,

17 tweets,

7 min read

Read on Twitter

1/ May not feel like it, but this week may be one of the most important in the lifetime of most investors. That's not so much a forecast, but a statement about current extremes, and the pressures weighing on them. I'll just share what I'm seeing, FYI. Do what you wish with it...

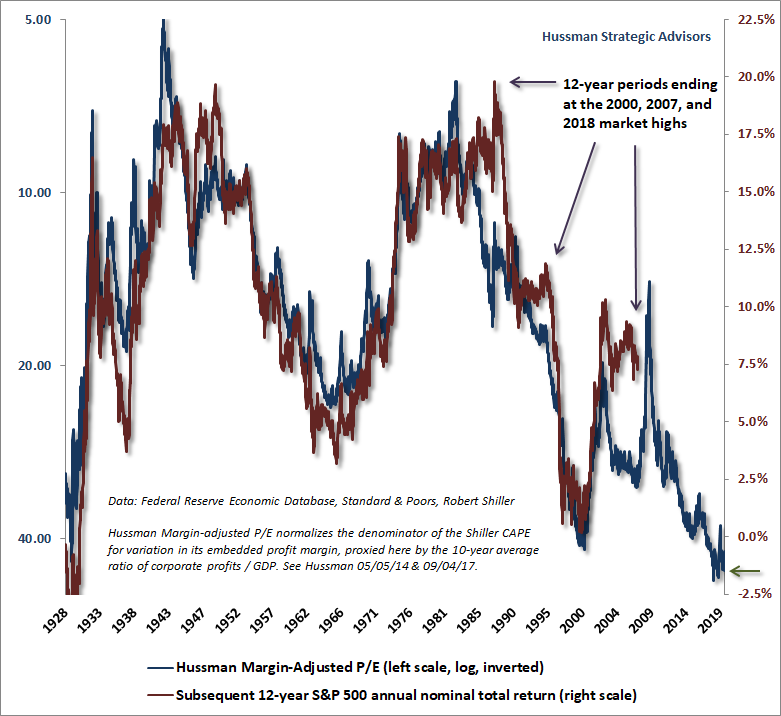

2/ First stop is probably valuations - not just any measure, but those best correlated w/ representative long-term cash flows and actual subsequent market returns. Note that valuations aren't a timing tool. You can't reach hypervaluation without advancing through lesser extremes.

3/ Last week, based on the prevailing level of market valuations and interest rates, my estimate of long-term returns on a conventional asset mix (60% S&P500, 30% T-bonds, 10% T-bills) fell to 0.46%, the lowest level in history except for the single week of the 1929 peak...

4/ Again, though, valuations aren't a timing tool in themselves. You'll notice that in periods prior to a hypervalued extreme, the market - by necessity - will have done better than one would have estimated previously. These deviations are temporary, and they're informative.

