2/ Most of the property indices for various cities across Canada are flat or declining over the last 1 month, 3 month, 6 month and even 12 month periods.

However, they are up substantially in the last 3 to 5 years. Congratulations to those who made some serious money!!!

However, they are up substantially in the last 3 to 5 years. Congratulations to those who made some serious money!!!

3/ Majoirty of the die hard capital market investors are NOT flexiable enough to understand real estate’s power.

Mortgages (leverage) are a common use when investing property.

This isn’t anywhere as risky as a broker’s margin, because public assets have huge volatility.

Mortgages (leverage) are a common use when investing property.

This isn’t anywhere as risky as a broker’s margin, because public assets have huge volatility.

4/ A few days ago I did a thread on compound interest & aiming for a 15% CAGR. Some asked how is this possible?

If the property market in your area rises 5% p.a. but you have an investment with 80% LTV — your gross return will be 25% p.a.

After costs, taxes & fees maybe 15%!

If the property market in your area rises 5% p.a. but you have an investment with 80% LTV — your gross return will be 25% p.a.

After costs, taxes & fees maybe 15%!

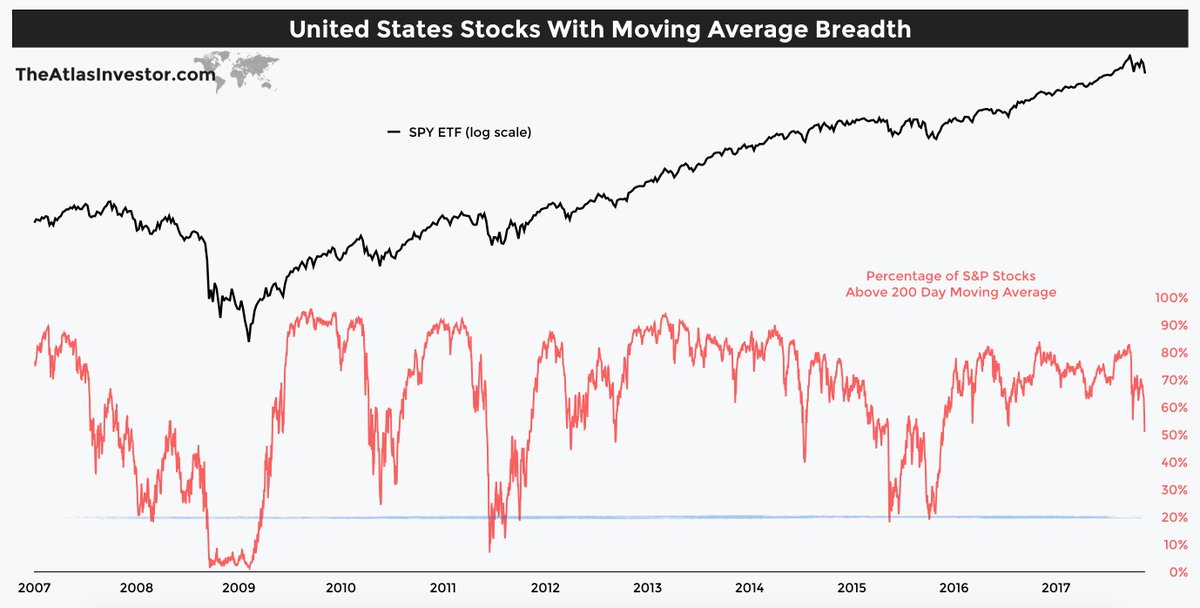

5/ Most of the people will say this is too risky, point to the 2008 global crash & claim debt use like that is dangerous.

These are the same people who never invested in property themselves and continue to return 3-6% per annum in capital markets (after taxes and costs).

These are the same people who never invested in property themselves and continue to return 3-6% per annum in capital markets (after taxes and costs).

