,

16 tweets,

11 min read

Read on Twitter

1/ Anomalies and News (Engelberg, McLean, Pontiff)

"Using a sample of 97 stock return anomalies, we find that returns are 6 times higher on earnings announcement days. Results are consistent with biased expectations being at least partially corrected."

papers.ssrn.com/sol3/papers.cf…

"Using a sample of 97 stock return anomalies, we find that returns are 6 times higher on earnings announcement days. Results are consistent with biased expectations being at least partially corrected."

papers.ssrn.com/sol3/papers.cf…

2/ Anomaly returns are 6 times higher on earnings days (and 50% higher on stock news days) relative to other days.

(The authors create an aggregate long-short portfolio that combines 97 anomalies and then look at how that portfolio performs on earnings and news days.)

(The authors create an aggregate long-short portfolio that combines 97 anomalies and then look at how that portfolio performs on earnings and news days.)

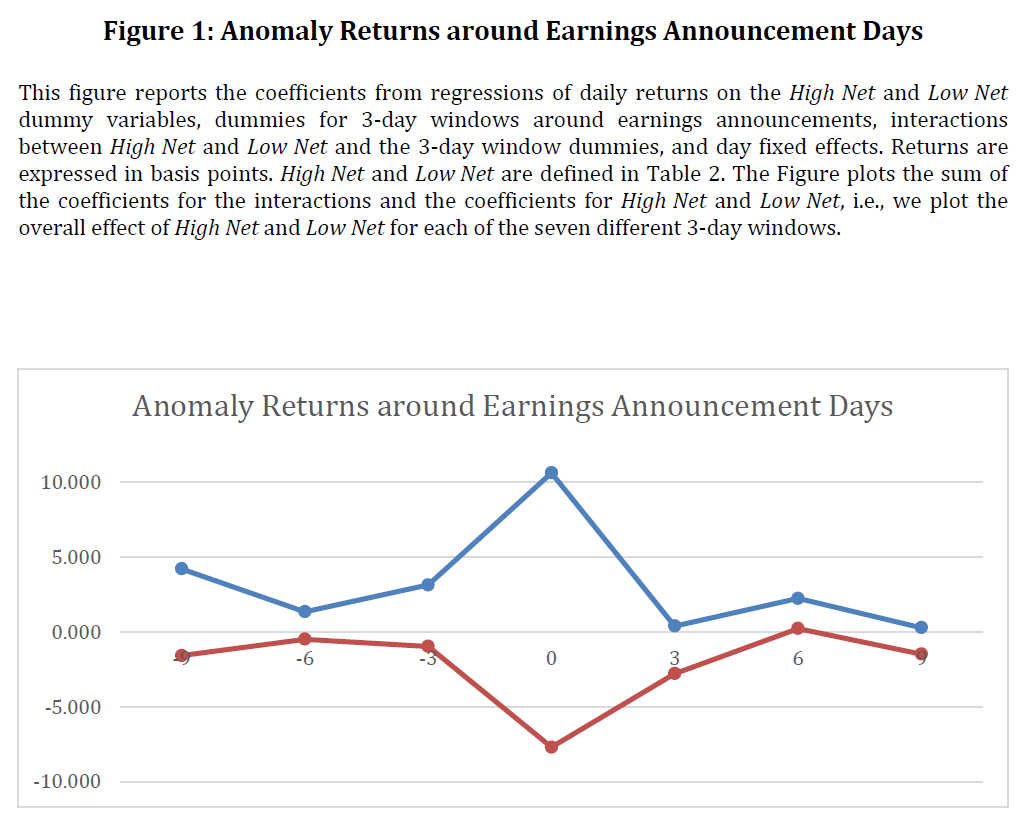

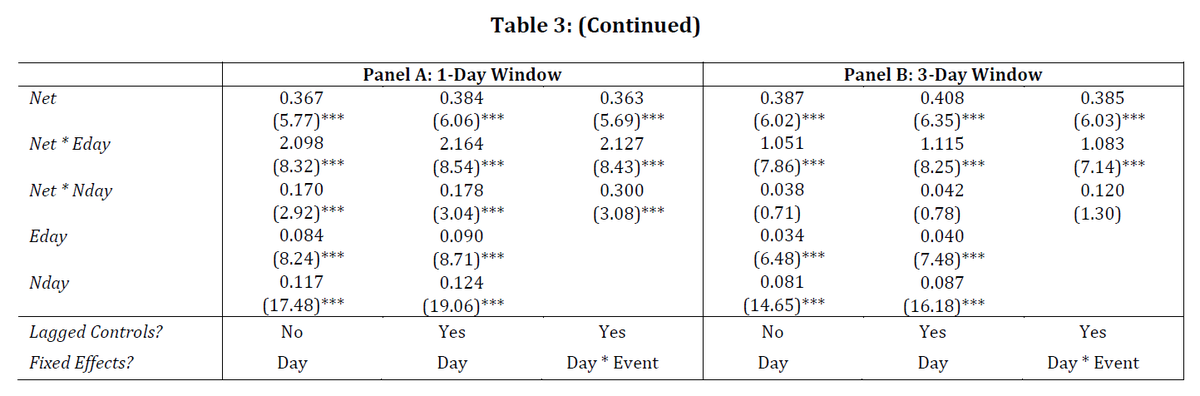

3/ When returns are examined for the most extreme quintile portfolios (High Net and Low Net), both the long and short sides produce stronger returns for individual stocks on their earnings and news days.

This is the case both for the day and the three-day window around it.

This is the case both for the day and the three-day window around it.

4/ Both the long and short sides of anomaly portfolios appear to perform better on earnings days.

This appears to be a one-time effect that doesn't reverse afterward. Instead, anomaly returns just go back to behaving as they would on normal non-earnings days.

This appears to be a one-time effect that doesn't reverse afterward. Instead, anomaly returns just go back to behaving as they would on normal non-earnings days.

5/ This result appears to hold when anomalies are broken down into categories (Market, Valuation, Fundamental, and Event).

Anomalies built on company-specific information are affected more by earnings than news days; anomalies built on market data are affected equally by both.

Anomalies built on company-specific information are affected more by earnings than news days; anomalies built on market data are affected equally by both.

6/ The authors find seasonality: Mondays have good returns, although not as good as news days' returns. They hypothesize that news gets released over the weekend that can't be traded until Monday.

(Of the days in the sample, 14.5% are news days, and only 1.1% are earnings days.)

(Of the days in the sample, 14.5% are news days, and only 1.1% are earnings days.)