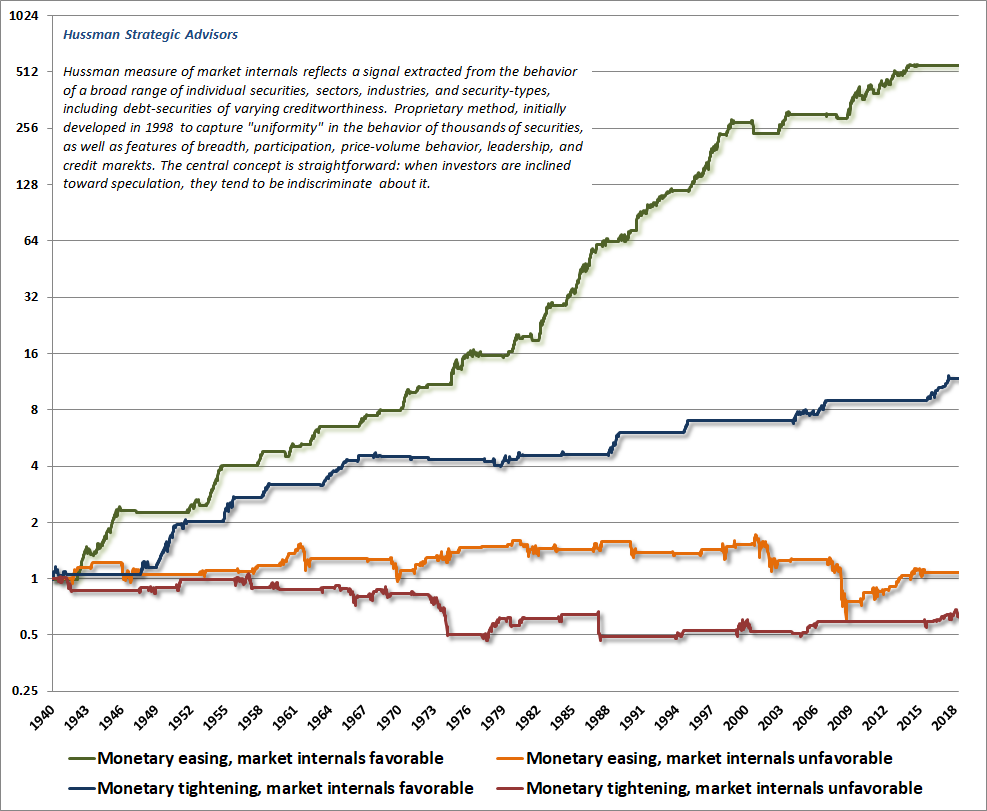

5/ What distinguishes an overvalued market that continues to advance from one at risk of dropping like a rock? It's the *psychological preference* of investors toward speculation or risk-aversion, best inferred from uniformity/divergence of market internals (more: read my stuff).

6/ It's when you have a combination of extreme valuations and divergent internals that a "trap door" often opens below the market. This is something we also observed at the 2000 and 2007 peaks. (Trolls, be patient. I'll get to my admitted error in this half-cycle in a second).

7/ So what was my recent error despite my prior success in decades of complete cycles? This half-cycle was legitimately "different" in one way. QE and ZIRP disabled historically reliable "limits" to speculation. We have to abandon a bearish stance unless internals are negative.

8/ Which brings us to the present, where we observe not only unfavorable valuations and still-divergent internals on our measures, but also the most extreme "overvalued, overbought, overbullish" syndrome we define. The others there were the precise peaks of 2000, '07, and Sep18.

9/ We're now about 3.2% above the Sep 18 peak, and even on much simpler measures, we've seen extremes in the past month that reflect internal divergences suggestive of increasing risk-aversion among investors.

10/ But isn't the Fed going to cut rates this week? Well, yes, I do expect the Fed to cut rates. Most likely by 0.25%, which is the current spread between the T-bills and target Fed Funds. If they move 0.5%, it will be because they have seen Friday's payroll report in advance.

11/ What's the issue w/ Friday's jobs report? Tho we can't be certain b/c a) it's a noisy signal, and b) NFP figures tend to be heavily revised around economic turns, leading measures suggest a roughly -270k shortfall from the past 10mo avg, which may give us a negative print.

12/ So yes, the Fed is likely to ease, but it's easing because recession risk is a whole lot hotter than investors may recognize. Indeed, current employment and yield curve conditions are already consistent with what we often see in association with oncoming or ongoing recession.

13/ And that's why the initial easing by the Fed, following a tightening cycle (see the chart text for how I've classified these) is also typically associated with an oncoming or ongoing recession.

14/ Won't Fed easing put a floor under stocks? Well, if you remember the 2000-2002 and 2007-2009 collapses, it should be clear that the Fed eased persistently and aggressively the whole way down. When investors are risk-averse, risk-free liquidity isn't an "inferior" asset.

15/ As it turns out, the market's response to Fed easing is entirely dependent on whether investors are inclined toward speculation or risk-aversion, and the market's response to valuations, that's best gauged by attending to market internals directly.

16/ As a side note, the internal dispersion we currently observe in the market has admittedly been uncomfortable for hedged equity strategies, particularly those with value-focused stock selection. Of course, that also tends to set up positive conditions for value in the future.

17/ The bottom line is that we have a hypervalued market, with the worst estimated prospective return for a conventional mix since the 1929 peak, divergent internals, extreme overextension, and oncoming recession risk. Whatever you're going to do, do it.

hussmanfunds.com/comment/observ…

hussmanfunds.com/comment/observ…