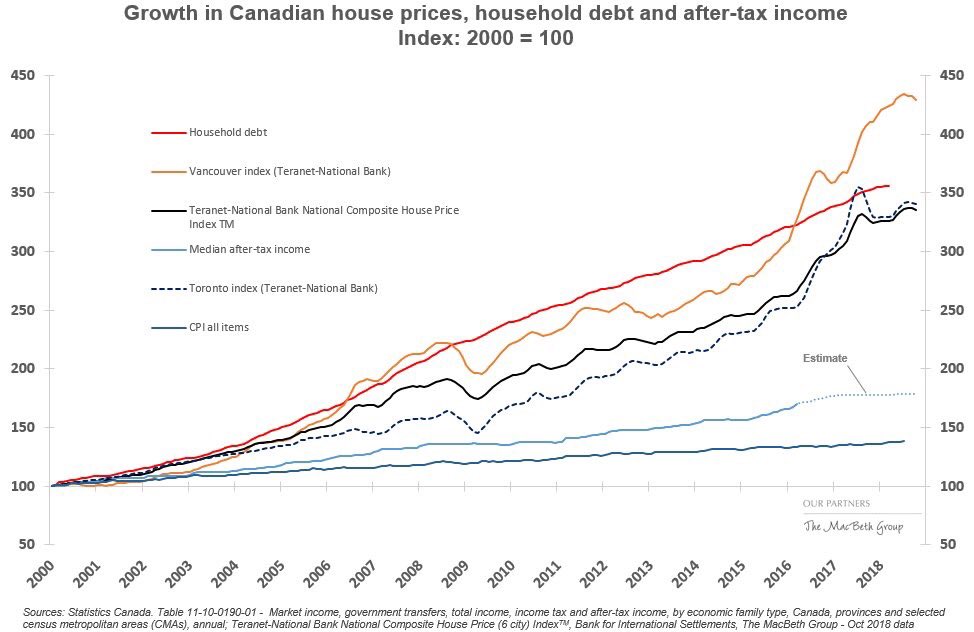

6/ So yes, Canadian market is slowing and prices are declining.

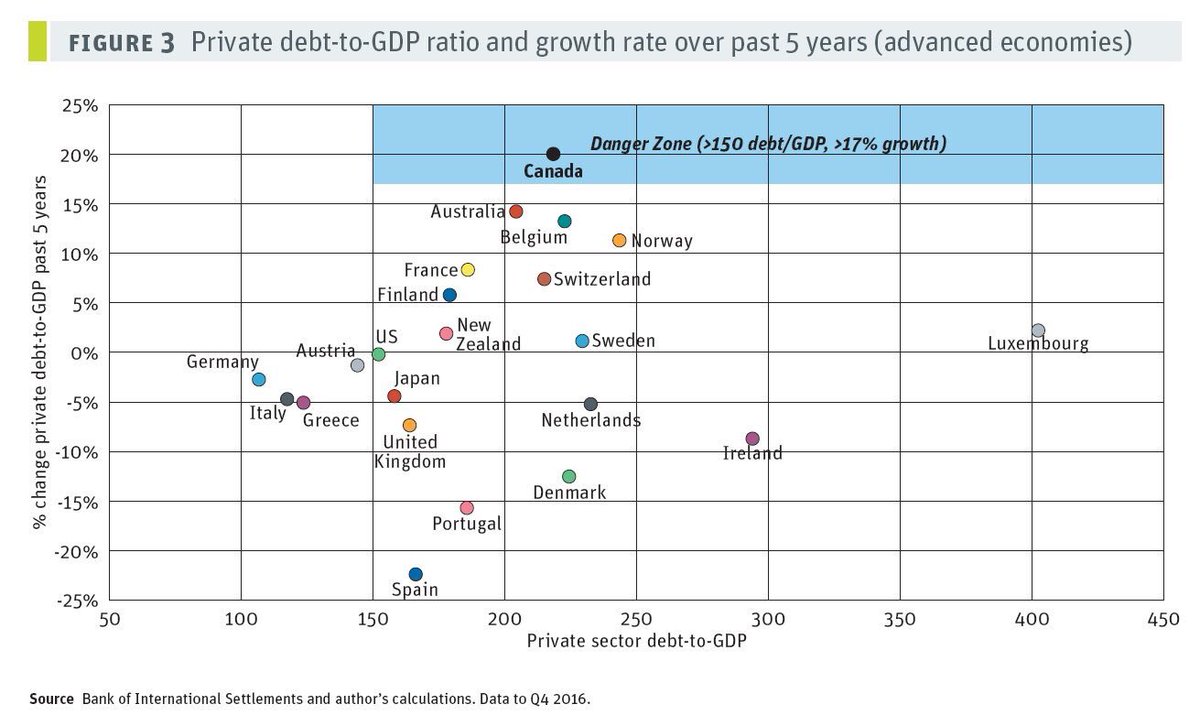

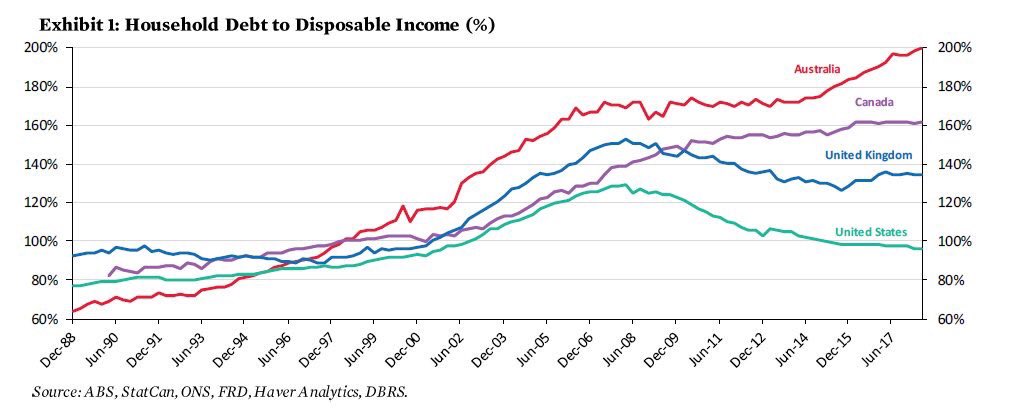

Because the mortgage levels in some countries (such as Canada, Australia, Norway, etc) are huge — no doubt that risks are higher of a deeper downturn.

Because the mortgage levels in some countries (such as Canada, Australia, Norway, etc) are huge — no doubt that risks are higher of a deeper downturn.

7/ Having said that, if you made a gross return of 100% on your property over the last 7 years in #Vancouver or #Sydney — which is around 10% to 11% CAGR — your cash in cash (COC) return using a mortgage is something like net 30% to 35% per annum.

Forget 15%, that is a double.

Forget 15%, that is a double.

8/ From a small down payment you’ve now made a lot of money (equity).

If you were smart you would have payed the debt down, rented your property, used tax writeoffs & achieved strong appreciation.

All 4 are forms of ROI — something the stock market doesn’t offer.

If you were smart you would have payed the debt down, rented your property, used tax writeoffs & achieved strong appreciation.

All 4 are forms of ROI — something the stock market doesn’t offer.

9/ So if the property prices fall significantly from here onwards — say 20% to 30% — you will be hurting... but probably still in a good shape.

The problem is with the new comers, the people who missed out on the boom. They are borrowing large amounts of debt to purchase today.

The problem is with the new comers, the people who missed out on the boom. They are borrowing large amounts of debt to purchase today.

10/ They have seen their friends and peers get rich investing in #realestate — and they want to do the same.

So they are borrowing excessive amounts of debt at the wrong time — during the late cycle prior to a downturn.

So they are borrowing excessive amounts of debt at the wrong time — during the late cycle prior to a downturn.

11/ So don’t listen to the haters out there — most of whom never even invested in #realestate outside of their house (that’s not an asset anyway).

It is a wonderful asset class, just like stocks or bonds, but only at the right time within the business & investment cycle.

It is a wonderful asset class, just like stocks or bonds, but only at the right time within the business & investment cycle.

12/ Focusing on Canadian real estate, the last part of the rise is definintly fuelled by excessive use of mortgage debt.

But for those who bought a decade ago, during the 2008 panic — they have made a fortune and are relatively safe now. @hmacbe

But for those who bought a decade ago, during the 2008 panic — they have made a fortune and are relatively safe now. @hmacbe

13/ Excessive use of mortgage debt at historically low interest rates is more evident in #Australia than anywhere else in the developed world.

No doubt this posses significant risks to the local #realestate market.

No doubt this posses significant risks to the local #realestate market.

14/ Some forecasters have been predicting a fall of 20%, 30% or even a large drop.

This is possible (anything is possible). Is it probable?

Regardless, a 20% drop would erase only 3.5 years of gains. Smart investors became stinking rich holding for a decade or two.

This is possible (anything is possible). Is it probable?

Regardless, a 20% drop would erase only 3.5 years of gains. Smart investors became stinking rich holding for a decade or two.

15/ The truth is haters argue about real estate bubbles — and write books about it — because they actually missed out on it themselves.

FinTwit is full of property bubble callers, which could soon be vindicated (but with totally wrong timing).

We will tell them they are RIGHT.

FinTwit is full of property bubble callers, which could soon be vindicated (but with totally wrong timing).

We will tell them they are RIGHT.

16/ After all — these academics, professors and analysts usually don’t have any skin in the game.

All they want to hear is that they were right, and they called it.

For rest of us investors, we ought to focus on achieving and growing wealth through wise long term investing.

All they want to hear is that they were right, and they called it.

For rest of us investors, we ought to focus on achieving and growing wealth through wise long term investing.

17/ Looking at the fantastic gains long term investors achieved in places like London, HK, Sydney, Vancouver, NYC & other places — it is obvious they won’t hurt all that much.

The pain will be felt by the late comers, the same kind that buy the top of a bull market in stocks.

The pain will be felt by the late comers, the same kind that buy the top of a bull market in stocks.