7/ Anomaly portfolios don't perform well on macroeconomic news days, which are therefore unlikely to explain the effects described above.

Controlling for extreme returns (daily return squared) doesn't eliminate the effects either.

Controlling for extreme returns (daily return squared) doesn't eliminate the effects either.

8/ Although the anomaly long portfolio tends to contain lower-beta stocks than the short portfolio does, this difference (as well as the elevated market betas on earnings days) do not appear to explain the effects described earlier.

9/ The factor beta of the long portfolio increases on earnings days (and the factor beta of the short portfolio becomes more strongly negative), but controlling for this doesn't materially alter the paper's earlier findings.

10/ Analysts' forecasts tend to be (1) too low for stocks in the anomaly long portfolio and (2) too high for stocks in the short portfolio. In other words, analysts are normally wrong about these stocks, and over-pessimism/over-optimism could contribute to anomaly returns.

11/ After controlling for monthly returns, the authors find that more of these returns are earned on information days than on other days, partially alleviating concerns about the anomalies being the product of data mining.

12/ Information-day anomaly returns tend to be dramatically larger for small stocks than large ones (resulting in higher t-stats as well).

Using only out-of-sample data for each anomaly (based on publication year) leads to similar results as for the full sample.

Using only out-of-sample data for each anomaly (based on publication year) leads to similar results as for the full sample.

13/ Analysts forecast in the wrong direction (more over-optimistic for stocks that will later have lower returns.). After controlling for monthly returns, the authors find that analysts also tend to forecast in the wrong direction for both the anomaly-long and -short portfolios.

14/ This is consistent with what others have found about analysts being the most over-optimistic about the worst factor stocks. For example...

16/ Although information (earnings) days only occur 35% (5%) of the time, they account for more than 80% (17%) of anomaly returns.

Even though earnings days affect valuation, fundamental, and event anomalies the most, there's still a marked effect on market-driven anomalies.

Even though earnings days affect valuation, fundamental, and event anomalies the most, there's still a marked effect on market-driven anomalies.

17/ Table A3: When analyst forecasts are wrong by more than one standard deviation from the sample mean, anomaly returns appear to be very high, supporting the hypothesis that anomaly returns are driven by inaccurate expectations.