W/ @deepa_driver's JEP submission, it appears to me, on closer inspection, that @USSbriefs has gone back in time & devoured the children of their own, i.e., @FirstActuarial's & @Dennis_Leech's, recommended approach to the #USS valuation! Can @Sam_Marsh101 disconfirm? More below.

I.e., I'm finding it difficult to reconcile @deepa_driver's critique of #USS embodied in Point 1 of linked @USSbriefs manifesto w/ the manifesto endorsement in Point 3 of @FirstActuarial's & @Dennis_Leech's recommended approach to the 2017 valuation. 1/

medium.com/ussbriefs/a-ma…

medium.com/ussbriefs/a-ma…

This is #USS's justification, and that of their scheme actuary, of the approach followed back then: 3/

Contributions can be kept relatively low via a portfolio weighted towards return-seeking assets (equity). Funding deficits caused by the resulting asset volatility are not cause for concern, given positive cashflow & long-term perspective of ongoing nature of scheme. 4/

👆The above is, of course, very similar to FA's recommended approach. This is no accident, since FA is sympathetic to the prelapsarian days of actuarial practices of valuing ongoing DB schemes, before the rise of mark to market financial economics. 5/

So it appears that the @USSbriefs manifesto is trying to have its cake and eat it too, via its combination of Points 1 & 3. That's my main message. I'll close this thread here but add some footnotes w/ textual documentation later. 6/6

Link to long subthread, where I reply to @Sam_Marsh101's claim that past valuations can be differentiated from the recommended approach for 2017 on grounds that past valuations used more optimistic discount rates.

I now comment below on this embedded tweet of @Sam_Marsh101's:

Reply: The same can be said of scheme members: it suits us to employ one valuation methodology to argue that the status quo can be maintained w/ No Detriment (including no rise in contributions) & then shift to another to argue that employers underpaid in the past. 1/

Scheme members need to display the honesty and self-awareness to acknowledge that accusations of confirmation bias and bad faith can justifiably be levelled at us as well as at our employers. 2/2

The more I read the USS valuations from 1999 to 2005, the more I am struck by how similar #USS's approach and that of their scheme actuary were to the approach that @FirstActuarial is now recommending. Some examples: 1/

From USS's 2005 valuation: 2/

Note the affinities between the above smoothed approach to setting the contribution rate and the following recommendation of @FirstActuarial's in their submission to the September consultation: 3/

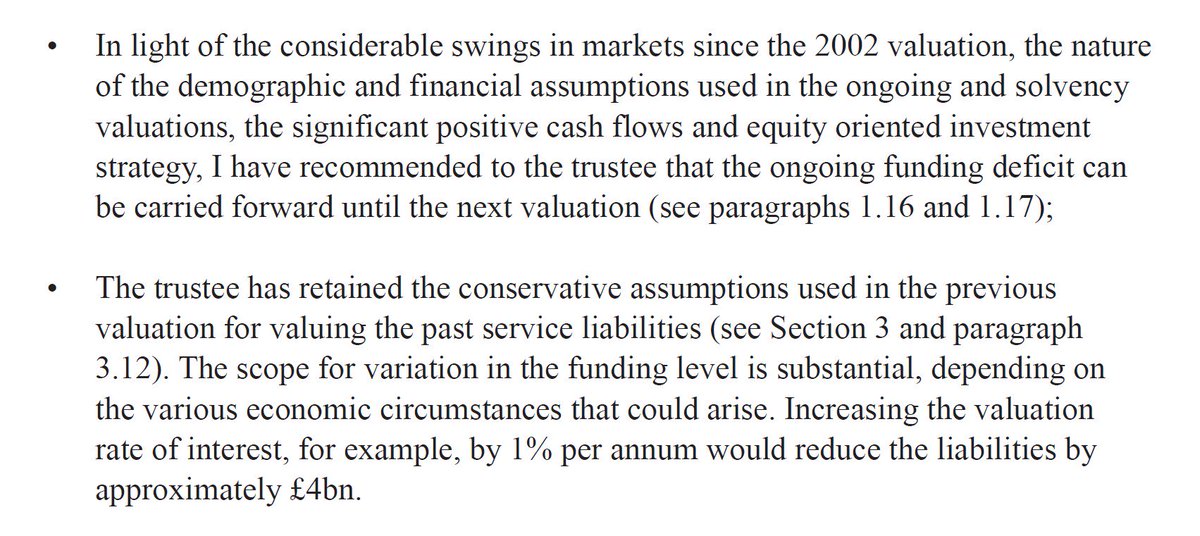

Note that in 2005, #USS recorded a £6.5 bn deficit, which was enormous in comparison with the size of the scheme, giving rise to a jaw dropping funding level of only 77%. 4/

