Why do people buy #LIC policy when returns are so bad? Long thread: As LIC goes towards divestment, let’s see what makes it policies click. It could save you a fortune, if you get the spirit behind this thread. Please keep your humor cells intact while reading. Let’s begin:

(1) Indian custom to buy LIC, passed through generations: LIC has the most entrenched network of 12 lac advisers & a legacy of 60 plus yrs. It has become customary to buy LIC. Your dad is bound to recommend the you same once you get your first salary.

However, fact is that the times when average returns from LIC were considered good (1950s-1980s) are long gone.With inflation running 9% for a decade in 2000s, LIC plans have been a big value destroyer.Unfortunately, it takes 20 yrs for you to even realize you lost money on LIC

So, most people don’t even understand the sub 5% returns I am talking about from LIC plans. Ever wondered why you dad makes such a hard-sell for LIC ? Try to surrender a plan after few years & you’ll know.

You can get out of a marriage, but not LIC. Its is a life partner that you can never leave, even if you want to. The 13th month persistency of 66% indicates that 1 in every 3 buyers never pay the 2nd year premium. Why such high dropouts ? We’ll see below.

(2) The great Indian social obligation:

#LIC agent is a known social person in locality. It becomes almost obligatory to buy policy from agents, even if you didn’t understand the policy. If each agent knows 100 “relatives”, we almost have the half of Indian households covered.

#LIC agent is a known social person in locality. It becomes almost obligatory to buy policy from agents, even if you didn’t understand the policy. If each agent knows 100 “relatives”, we almost have the half of Indian households covered.

So, you can’t escape an LIC agent. He’s one of you & you may not even know it. However, what is the adviser’s interest in pushing these plans ? Of course, LIC has one of the best in commission payouts largely because of the nature of the policies sold (opaque traditional plans)

What’s worse, there is no accountability on returns since most plans work on 20 plus yrs tenure. So, you can’t even confront agent after few years of “non-performance” like you can in case of ULIP/market linked plans. You tend to feel that your investments are great & guaranteed.

(3) The same old (mis) selling pitch:

This is the best trick up their sleeve. Majority of (tempted to say all) LIC agents have a similar selling pitch.They almost never talk to you about “annualized returns”. The pitch is “your money grows 4 times in 20 yrs or 6 times in 30 yrs”

This is the best trick up their sleeve. Majority of (tempted to say all) LIC agents have a similar selling pitch.They almost never talk to you about “annualized returns”. The pitch is “your money grows 4 times in 20 yrs or 6 times in 30 yrs”

Most people can’t calculate what the annualized % returns are. Fact is - most returns are 3.5% to 5% at max. A bank FD would be much better despite taxes. But it is never stated clearly on paper & the agent gets away by quoting “additional bonus” & other throwaways.

No clear track record of past annual returns % at policy level is disclosed by LIC. This tacitly helps the agent & LIC supports this by not taking any efforts to curb mis-selling of returns.

Considering 99% plus plans from #LIC are endowment kind, who will buy any policy if it were known that returns are 5% only? So they never get published. This is true of even private life insurers offering traditional plans. You get absolutely poor returns, guaranteed of course!

(4) The smart financial buyer (or so he thinks):

The buyer thinks he's being smart by taking a small % of the commission from agent. What he certainly doesn’t know is that the “cut” he takes in first year is just a small fraction of the money agent will make in trail commissions

The buyer thinks he's being smart by taking a small % of the commission from agent. What he certainly doesn’t know is that the “cut” he takes in first year is just a small fraction of the money agent will make in trail commissions

While reading this, some are still thinking that their policy is something unique.Others may get poor returns but their “Jeevan blah blah” is the chosen one for select few & will get special bonuses. We always overrate our own investments. But did u know it before agent sold you?

Average life cover of 1.6 lac per policy indicates customers are not getting much life protection either (LIC has 29 cr policies with 46 lac cr life cover). Aside, buying #LIC doesn’t make you a genius. You do what 2 crore plus Indians do every year. Still unique? Interesting!

(5) Seeking guarantees in life at any cost:

Now this one has some cultural history. Indians have been duped so much by notorious private investing firms that anything from the govt gives us comfort. I understand that there is a notion of implied govt guarantee in LIC.

Now this one has some cultural history. Indians have been duped so much by notorious private investing firms that anything from the govt gives us comfort. I understand that there is a notion of implied govt guarantee in LIC.

