1/ 📚 Random Research Note

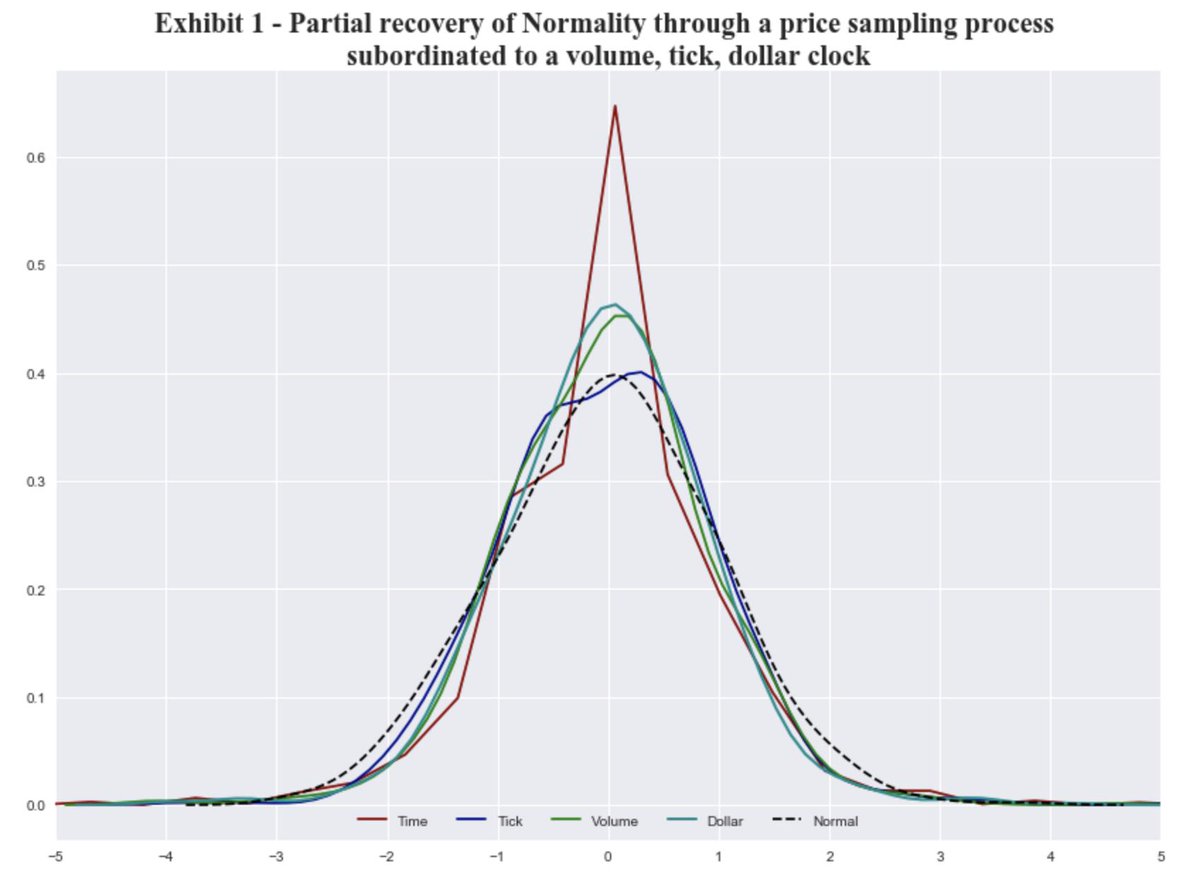

While doing research in 2006-2007, one of the interesting phenomenon I found was that sampling a data on a non-time-related domain created beneficial statistical properties.

While doing research in 2006-2007, one of the interesting phenomenon I found was that sampling a data on a non-time-related domain created beneficial statistical properties.

2/ In other words, I would transform a time-series so that the x-axis was no longer a constant time measure, but rather something like constant volume, ticks, or even variance.

3/ Suddenly, "returns" became a lot more normal and stable looking.

(Image source: github.com/Jackal08/finan…; credit @JacquesQuant)

(Image source: github.com/Jackal08/finan…; credit @JacquesQuant)

4/ My hypothesis for this phenomenon was that information flow into the market was not constant over time. So by sampling in the time domain, we were over-sampling during calm periods and under-sampling during chaotic ones.

5/ You can "see" this by looking at something like accumulated variance in the time domain.

6/ I had never heard anyone else really talk about this until I recently read @lopezdeprado's book Advances in Financial Machine Learning.

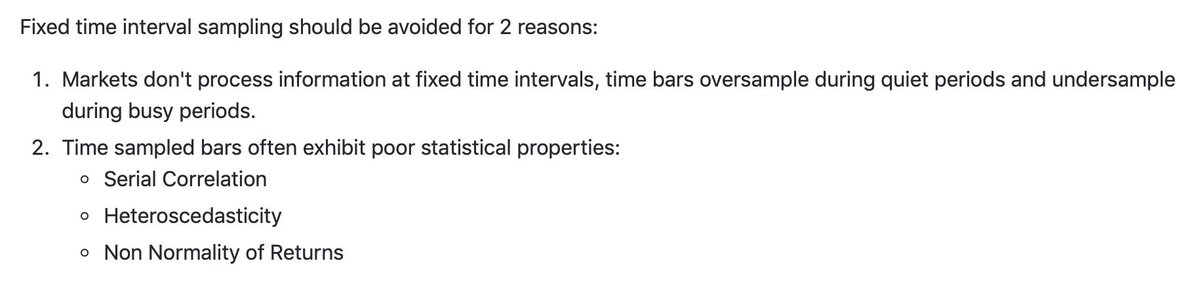

Paraphrasing from github.com/Jackal08/finan… (credit @JacquesQuant):

Paraphrasing from github.com/Jackal08/finan… (credit @JacquesQuant):

7/ Beyond the potential statistical benefits, there are other interesting aspects of domain transformation as well.

For example, an indicator in a fixed volume domain might appear *dynamic* in a fixed time domain.

For example, an indicator in a fixed volume domain might appear *dynamic* in a fixed time domain.

8/ e.g. Here I take $SPY and transform it to a fixed accumulated variance domain, run a 200 bar SMA, and then transform it back to the time domain.

Note how much "faster" it tracks the market in 2008 than the fixed 200 day SMA.

Note how much "faster" it tracks the market in 2008 than the fixed 200 day SMA.

9/ Obviously this has interesting applications in the trend-following domain.

But it might in others as well (e.g. rebalancing on a fixed accumulated variance vs fixed time horizon).

Back to the lab... 👨🔬

FIN.

But it might in others as well (e.g. rebalancing on a fixed accumulated variance vs fixed time horizon).

Back to the lab... 👨🔬

FIN.