By contrast, #USS's current £7.5 bn deficit, which critics dismiss as illusory and merely notional, gives rise to a much higher level of funding of 89% (given how much greater the asset value is now compared to back then). 5/

Did the £7.5 bn 2005 deficit cause #USS to go into a panic and call for either huge cuts to benefits or massive rises in the contribution rate? No! This was their response: 6/

In other words, #USS's response was that we should keep calm and carry on at current benefit and contribution levels. No Detriment! Swings in the market value of the assets were of little concern, given the cashflow positive nature of the ongoing scheme.... 7/

...and the likely returns on the equity-weighted portfolio. They also note that we shouldn't make drastic changes on the basis of such volatile large numbers that don't reflect the underlying nature of the scheme. 8/

These are exactly the sort of points that @FirstActuarial, @Sam_Marsh101, and @Dennis_Leech have been pressing for this valuation. 9/

By contrast, @deepa_driver has this reaction to the 2005 deficit: "Data provided at the next triennial valuation in 2005 confirms that this was a misguided and risky strategy, with a deficit of over £6.5bn accruing as a result." 10/

medium.com/ussbriefs/a-br…

medium.com/ussbriefs/a-br…

Also by contrast, @deepa_driver is critical of #USS's heavy investment in equities and regards the fall in their price after the dot bubble burst as cause for alarm regarding the prudence of #USS's investment strategy. 11/

So we have gone through the looking glass and into Alice's wonderland, where @USSbriefs is taking the same sort of stance towards the 2005 deficit and the scheme's investment in equities that the critics whom they dismiss as doom-mongers take towards today's deficit,... 12/

...which @USSbriefs dismisses as a phantom, an illusion. And we see #USS taking the same approach to scheme funding back then that @FirstActuarial, @Dennis_Leech, and @Sam_Marsh101 are urging #USS to take today. 13/13

