football…

Chelsea: What to make of a man who says he has no connection to Russian government but gifts a £25m yacht to Putin.

independent.co.uk/news/people/vl…

independent.co.uk/news/people/vl…

£110m IC loan (1.24%) for Main Stand funding, £150m revolving credit facility (2.24%) for w/cap to 2020 (refi 2015).

Not true. For FY ending 2016, #lfc's FTE was 700 (500 commercial/admin/other), MUFC 799 (636 comm/admin/other).

Indeed, the other point to make here is that #lfc's proportion of comm/admin/other staff to FTE is also lower than MUFC (71.4% to 79.6%).

Also not useful to compare MCFC like for like here. MCFC's financial report notes 170 commercial/admin staff, but further 437 work for CFG.

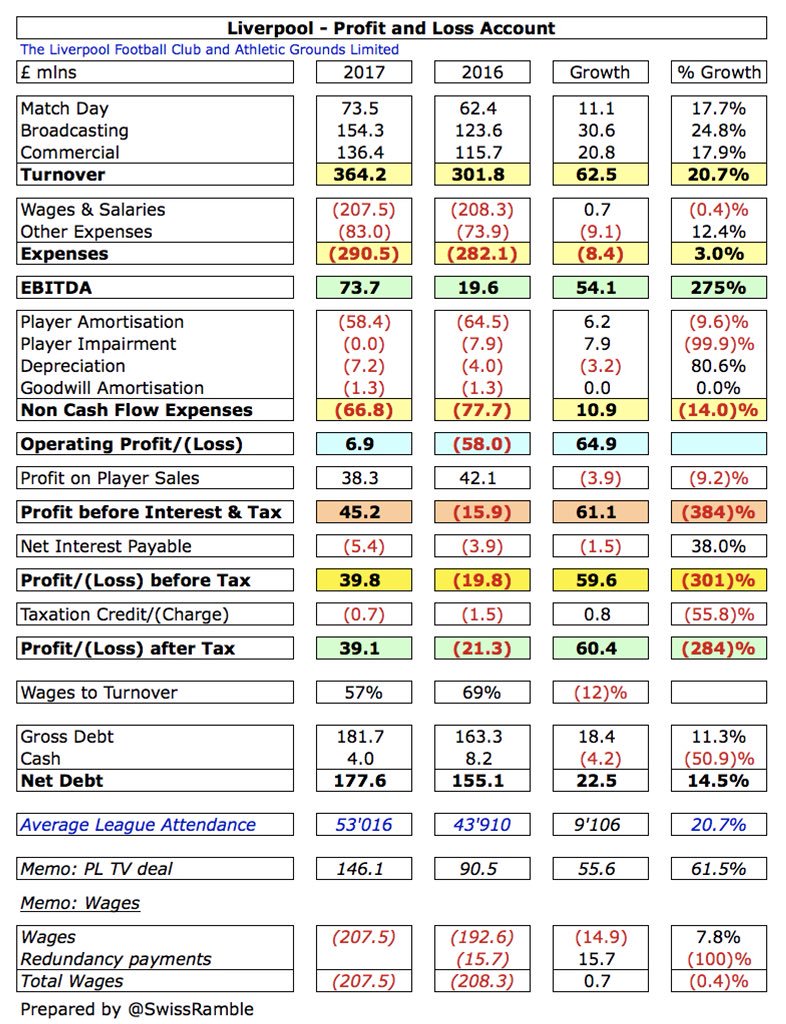

I'm quoting post-tax losses from the annual financial reports, you're describing revenue.

Profit (loss)

2010-11 (49.4m) - part inc. H&G

2011-12 (£40.5m)

2012-13 (£49.9m)

2013-14 £413 (pounds total)

2014-15 £58.8m

2015-16 (£21.4m)

2010-11 (49.4m) - part inc. H&G

2011-12 (£40.5m)

2012-13 (£49.9m)

2013-14 £413 (pounds total)

2014-15 £58.8m

2015-16 (£21.4m)

And if ever there was a predictable response, it's this - that I'm an "FSG apologist and mouthpiece".

A "mouthpiece" wouldn't be critical, for example, over the botched approach to Van Dijk.

Nor would I have repeatedly raised the issue of ticket pricing at Anfield - one of several examples here.

Several q's on what I think FSG have done well. My view:

(1) The Main Stand (original pricing aside)/general infrastructure investment.

(1) The Main Stand (original pricing aside)/general infrastructure investment.

(2) (Senior) exec team. Moore (CEO), Hughes (COO), Hogan (CMO/MD), Breglec (Marketing), Black (Comms), and more have v. good reputations.

(3) Engagement. What #lfc are putting in place with Tony Barrett is - with few exceptions - potentially more far-reaching than elsewhere.

(4) Retail. #lfc have the cheapest kit price for adults and youths in the big six in the Premier League.

(5) Cheap tickets for local (L postcode) fans. A very welcome step, and something the club could have decided against over EU law issues.

(6) Fully integrating the women's team into #lfc. Maybe there are some who don't see this as being particularly important, but I do.

(7) The Foundation. While it existed before FSG, it's a wholly different operation to what it can deliver to various communities.

#lfc currently lists 5 exec directors (Henry. Werner, Egan, Gordon, Hughes). Man Utd have 10 (plus 3 independent).

Furthermore, MUFC paid £11.1m in "key management compensation" in 2015-16. LFC (directors) were paid £1.7m.

My club's existence/future to be secure & sustainable is the preference where any comparison is concerned with H&G.

I'm loathe to get into these discussions, but I'm a fan, for several seasons was a steward, & go to games regularly.

There is absolutely no evidence to demonstrate that FSG have "drained" - i.e. taken money out of #lfc - revenues are simply re-invested.

It's possible to dispute the manner/type/scale of particular investments (into e.g. the playing squad), but not the actual revenue cycle.

And as I'm much less qualified to say who/when/why/(how much) certain players should be bought (for), I'll leave that for others to discuss.

And it's only reasonable to discus the reverse. Where do I think #lfc could improve/do better? There are, for me, a couple of key issues.

(1) For some it might not be a concern, & commercial income means the club can invest, but I found the Bet Victor deal problematic.

Without getting into it too deeply, I'd simply prefer not to see gambling companies promoted on merchandise/club assets used for the same.

As a general principle, community-oriented clubs shouldn't so heavily involve themselves with an industry which can disrupt the same.

(2) Anfield Road expansion. The season ticket waiting list, I think, is still somewhere in the region of 26,000.

Outline permission expires Aug 2019, which might mean an expanded Anfield Rd, if I remember the planning process correctly, as late as 2023.

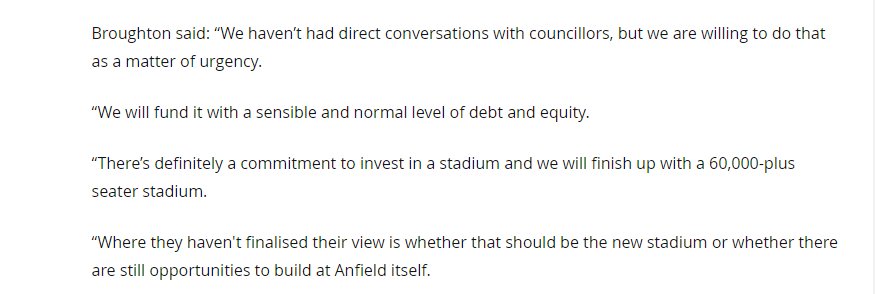

Back when FSG took over, then Chairman Martin Broughton said "we will finish up with a 60,000-plus seater stadium."

liverpoolecho.co.uk/news/liverpool…

liverpoolecho.co.uk/news/liverpool…

Whilst I recognise (my own!) arguments about where to place investment, 12 years to add c.15k seats where demand exists seems rather slow.

I could, quite happily, forego transfer fees totalling c.£45m to see more people at Anfield. Others might and probably would disagree.

