1/ This is a thread for weird stuff that's hard to explain. IMO, there's a lot evidence against the random walk and CAPM interpretations of EMH.

That suggests that finance has the same issues as other fields in finding a model that works both conceptually and empirically.

That suggests that finance has the same issues as other fields in finding a model that works both conceptually and empirically.

2/ Professional stock analysts tend to be worse than random forecasters. (This is exploitable: Buying their sell recommendations and shorting their buy recommendations has had alpha in the S&P 500 universe over the past 15 years after transaction costs.)

3/ Value and momentum are negatively correlated, but both have positive returns. Tail risk historically hasn’t been sufficient to explain why this is the case:

4/ Time-series momentum pays the investor a positive return for partial tail risk protection. This is due to time-series autocorrelations in stock and commodity returns, as the returns *don’t* randomly walk.

5/

6/ Value doesn't seem to be a compensation for risk (based on accounting data). The highest-quality value stocks, ex-ante, also produce the highest returns.

Using Piotroski's quality definition:

Using AQR's more robust definition:

Using Piotroski's quality definition:

Using AQR's more robust definition:

7/ Value also doesn't seem to have "short vol" properties when its historical tail metrics are examined.

*Long* thread below:

*Long* thread below:

8/ There are other factors, most notably momentum, that do have poor tail metrics (negative skewness and high kurtosis).

However, the combination of value and momentum (negatively correlated factors) seems hard to explain using risk-based arguments.

However, the combination of value and momentum (negatively correlated factors) seems hard to explain using risk-based arguments.

9/ CAPM is based on high risk = high return. That doesn't seem to be true for either value or the combo of value and momentum.

CAPM is also more broadly false: low-risk (low volatility, low beta) stocks have equal or higher returns.

Betting Against Beta

papers.ssrn.com/sol3/papers.cf…

CAPM is also more broadly false: low-risk (low volatility, low beta) stocks have equal or higher returns.

Betting Against Beta

papers.ssrn.com/sol3/papers.cf…

10/ Embedded Leverage

(Long-dated options, which have lower risk, have better returns.)

papers.ssrn.com/sol3/papers.cf…

Capitalizing on the Greatest Anomaly in Finance with Mutual Funds

researchgate.net/publication/25…

Volatility Effect: Lower Risk Without Lower Return

papers.ssrn.com/sol3/papers.cf…

(Long-dated options, which have lower risk, have better returns.)

papers.ssrn.com/sol3/papers.cf…

Capitalizing on the Greatest Anomaly in Finance with Mutual Funds

researchgate.net/publication/25…

Volatility Effect: Lower Risk Without Lower Return

papers.ssrn.com/sol3/papers.cf…

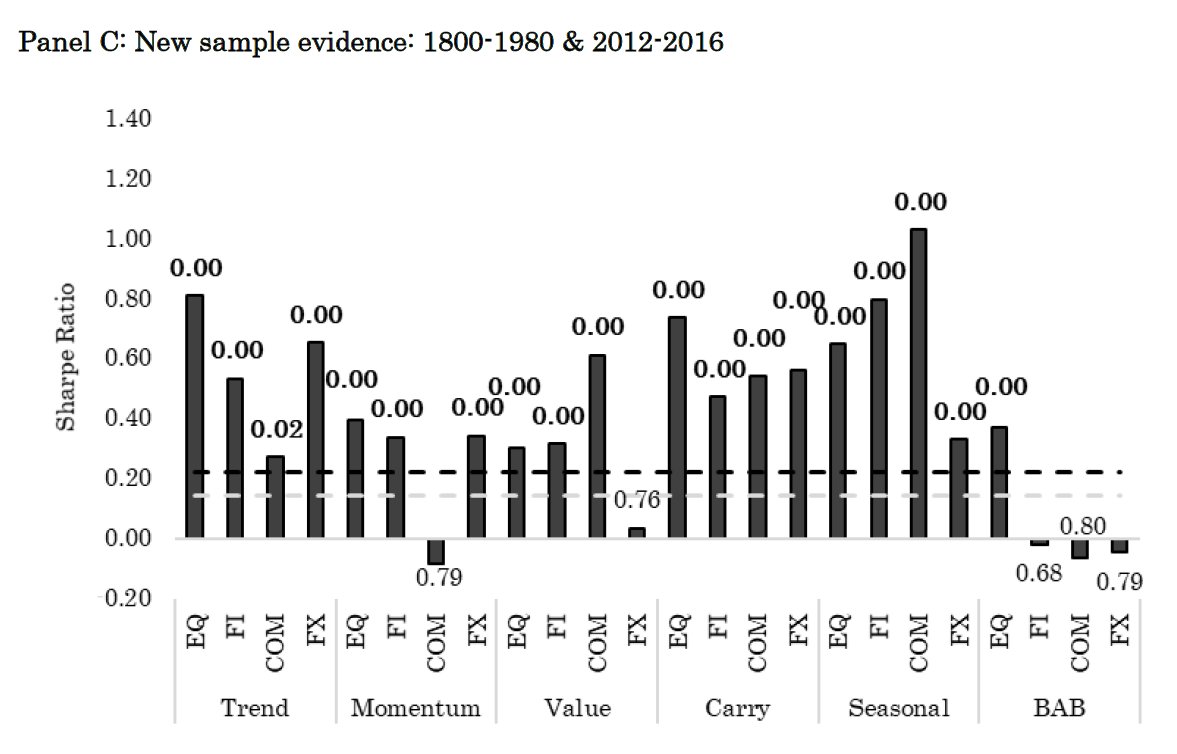

11/ Using value+momentum+carry+defensive in out-of-sample assets classes + a longer sample, AQR finds