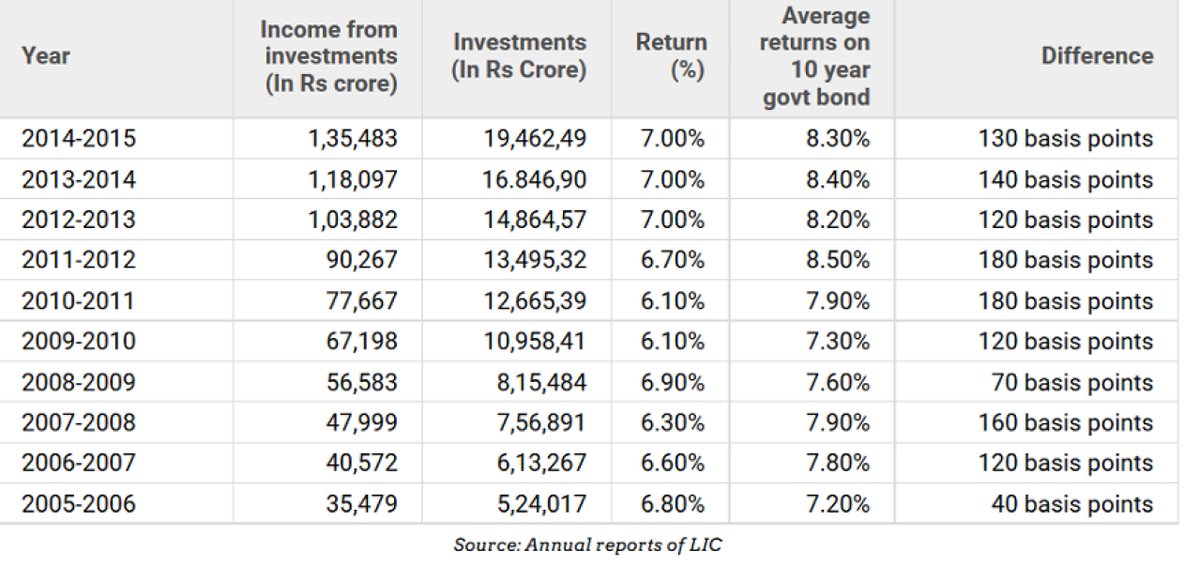

However, this is like saying that your money is safer in SBI & not in private banks !! Really ? And what is the guarantee after all when all you get is sub 5% return? Look at the historical returns that LIC has earned on its investments since 2005.

LIC earns just 7% or below (Table courtesy @kaul_vivek ) when average returns of govt bonds were 8.4% . And the inflation during this period was averaging 8.85%. All because of the high cost structure of LIC.

Add commissions to this & you realize that all you make is a good 30% less than the govt bonds! So hell yes, count all bonuses that you like, you are guaranteed to get poor returns, no matter what “Jeevan something” you hold. So much cost for the guarantee !

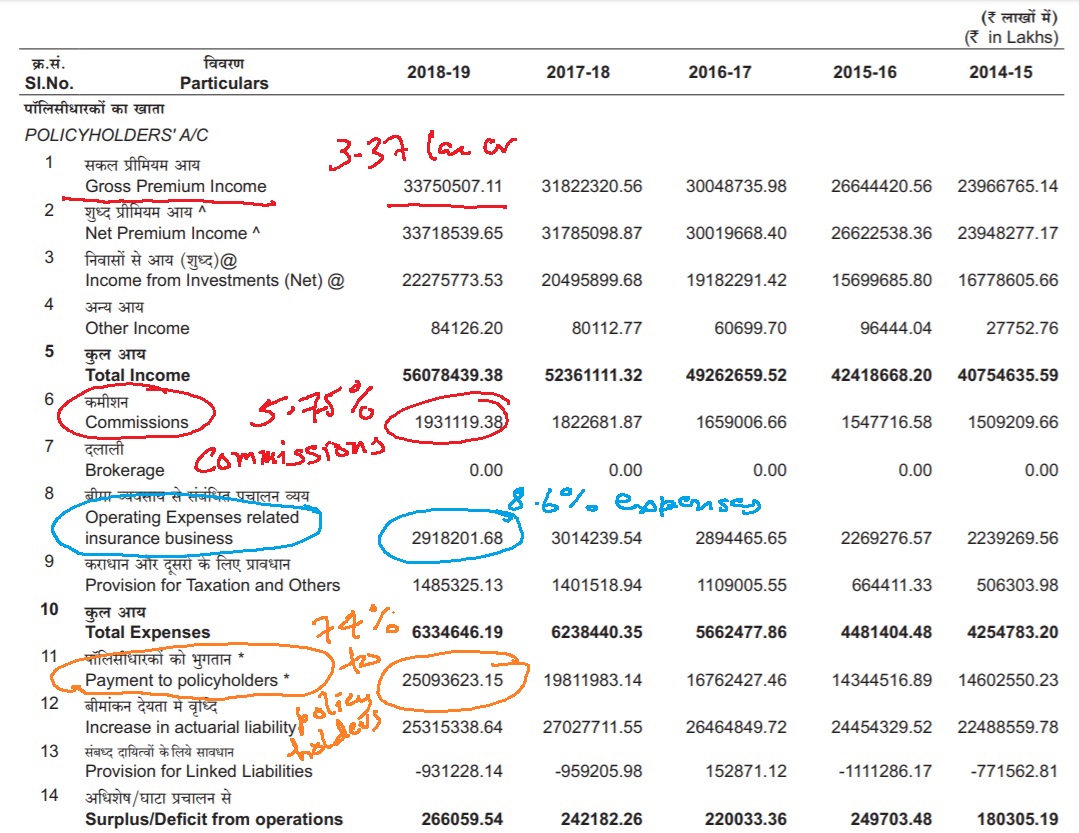

Return to shareholders: Finally, something about the return to shareholders, now that we’re looking at listing & stake dilution of #LIC. The 2019 balance sheet has few observations for policy holders(who are the current shareholders in a way) & the future shareholders in markets

We see that policy holders pay almost 6% in commissions every year & about 9% in operational expenses. This is gross in-efficiency for a investing firm. Add to this the NPA losses of 6.15% (yes, NPA) & we’re looking at a huge 20% shaved off from the premiums paid.

As @monikahalan writes, #LIC market listing would bring out an interesting clash between the interests of policy holders & those of the new shareholders. However, looking at the investing sense of policy holders, looks like shareholders will clearly win this round.

n/n If LIC plans made you rich, India would have been a developed nation by now. There is nothing “intelligent” about buying an LIC policy. Something majority Indians do without thought is never going to make you rich. Looks like even this is too difficult to understand for most.

Detailed answer on Quora. quora.com/Why-do-people-… . If you have a LIC story to share, pls do.