In this thread, I assess the following argument for the claim that #USS is not in deficit:

Argument #2: The scheme is not in deficit but rather is in surplus because it is in surplus on a best estimate basis.

1/

Argument #2: The scheme is not in deficit but rather is in surplus because it is in surplus on a best estimate basis.

1/

This is the second in a series. See this embedded link for my assessment of Argument #1: 2/

Argument #2 figures in @UCU's HE8 (linked), which speaks of "the artificial creation of the USS deficit" and calls on UCU negotiators to replace USS's approach to the valuation by "best estimate", among other things. 3/

ucu.org.uk/article/9502/H…

ucu.org.uk/article/9502/H…

As I mention in my Arg #1 thread, whether USS is in deficit as of 31 Mar 17 is a matter of whether contributions prior to that date, plus the returns on the investment of these contributions, are sufficient to cover the pensions promises to which these contributions give rise. 4/

If we could look into a crystal ball which reveals (a) precisely how great the investment returns on these contributions will be in future years and (b) the precise pension payments to which these contributions will give rise... 5/

...where (b) is a matter of how much these 1/75 accruals to which these contributions give rise will be revalued by CPI in future years, and how long each person will live to receive the promised pension... 6/

If we could look into a crystal ball which reveals (a) and (b), then we could calculate, with certainty, whether the assets in the scheme as of 31 Mar 2017 are sufficient to cover all the liabilities with which they're associated. 7/

Of course, we lack such certain knowledge, of how long each pensioner will live, how much CPI will increase in future years, and especially of what the investment returns on the assets will be. 8/

What do we do in the face of such uncertainty? We might take a 'best estimate' approach, as UCU's HE8 advocates. On this approach we gather and analyse the available evidence in order to come up with estimates of longevity, inflation, and investment returns. 9/

A best estimate is one that has a 50% chance of coming true and a 50% of being false. 10/

According to USS, the scheme is in surplus on a best estimate basis. In other words, the investment returns on past contributions there is a 50% chance of achieving are more than sufficient to cover the pensions promises associated with those contributions. 11/

A 'best estimate', however, tells us nothing about how far short of full funding the scheme might fall if investments fail to achieve what they have a 50% chance of achieving. 12/

If there's a sufficiently high chance that investment returns will fall very far short of full funding, then it is imprudent to fund the scheme on a best estimate basis. 13/

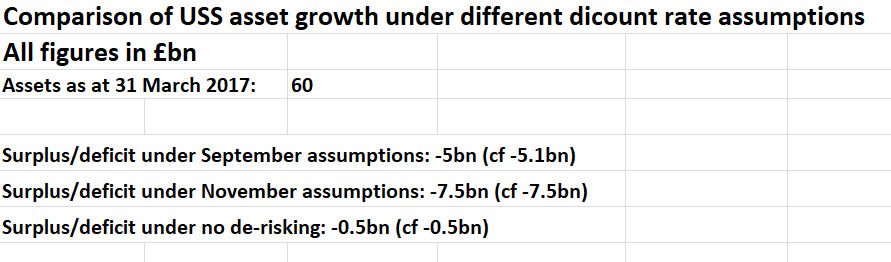

Moreover, the downside risk of 'growth assets' such as equities are generally regarded as greater than that of bonds. See this chart for an illustration of the relative downside risks of an 80/20 equities-bonds split, versus 60/40 equities-bonds, and 20/80 equities-bonds. 14/

Though the best estimate median (50%) returns on an equity-weighted portfolio are much higher than for a bond-weighted portfolio, the downside risk is also much higher. USS's current portfolio is approximately 60/40 equities-bonds (middle graph). 15/

It would be imprudent to fund pensions promises on a best estimate basis when there is a sufficiently high downside risk that investment returns will fall so far short of this estimate that it would be difficult or impossible to recover from that shortfall. 16/

Moreover, the regulations call for the funding of schemes on a prudent, rather than a best estimate, basis. (This requirement of prudence applies both to investment returns and longevity.) 17/

USS maintains that the appropriate prudent adjustment of assumed investment returns on its portfolio takes us from a 50% (best estimate) chance of full funding to a 67% chance of full funding. 18/

It is open to debate whether so great an adjustment, from 50% up to 67%, is warranted. (For the 2014 valuation, USS adopted the slightly less demanding requirement of a 65% chance of success.) 19/

By my lights, however, it would be imprudent to fund the scheme on a best estimate basis, given the downside risks of both the current c. 60/40 equities/bonds portfolio and the 'de-risked' c. 50/50 equities/bonds portfolio to which USS plans to shift over the next 20 years. 20/

In any event, there is no chance that the USS trustee, the scheme's actuary, or the pensions regulator would accept a funding of the scheme on a best estimate basis. 21/21