,

38 tweets,

12 min read

Read on Twitter

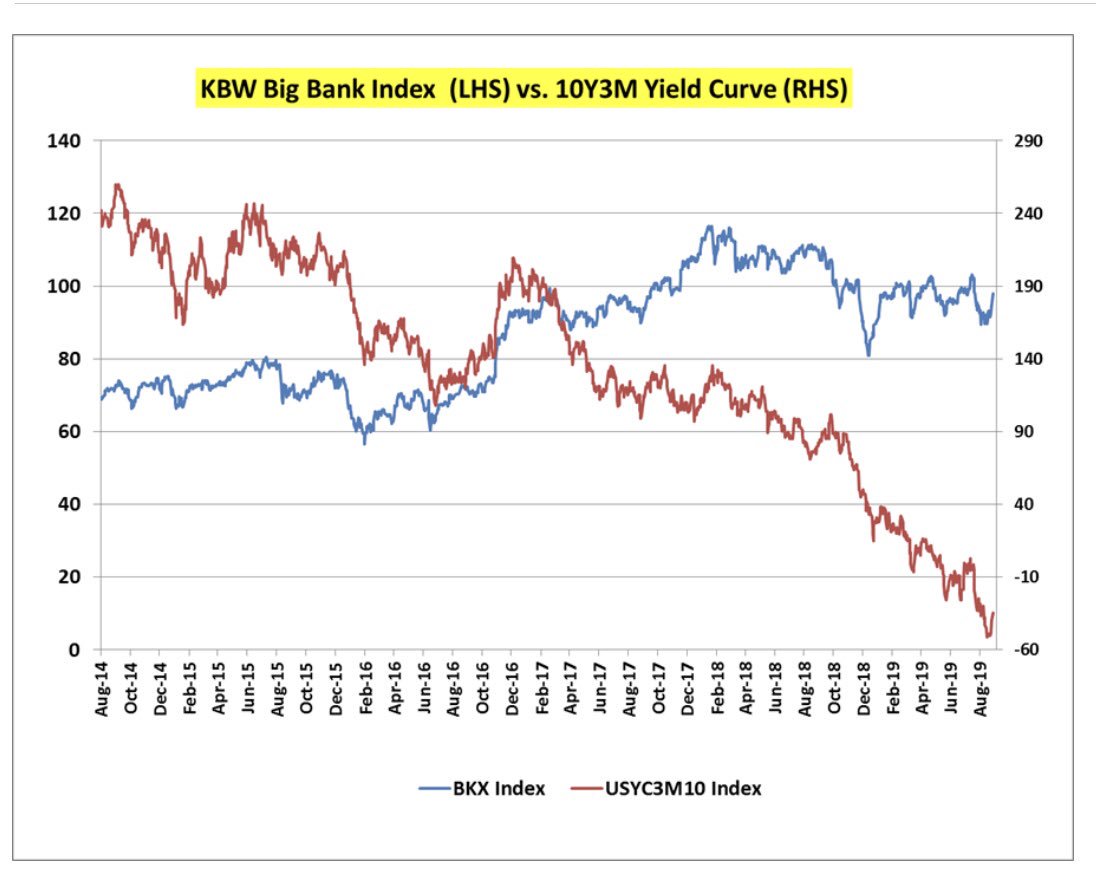

It’s just the beginning.. rate cuts take time to price in. Spread between bond market rate expectations & Bank stocks are large. There’s a lot of $XLF complacency imho..just hear Bank CEOs talk up the economy & their book. Credit costs are edging higher in C&I & already in Cards.

At some point the gravitational pull of the Yield Curve may be a rude awakening for Street Consensus $XLF Bulls & Bank Management.. unless the assertions that this time is different with the Curve comes to Bear over time.

