1/ Carry Investing On the Yield Curve (Martens, Beekhuizen, Duyvesteyn, Zomerdijk)

"Global curve carry has strong performance that cannot be explained by other factors. Bond BAB has no added value for an investor who already invests in curve carry."

wp.lancs.ac.uk/fofi2018/files…

"Global curve carry has strong performance that cannot be explained by other factors. Bond BAB has no added value for an investor who already invests in curve carry."

wp.lancs.ac.uk/fofi2018/files…

2/ * Bonds are from 10 countries (multiple maturity buckets)

* Choice of funding rate (Eurocurrency vs. US T-bill) matters: duration-neutral portfolios are not self-funding

* Curve carry includes the funding rate in its signal, but BAB (applied to the curve) does not

* Choice of funding rate (Eurocurrency vs. US T-bill) matters: duration-neutral portfolios are not self-funding

* Curve carry includes the funding rate in its signal, but BAB (applied to the curve) does not

3/ "In the U.S., we see more carry per unit duration in lower-maturity buckets: the curve is steeper at the short end.

"Carry differences between the buckets are much larger for T-bill rates than for Eurocurrency rates, leading to larger differences between excess bond returns."

"Carry differences between the buckets are much larger for T-bill rates than for Eurocurrency rates, leading to larger differences between excess bond returns."

4/ "Carry is a strong predictor of expected return differences between different-maturity bonds.

"The curve carry strategy positions itself in maturity buckets where the most yield increases are expected, but not all the increases materialize."

10 countries→diversification

"The curve carry strategy positions itself in maturity buckets where the most yield increases are expected, but not all the increases materialize."

10 countries→diversification

5/ "For most international bond markets, the betting-against-beta strategy works for the low funding rate based on T-bills. But the strategy does not work when using the higher Eurocurrency rates as funding rate."

6/ "Investors should opt for curve carry and ignore the low-maturity (BAB) effect, especially when facing Eurocurrency rates as the funding rate rather than T-bill rates.

"Curve carry takes the funding rate into account when choosing between maturity buckets."

"Curve carry takes the funding rate into account when choosing between maturity buckets."

7/ "Carry and yield pick-up are highly correlated (0.95), but the alpha of carry is still significant at the 5% level, while the alpha of yield pick-up is no longer statistically significant.

"We can conclude that carry improves over yield pick-up."

"We can conclude that carry improves over yield pick-up."

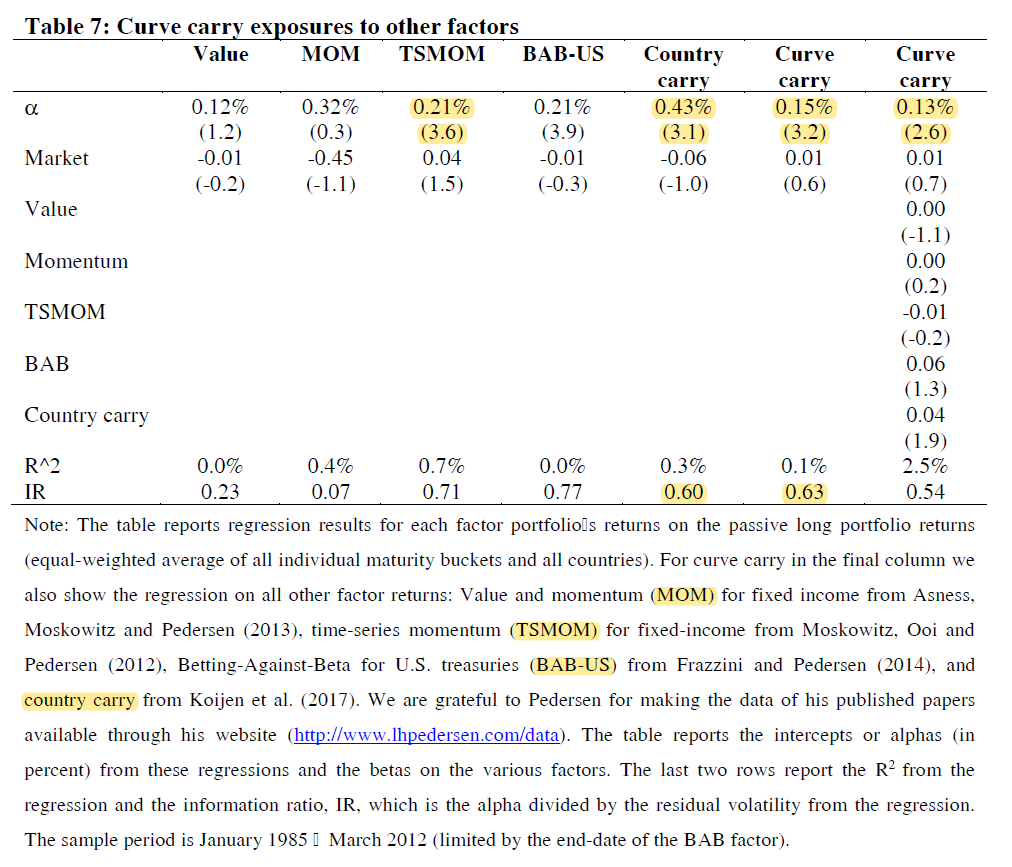

8/ * Value and cross-sectional momentum (Asness et. al.) have an insignificant alphas for government bonds

* TSMOM (Moskowitz et. al.) and country carry (Koijen et. al.) may be useful

* Curve carry survives controlling for the other factors, although it loads on country carry

* TSMOM (Moskowitz et. al.) and country carry (Koijen et. al.) may be useful

* Curve carry survives controlling for the other factors, although it loads on country carry

9/ Links to the aforementioned papers:

Value and Momentum Everywhere (Asness et. al.)

(findings for bonds)

Time-Series Momentum (Moskowitz et. al.)

Carry (Koijen et. al.)

Value and Momentum Everywhere (Asness et. al.)

(findings for bonds)

Time-Series Momentum (Moskowitz et. al.)

Carry (Koijen et. al.)

10/ "Curve carry shows excellent results for the U.S. in a period of rising yields. Combined with the main 10-country results from 1986 to April 2017, this shows that the curve carry premium is significant in both bull and bear bond markets."

11/ "Curve curry is, on average, wrongly positioned during central bank actions. Half of the losses due to yield changes can be explained by negative returns during central bank actions."