* some evidence of data mining

* no evidence factors have been arbed away

* no evidence that factors as a whole are compensation for macroeconomic risk

* some evidence of data mining

* no evidence factors have been arbed away

* no evidence that factors as a whole are compensation for macroeconomic risk

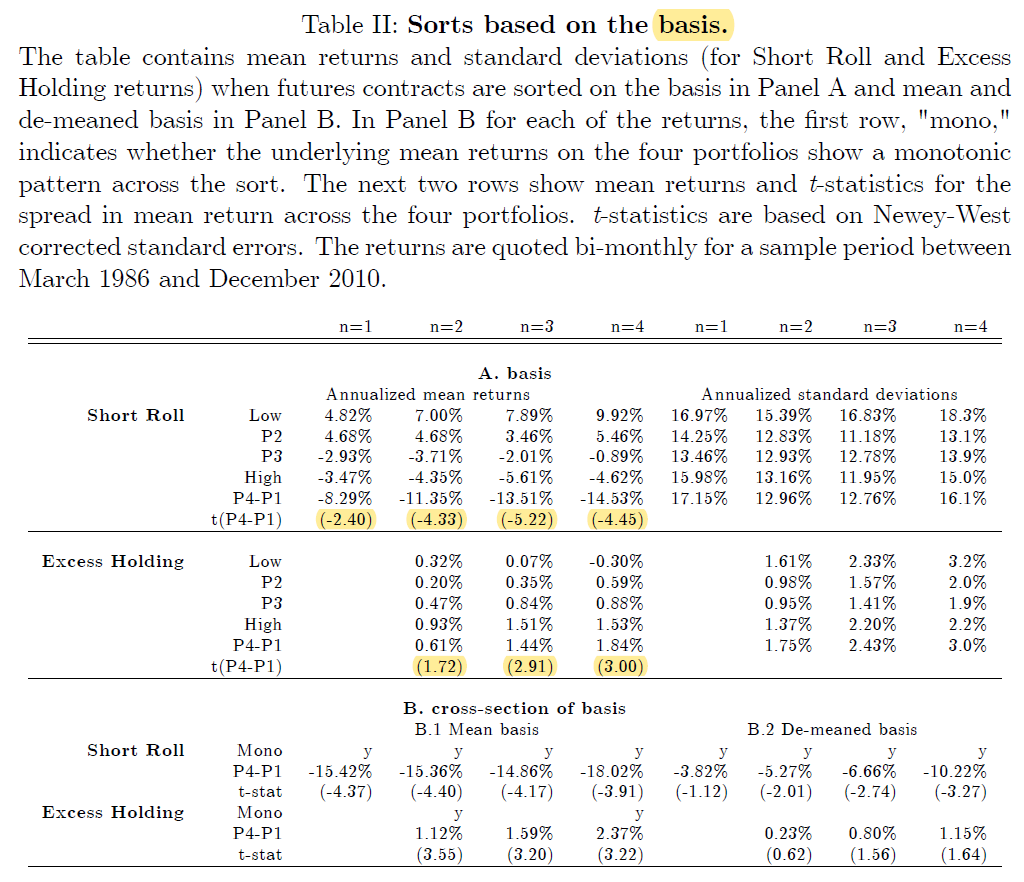

12/ New paper: the short legs of factors add no value to the long legs.

In other words, shorting stocks is expensive, hard to manage, less diversifying, and more prone to tail risk, but these risks are compensated by *negative*, not positive, returns.

In other words, shorting stocks is expensive, hard to manage, less diversifying, and more prone to tail risk, but these risks are compensated by *negative*, not positive, returns.

13/ There seems to be some truth to Buffett-style investing: less risk = same or better returns.

Indeed, his alpha can be explained by the factors in this thread, but to the extent that factors are not compensation for risk, EMH is still problematic.

Indeed, his alpha can be explained by the factors in this thread, but to the extent that factors are not compensation for risk, EMH is still problematic.

14/ Here are some papers that look at the valid data mining concerns that have been brought up:

Global Factor Premiums

(This goes *really* far back to when trading costs were higher, so it addresses data mining but not "factors will disappear" objections)

Global Factor Premiums

(This goes *really* far back to when trading costs were higher, so it addresses data mining but not "factors will disappear" objections)

15/ Conservative Formula: Quantitative Investing Made Easy

(Here, only price data, not accounting data, is allowed for factor definitions.)

Dual Momentum – A Craftsman’s Perspective

(Stability across factor definitions)

(Here, only price data, not accounting data, is allowed for factor definitions.)

Dual Momentum – A Craftsman’s Perspective

(Stability across factor definitions)

16/ Trends Everywhere

(Trend following examined using new contracts, including VIX and VSTOXX futures)

Commodity Futures Risk Premium: 1871–2018

(New database, built from newspaper data, for commodity strategy tests)

(Trend following examined using new contracts, including VIX and VSTOXX futures)

Commodity Futures Risk Premium: 1871–2018

(New database, built from newspaper data, for commodity strategy tests)

17/ Carry

(A consistent definition for carry is tested across asset classes along with a logical variation that also works)

(A consistent definition for carry is tested across asset classes along with a logical variation that also works)

18/ Equity factors also earn more of their returns on earnings and news days than on other days (even after controlling for the stocks' same-month returns)... so factors may have "early" information that gets more fully priced in when news is released.