BKX Index approaching a #DeathCross

$TLT $KRE $IWM

BKX Index approaching a #DeathCross

$TLT $KRE $IWM

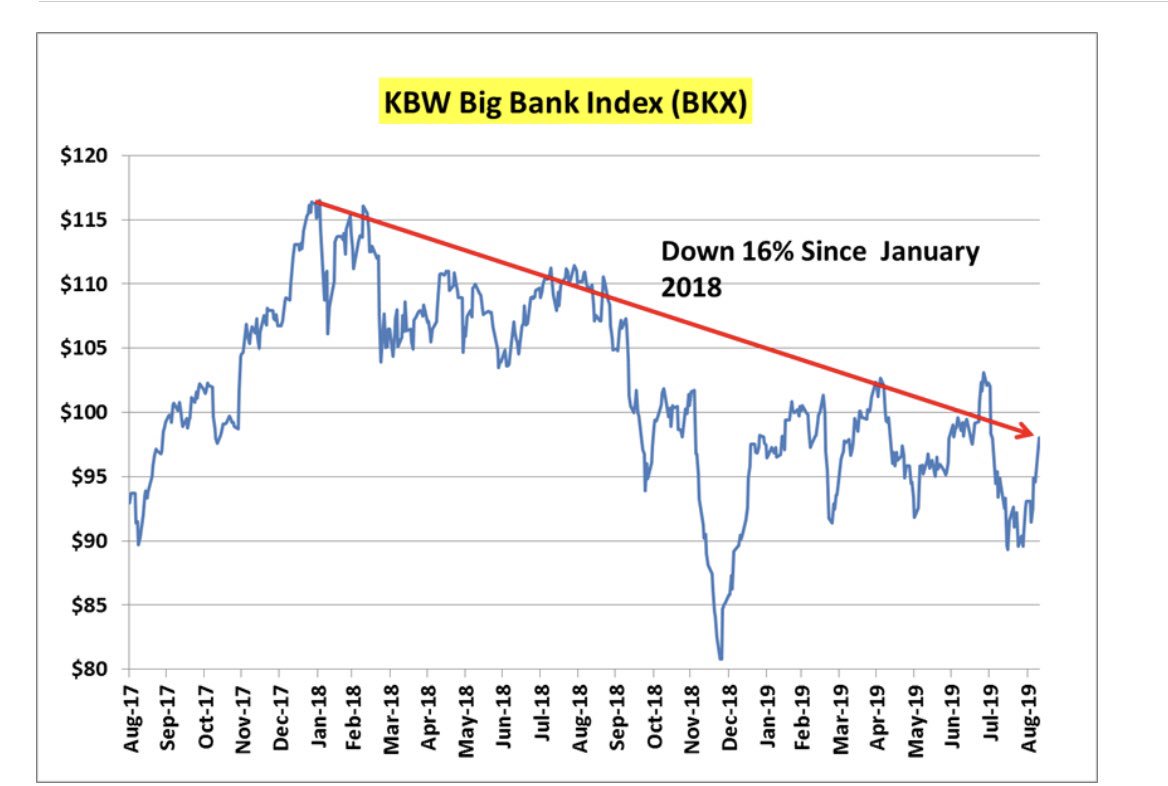

$XLF Bulls who bought Big US Banks BKX Index since its Peak Bank Street & Management Complacency at the top in Jan 2018.... are getting absolutely pummeled... down 16% vs. Cash or $TLT.