And that's to exclude/ignore the fact that infrastructure investment is effectively excluded from any FFP break-even calculations.

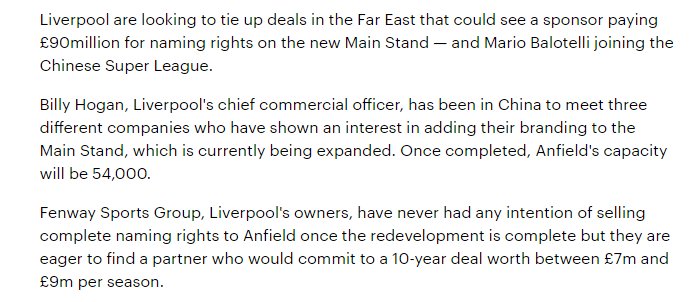

(3) Naming rights

Feb 16: #lfc "close to £90m deal."

Mar 16: May not be in place before Main Stand opens.

Aug 16: Unlikely to be until 2017.

Feb 16: #lfc "close to £90m deal."

Mar 16: May not be in place before Main Stand opens.

Aug 16: Unlikely to be until 2017.

Assuming all the reporting is correct, it's Aug 2017 and it appears rather quiet on that front (which doesn't mean to say it actually is).

But as a larger point, the commercial revenues from "a" naming rights deal (whether combined with other assets or not) are important.

Politics teacher and fan of club known for political fans deems politics not important.

So they aren't perfect, they do make mistakes, and I think they can do a number of things better - or at least, I'd prefer different action.

But they aren't mendacious, they aren't taking money out of the club, and the club is in a much better place than it was 7 years ago. *Ends*

#lfc have "no plans" to sell Main Stand naming rights this (2017-18) season but are thinking of one for Kirkby. liverpoolecho.co.uk/sport/football…

Olly Dale's words - it "isn't an immediate priority" - are interesting. An implication that the MS was more successful than anticipated?

i.e. "We find ourselves in a great position with Anfield with the new main stand which has been a terrific success".

As far as I'm aware, there was never any indication that naming rights were crucial/critical to the Main Stand financing/loan repayments.

Further thoughts: Dale (Commercial Director) said "that's not something [at the] top of our to do list ... in terms of ... commercial."

In a broader context, this makes perfect sense. Standard Chartered’s current shirt sponsorship deal expires at the end of 2018-19.

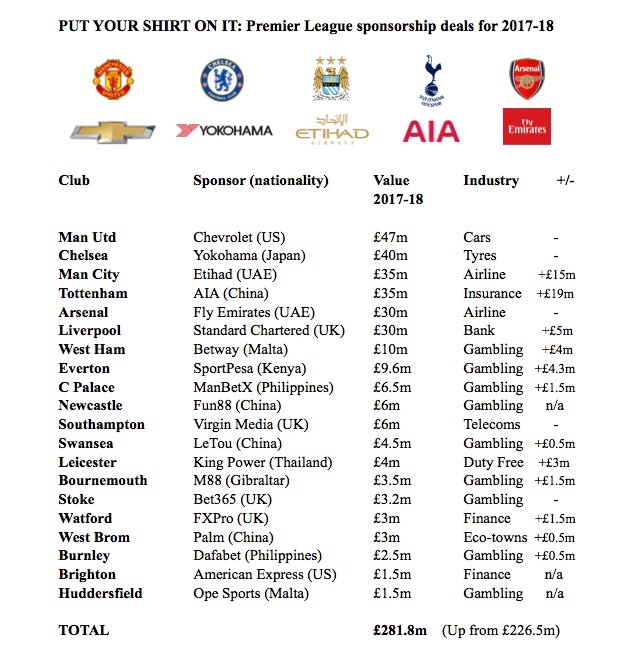

As per @sportingintel, #lfc (with Arsenal) now have the smallest shirt sponsorship income of the big six clubs.

sportingintelligence.com/2017/07/24/pre…

sportingintelligence.com/2017/07/24/pre…

There has been investor unrest at Standard Chartered over the value generated, & given the bank’s recent troubles.