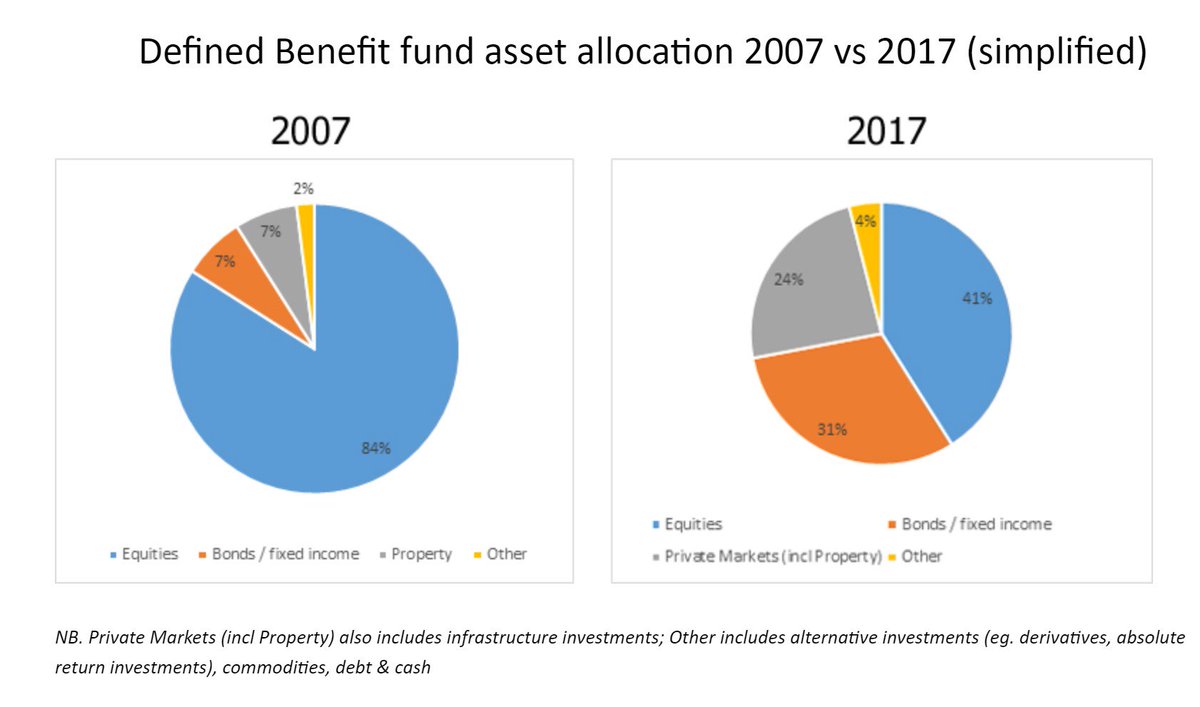

Higher expected returns back then were justified by the fact that the portfolio was then much more heavily invested in return-seeking assets -- i.e., the investment strategy was then more in line w/ what @FirstActuarial recommends for an ongoing scheme such as #USS! 2/2

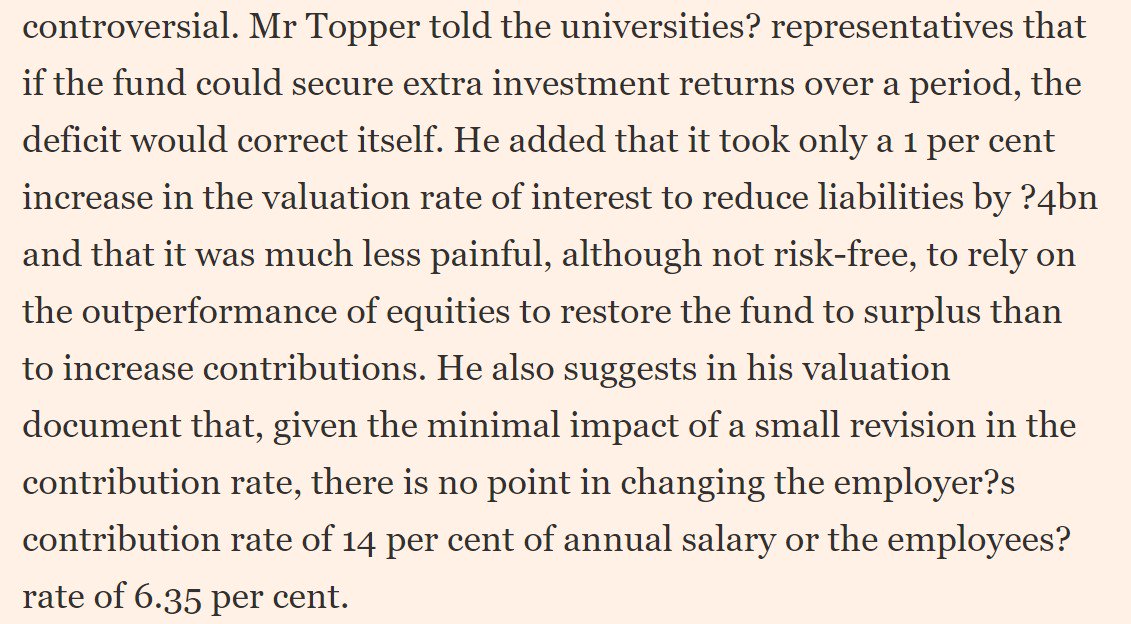

2006 FT article w/ scheme actuary's defence of not raising contribution rates: 1/

Scheme actuary's defence (cont.) 2/

And see this defence by #USS's CIO of their equity-weighted portfolio. This could have been written by @Sam_Marsh101, @Dennis_Leech, or Marion Hersh!: 3/

Note that, as of the 2008 valuation, 1st under Pensions Act 2004 regulations that still apply, #USS appears in fine shape. Contributions up to 16%, but technical provisions funding level is 103% (£0.7 bn surplus) for scheme that's 1/80th DB final salary on all salaries. 1/

Moreover, the scheme is even *more* well funded -- 104% -- on an FRS 17 basis, where the discount rate is AA corporate bonds. This is the discount rate that @JohnRalfe1 maintains is the correct one. 2/

So it appears that #USS has returned from it contribution holiday in good financial shape, both by the measure of its own valuation methodology and by John Ralfe's preferred measure. 3/3

Link to a new thread on this: