1) On Mon/Tue, I'll be doubling my $TSLA short position. This is not advice, just my Q3 estimates. Stock has risen on speculation that Q3 could see profits. But things aren't good. Even bulls like @ARKInvest are dumping lots of $TSLA shares & HFs in the "swing trade" dumping too.

2) I've changed my $TSLA model to focus on retail deliveries (ex-lease) & eyeball lease revs/gross profit. Note Auto Revs in Q1 & Q2 adjusted for RVG deferred revs of $501m & $64m, respectively. I subtract $65m from my Q3 revenue est for FX headwinds. But ASP is flat w/ Q2's.

3) Gross profit assumptions:

(a) COGS/Unit -1% QoQ on higher output

(b) Q1/Q2 COGS/unit adj for RVG

(c) FX headwinds: -$65m

(d) $200m in ZEV/GHG credit sales. No FSD est

*Q3 GM of 21% is flat QoQ despite higher ZEV/GHG credits & deliveries. FX headwind of -$65m is generous.

(a) COGS/Unit -1% QoQ on higher output

(b) Q1/Q2 COGS/unit adj for RVG

(c) FX headwinds: -$65m

(d) $200m in ZEV/GHG credit sales. No FSD est

*Q3 GM of 21% is flat QoQ despite higher ZEV/GHG credits & deliveries. FX headwind of -$65m is generous.

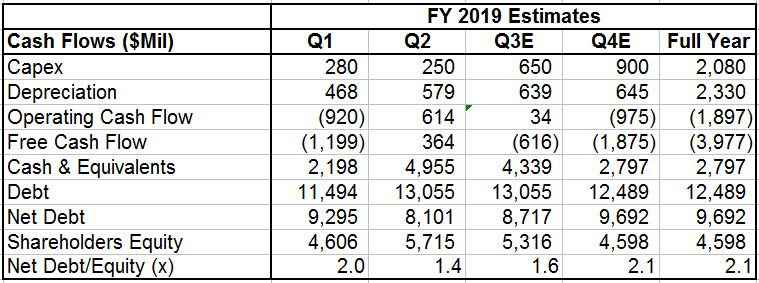

4) Q3 SG&A should be slightly up QoQ. While G&A comes down on the removal of restructuring, GF3 expenses start to weigh in & R&D should rise for Model Y early launch. Q3 adj Operating Losses (Ex-ZEV/GHG) deteriorate from -$279m in Q2 to -$301m in Q3 despite record deliveries.

5) Net interest expenses rise QoQ, but FX headwinds on overseas assets rise by $40m QoQ. Total Non-Operating Losses up by $55m QoQ to -$257m.

Q3 GAAP Net Loss is -$400m w/ EPS of -$2.23. Consensus is at -$213m & -$1.48. But FCF is the biggest focus & where consensus is way off.

Q3 GAAP Net Loss is -$400m w/ EPS of -$2.23. Consensus is at -$213m & -$1.48. But FCF is the biggest focus & where consensus is way off.

6) Model Y will be launched in Q1'20 & pro-$TSLA media already leaking the story. This will be the pump on next Wed's conf-call. This means capex should be at least $600m in Q3 after low levels of $265m in Q1 & Q2 (watch the huge capex spike in Q2'18 & Q3'18 ahead of M3 launch).

7) Accounts Receivable should also rise, given likely China "channel-stuffing" & 46% higher leases vs Q2. I'm calculating a +$320m QoQ rise in AR; slightly lower inventory (-$50m) & -$150m fall in Accounts Payable (the avg fall each Q since $TSLA began paying Pana back).

8) So it should be the -$616m in FCF that gets the stock to tank (consensus is at +$40m). Q3 revenues are factored in (at $6.37bn, it's lower than mine). Net loss is too optimistic & part of $TSLA's share price rise this month was due to speculation of a "slight profit".

9) Very few pumps that @elonmusk can use next Wed. Model Y news is already out & will only lead to a quicker demise of the Model 3 from Q1'20. GF3 might be on schedule, but we all know $TSLA must lower the local M3 price by 30% in order to sell planned 12.5K/month.

$TSLAQ

$TSLAQ

@elonmusk Erratum in 6): I have the wrong quarters for capex spike ahead of the Model 3 launch.

It was Q2'17 & Q3'17 when capex hit $959m & $1.1bn, respectively, as the Model 3 was launched.

Model Y said to be cheaper, but still needs more capex from Q3'19.

It was Q2'17 & Q3'17 when capex hit $959m & $1.1bn, respectively, as the Model 3 was launched.

Model Y said to be cheaper, but still needs more capex from Q3'19.