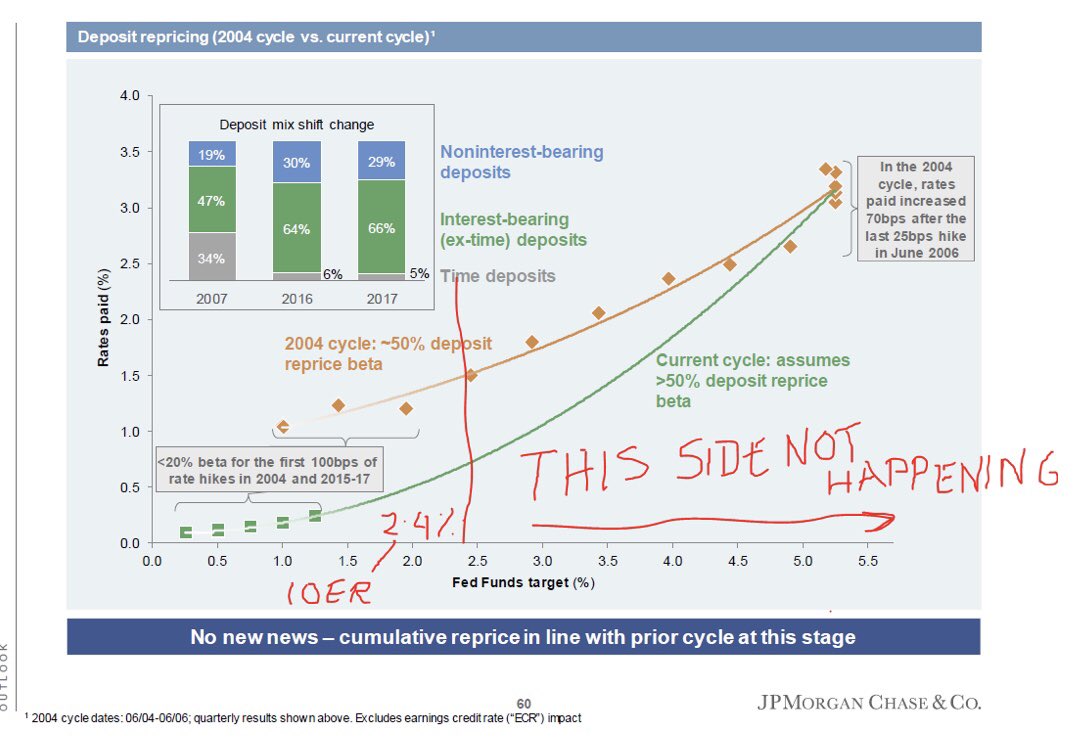

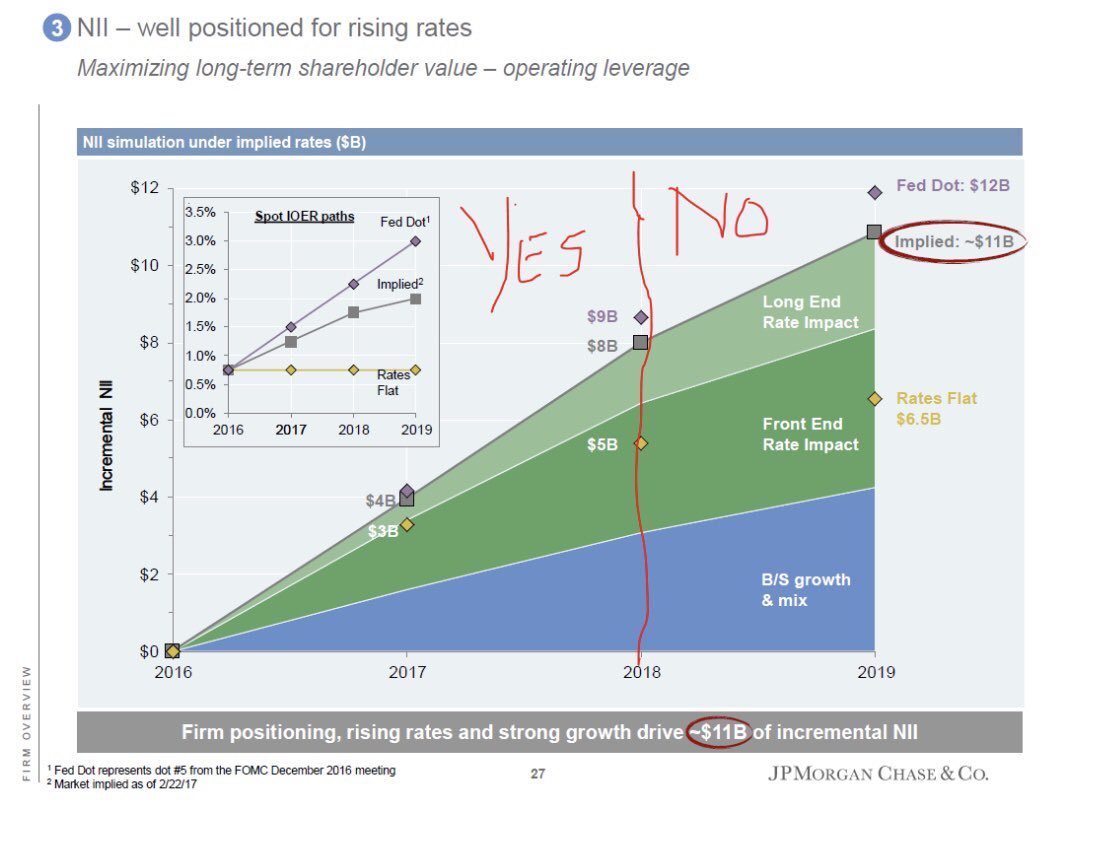

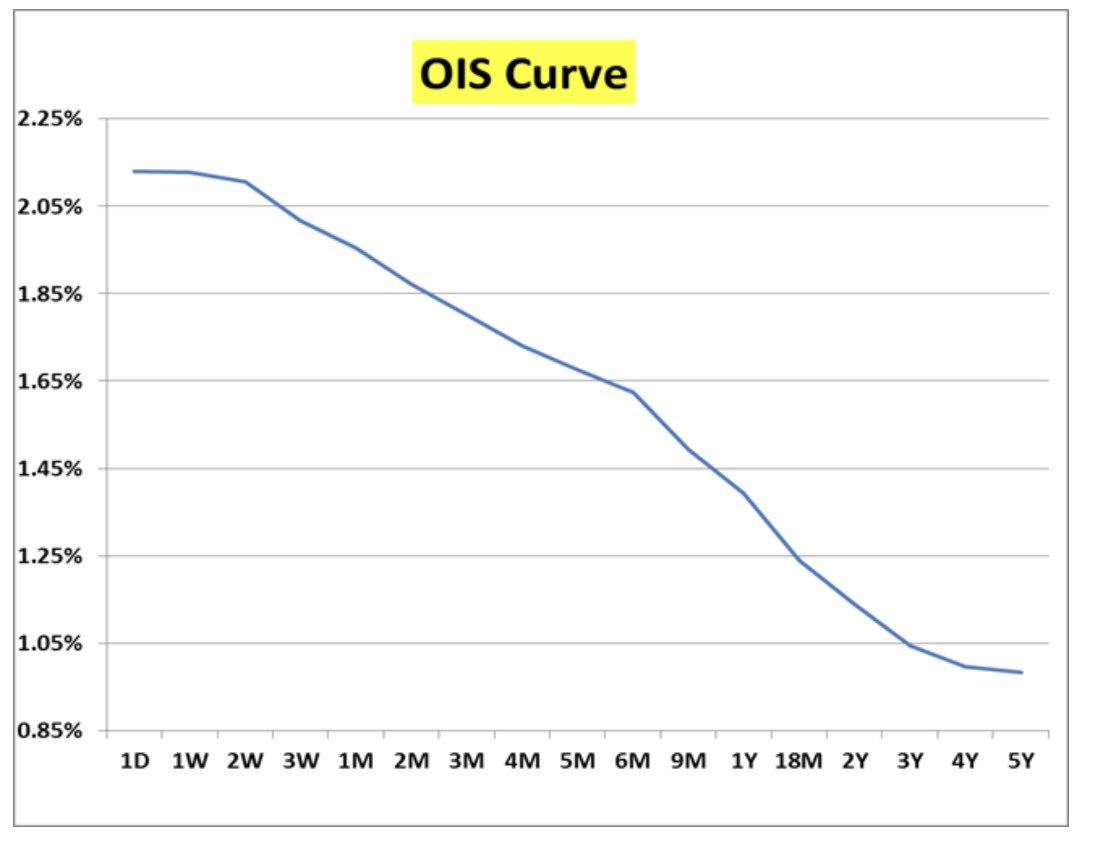

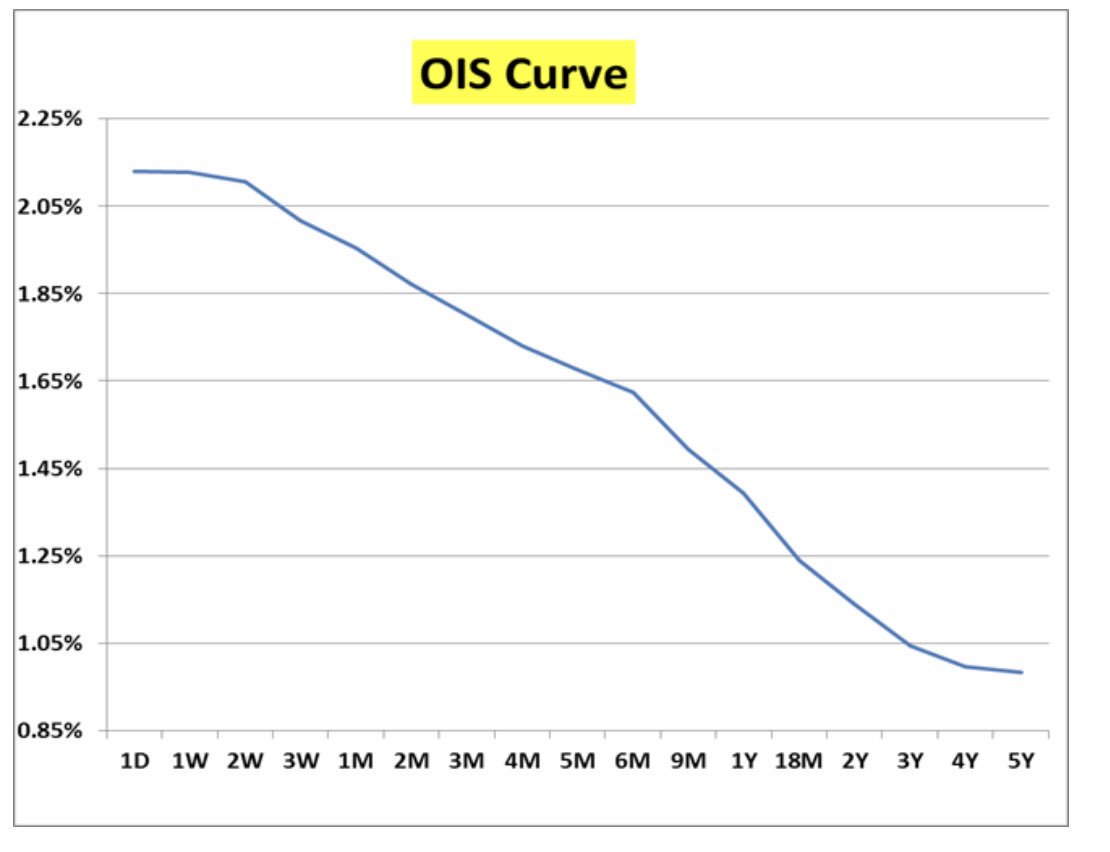

$JPM ‘s Net Interest Income dot plot needs 2 be recalibrated downwards...they originally predicted 4 hikes in ‘18 that worked.. but GDP couldn’t handle & now $TLT & OIS Curves say they r all coming back & some. Will bank capitulate? Likely over time. Let’s c.

@TeddyVallee $XLF

@TeddyVallee $XLF

If $JPM doesn’t.. equities will end up marking to market their NII as per bonds..which just on 1st order basis is >50% of its total revenues... meanwhile FICC, Equity trading & Banking fees not looking that gr8 either according to others.. Loan/Retail Deposit growth weak as well.

$TLT to the moon & mortgage production benefited from stronger refi (that burns out).. & MSR valuation losses offset as prepay speeds gap up & cash flows down.. XS servicing cash now gets lower IRR on front end reductions.. meanwhile Purchase Apps lackluster vs. plummeting rates.

So that leaves you with cycle low credit costs (ex Cards that continue 2 rise) & a better tax rate that’s already in YoY comps..House price HPI rolling over so legacy resi re reserve releases are done which was Card NCO offset..

& now oil & shale rolling over.. so expect more C&I Criticized Loans & DQs to rise in 2H19 & 2020... Cards are a big driver of Cycle Credit Losses.. real losses further amplified as jobs slow.. & CECL accounting kicks in 2020.. Reserves up big..

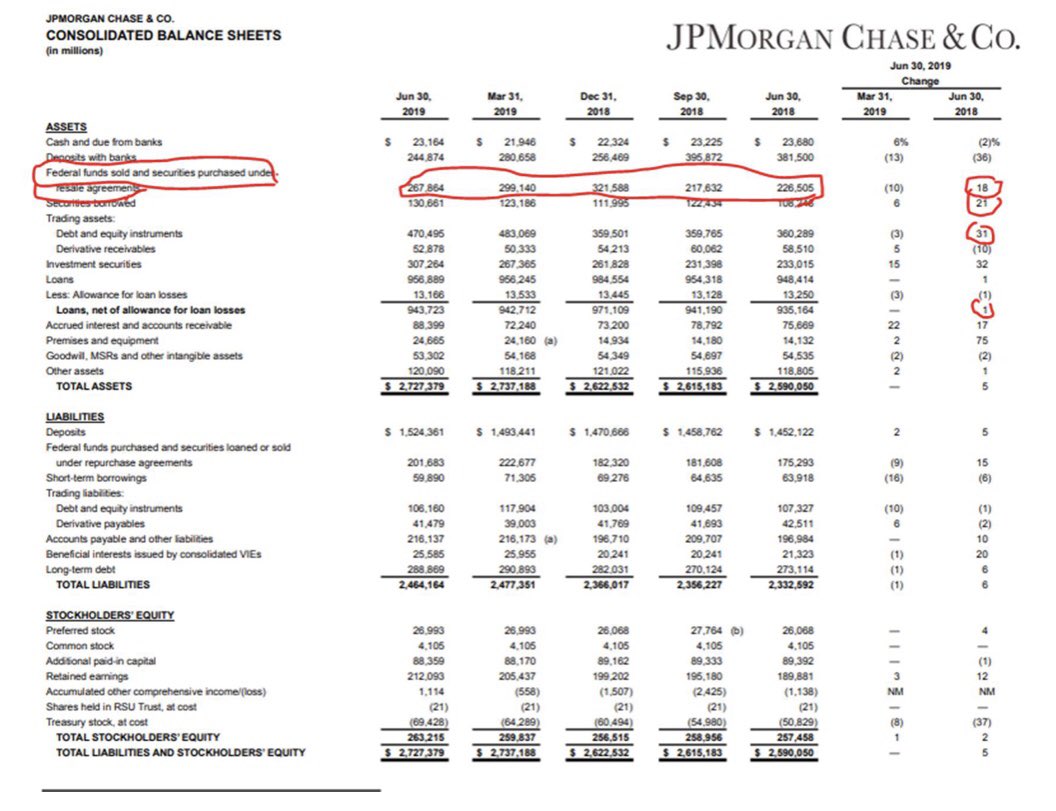

But in 4Q18 $JPM unleashed their cash..64% of HQLA at time.. & funded basket case $EUFN $XLF & $EUFN banks for LCR liquidity (Reverse Repo Bridge Loans) & Reversed in $TLT & bot a huge amount of $TLT themselves for their RLAP.... but barely grew loans by a meager 1% YoY...

What does that tell you about our US economy.. if $JPM the lender of 3rd last resort (after Fed & FHLB)... is growing their liquidity book like a weed but can’t even grow their loan book by > 1% YoY? Banks sell $DXY money (loans/volume) at a price (rates).. both stink. $XLF

But being being lender of 3rd last resort comes w a price. $JPM LCR ratios have deteriorated substantially as have most GSIBs..with $DXY liquidity drain coming coz of TGA cash build to $410B they should deteriorate further.. & constrain b/s capacity w no GSIB Surcharge relief...

So...how do we solve this problem?

The solution (no good ones) is a problem for $JPM $XLF & $KRE..The Fed has to end up re liquifying the system & slashing front end rates..that eventual Bull Steepening kills NII & risk adjusted returns that further constrains b/s deplolyment.

The solution (no good ones) is a problem for $JPM $XLF & $KRE..The Fed has to end up re liquifying the system & slashing front end rates..that eventual Bull Steepening kills NII & risk adjusted returns that further constrains b/s deplolyment.

Jamie Dimon now at Barclays Fin:

Reducing NII for 2019... by $500MM to ~$57Billion... that’s just for this year.. talking about cutting expenses as an offset... now saying see Q Disclosure down $2.7B for 2020 NII.. “if we go into recession it will be far worse than that.” $JPM

Reducing NII for 2019... by $500MM to ~$57Billion... that’s just for this year.. talking about cutting expenses as an offset... now saying see Q Disclosure down $2.7B for 2020 NII.. “if we go into recession it will be far worse than that.” $JPM

Less overly bullish talk on economy more on superior mouse trap.

BN: “JP Morgan loan growth is no longer outpacing peers.”

“ $JPM is cautious on C&I & CRE Loans.”

“Risk in JPMs China expansion has increased.”

BN: “JP Morgan loan growth is no longer outpacing peers.”

“ $JPM is cautious on C&I & CRE Loans.”

“Risk in JPMs China expansion has increased.”

Dimon talked a bunch about LCRs & GSIB Buffers being heavily constraining for $XLF & $JPM balance sheet capacity & the dearth of liquidity in Stress...essentially saying no relief in sight as of today.. basically saying “watch out” vol is coming.. & said get ready for it. $TLT

1) Jamie Dimon: “I wanted to mention one thing when we look at LCR... in talking about monetary transmission policy...u see recently China changes reserve requirements .. & they do that & it frees up $100B of Lending.. WE CAN’T DO THAT HERE BECAUSE OF LCR...

2) “It has nothing to do with monetary policy... but conflicting regulatory policy.. LCR also means I can’t finance a corporate bond & include that as liquidity anywhere... so when you all are selling corporate bonds & one day u want $JPM take on & finance $1Billion... I CAN’T.”

3) “It will immediately affect those ratios (LCRs)... so we have taken liquidity out of certain products.. so it won’t hurt you in good times..but WATCH OUT when times get bad.. & people get Stressed a little bit.”

4) He was asked if DC regulators understand these $DXY liquidity issues & will address them:

“I think some folks r very smart.. but it’s so political & so much is going on ... my own view is they (LCRs/GSIB Scores) aren’t going to be addressed...JUST PREPARE FOR IT”

$DXY $TLT

“I think some folks r very smart.. but it’s so political & so much is going on ... my own view is they (LCRs/GSIB Scores) aren’t going to be addressed...JUST PREPARE FOR IT”

$DXY $TLT

5) “Volcker Rule changes may at the margin improve trading liquidity a bit...I think far more important impact on liquidity is LCR & how GSIFI (GSIB Surcharges) looks at Repo.. & those things wlll hurt system in downturn...it will b much harder 4 banks 2 intermediate a downturn.”

6) “Regulators have to look at how America Gold Plated everything... LCR & GSIFI & a bunch of other rules... that’s ok in short term..but needs 2 be harmonized.. doubling down on GSIFI Surcharges isn’t sustainable.”

He has now capitulated on SCB..

(Stressed Capital Buffer)

He has now capitulated on SCB..

(Stressed Capital Buffer)

“Stressed Capital Buffer” is the way to go”

—> btw this is very bad for $MS & $GS b/s deployment that has very little room on this Buffer.. which is predicated on peak to trough decline in the DFAST Stress tests for CET1 ratios in Fed Severely Adverse Case.. but I digress...

—> btw this is very bad for $MS & $GS b/s deployment that has very little room on this Buffer.. which is predicated on peak to trough decline in the DFAST Stress tests for CET1 ratios in Fed Severely Adverse Case.. but I digress...

7) Astute Audience Question 4 Dimon:

“U have spoken about tightness of GSIB Scores & LCR which is true 4 u & other Primary Dealers.. do u think Fed acknowledges tightness on front end w more T Supply coming.. r they worried about the fact u r capped on your balance sheet?

“U have spoken about tightness of GSIB Scores & LCR which is true 4 u & other Primary Dealers.. do u think Fed acknowledges tightness on front end w more T Supply coming.. r they worried about the fact u r capped on your balance sheet?

8) Dimon Response:

“I think they r aware of it because they have seen the charts/graphs & stuff like that..& I think they know it’s true but fixable.. but it isn’t something they r worried about immediately.” 😳

My translation: Collateral Damage has 2 be bad..Fed behind Curve.

“I think they r aware of it because they have seen the charts/graphs & stuff like that..& I think they know it’s true but fixable.. but it isn’t something they r worried about immediately.” 😳

My translation: Collateral Damage has 2 be bad..Fed behind Curve.

9) The problem is if the Fed lowers GSIB Scores & LCR/RLAP 2 reduce front end tightness & further $TLT buying amplifying Curve Inversions they are trading $XLF Bank Safety (Basel/DF).. in an election year 2020..close 2 zero chance @RepMaxineWaters & @RepKatiePorter will allow it.

10) These scores r adjudicated by Fed & can be recalibrated by Fed & doesn’t need new legislation... BUT...that’s bad look 4 Fed in ‘20 Election season when Powell is already under assault from Trump to lower IOER.. & it’s late in Credit Cycle & they r already thinking CCyB 👆

11) Dimon on Loan Growth:

“Loan growth in CIB is episodic.. in the Commercial Bank we have very low loan growth in C&I & CRE... we r being cautious on that side.. that’s a decision we make.. less than some banks.. we aren’t outpacing other banks.”

Remember this? 👇 $TLT $XLF

“Loan growth in CIB is episodic.. in the Commercial Bank we have very low loan growth in C&I & CRE... we r being cautious on that side.. that’s a decision we make.. less than some banks.. we aren’t outpacing other banks.”

Remember this? 👇 $TLT $XLF

12) “Card book growing.. mortgages what’s on our b/s is up to us.. we make that decision...so right now we r REDUCING.. our on on b/s mortgages.. we r moving them so u see mortgage balances going down.”

“Although originations up”

My Translation: we like fees not risk on b/s..

“Although originations up”

My Translation: we like fees not risk on b/s..

13) Now remember in ‘17 & ‘18 when rates were rising & Purchase & Refi was getting pounded & Originations were getting crushed to the point $BAC took out the slide from its deck & GSIBs proclaimed they loved the “on b/s mortgage” risk..well now not so much.. Post Curve Inversion.

14) “It’s hard 2 manage b/s in a low rate environment..NII is what u look at.. Obviously u have to look at long run effect of those lower rates...There r certain businesses that don’t get affected at all.. but there r business that it just sucks into ur margin & little u can do.”

15) “I don’t think we have zero interest rates in the US but worth thinking about how to get prepared 4 it.. just in the normal course of risk management.”

“One can cut costs.. but u can charge a/c fees.. but u can’t cut consumers < 0%.”

“One can cut costs.. but u can charge a/c fees.. but u can’t cut consumers < 0%.”

16) $JPM reducing NII to $57B for FY’19..the other major things is if u go

to our Qs u will see -$2.7B negative impact 4 a 100bps shift in the Curve.. keep that in back of mind for 2020.”

to our Qs u will see -$2.7B negative impact 4 a 100bps shift in the Curve.. keep that in back of mind for 2020.”

17) “Far more important effect is the why... if we go into a recession you are going to be hurt far worse than that.” (NII impact)..Talks about offsets to NII if IOER gets slashed & no recessions..keep in mind there r v few instances when late cycle cuts - don’t end in recession.

18) There r very few instances when yield curve inversions - don’t end in recessions. $TLT $XLF

19) “One of risks in market.. not just going up or down but is the provider of liquidity or credit going to be there when spreads are +1,000 bps over... & I can guarantee u there will be whole chunks of them that won’t be there..some who can’t coz the company can’t afford it.”

20)”.. some who can’t afford to pay the price.. they will bankrupt them.. & they (non banks) can’t afford to roll over at a price a bank can.. because of huge marks (hits).”

Future Capex plummeting... no need to grow loans.. customers can’t sell inventory... weak sales will provide plenty of cash as inventories run down & conversion cycle - neuters any demand for $XLF loans at peak leverage... supply constrained by late cycle negative carry. $TLT

“That’s a decision we make.” - Indeed.

Also ur LCR/RLAPs almost require it as u spent ur cash funding $DXY dollar shortage w $XLF Rev Repo Loans since 4Q18 while fracking ur own cash reserves..deep water drilling..now same $XLE drilling guys r gonna need cash as $DXY👆FCF 👇

Also ur LCR/RLAPs almost require it as u spent ur cash funding $DXY dollar shortage w $XLF Rev Repo Loans since 4Q18 while fracking ur own cash reserves..deep water drilling..now same $XLE drilling guys r gonna need cash as $DXY👆FCF 👇