And maybe it wasn’t intentional/a “signal”, but Standard Chartered appeared less keen on advertising it this year.

Given in FY 15-16 £25m per year (now £30m p/y as part of the 16-19 extension) constituted 22% of total commercial income, it’s a vital deal.

& given its importance/other factors, this deal of any will surely be “at the top of [the] to do list in terms of the commercial programme.”

Rumoured #lfc approached Nomura (among others) prior Standard Chartered's extension; wonder if it will be revisited. liverpoolecho.co.uk/sport/football…

Whilst a rumour, Nomura were Sponsorship Consulting's client (since sold – now Bastion?), who worked on Standard Chartered’s side re: #lfc.

One more deal currently scheduled to expire in 2019 is Carlsberg (involved commercially in some shape/form with #lfc since at least 1992).

Indeed, perhaps worth pointing out, again just for the broader context – believe 8 of #lfc’s 15 current official partnerships expire 2019.

Which isn’t a surprise/problem – of 5 of 8 began in 2016. But perhaps puts in perspective where priorities might lie for a commercial team.

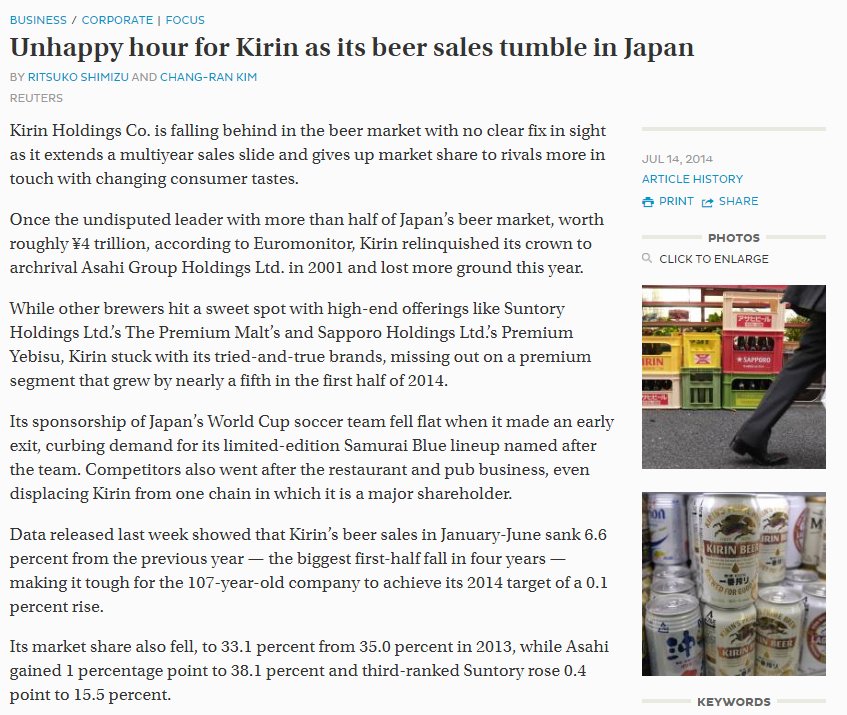

On the subject of Carlsberg, and just idle musing on my part, but Japan's Sapporo have recently been on the acquisition/expansion trail.

Week ago Sapporo bought San Francisco’s (craft brewery) Anchor Brewing; they’re behind Asahi, Kirin, & Suntory domestically in market share.

Beer consumption is on the wane domestically (ageing population); Japan's breweries (see also Sleeman purchase) need international growth.

They have a decent sized soft drinks range via their Pokka brand to cover regions where alcohol consumption is restricted/banned.

Global business growth is part of the Sapporo group's “Speed150” long-term management vision; Europe/US/SEA are key target markets.

In terms of #lfc’s own ambitions in terms of growth, there’s probably some useful overlap/alignment here (& importantly the beer’s better).