Lessons of the market. The thread we promised.

The SV dream of 100s of tokens, each accruing value in their own ecosystems, is dead. Whatever your mental model - a complex theory of velocity (MV=PQ) or the idea of "work tokens" - it's important to realise all tokens ultimately compete on a single playing field:

Currency.

Currency.

The problem with "ecosystem" tokens deployed on existing blockchains is that they try to innovate on two levels at the same time:

1) Business -> success or failure depends on cash flow and generating profits

2) Currency -> success or failure depends on liquidity and adoption.

1) Business -> success or failure depends on cash flow and generating profits

2) Currency -> success or failure depends on liquidity and adoption.

For a small minority, this makes sense. The premier example being @binance, which has built a profitable exchange business AND bootstrapped adoption & liquidity of the ecosystem token $BNB.

As one of the largest exchanges, @binance are a pillar of the crypto-economy. The company has immense influence, and thus merchants & service providers integrate $BNB as an alternative method of payment.

CEO @cz_binance rewards those who adopt $BNB as quasi-currency with the occasional retweet, and @BinanceLabs may even go as far as funding their ecosystem.

But for most tokens, trying to innovate at both the business and currency level results in no customers and an illiquid shitcoin.

In a vicious cycle, the added friction of the "ecosystem" token dampens network effects, lowering token liquidity, driving customers to competing platforms free from the burdens of a token, ultimately causing the underlying business (as well as the token) to fail.

How did most teams - who had an interest in justifying their token to raise money - try to get around this?

The alchemy of "cryptoeconomics" (a methodology we once subscribed to).

The alchemy of "cryptoeconomics" (a methodology we once subscribed to).

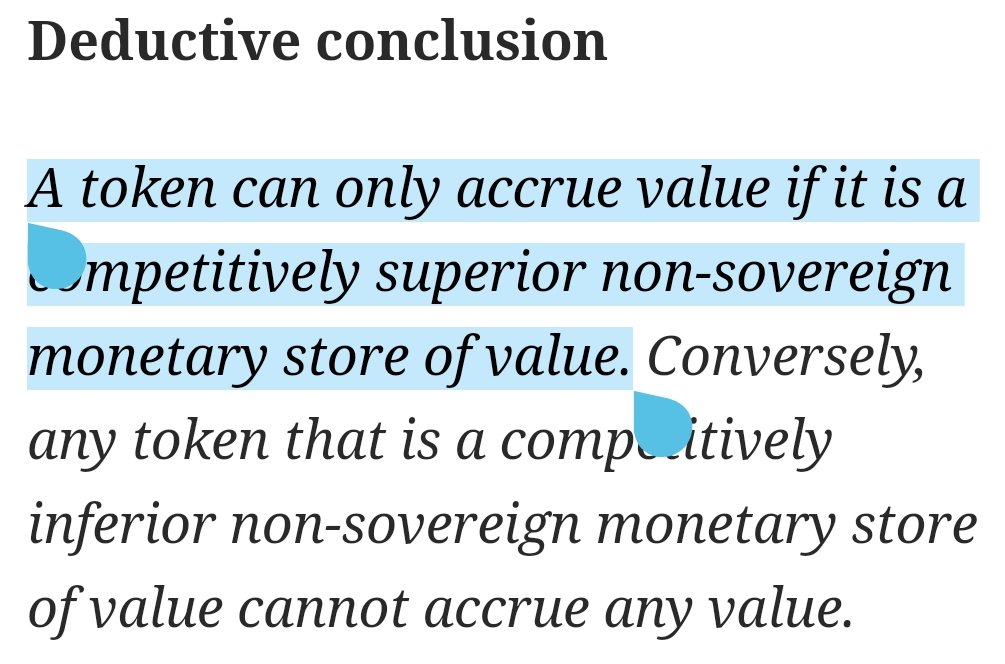

By introducing "staking mechanisms", token issuers try to build a network on promises of future value. However, without real adoption & usage, why would these tokens be worth anything at all?

You can't get past the "currency" problem by introducing a pseudo-ponzi scheme.

You can't get past the "currency" problem by introducing a pseudo-ponzi scheme.

Regardless of "cryptoeconomic" design, teams must still fight an uphill battle to create real use cases that drive value to their tokens.

So where does this leave us? Exit all crypto markets?

Far from it.

Far from it.

We recently met with partners at @Algo_Capital. Something struck us after the meeting.

The mandate is different from most ecosystem funds. It's not to invest in "ERC20"-like utility tokens on @Algorand, but in profitable businesses which adopt the $ALGO token as their currency.

The mandate is different from most ecosystem funds. It's not to invest in "ERC20"-like utility tokens on @Algorand, but in profitable businesses which adopt the $ALGO token as their currency.

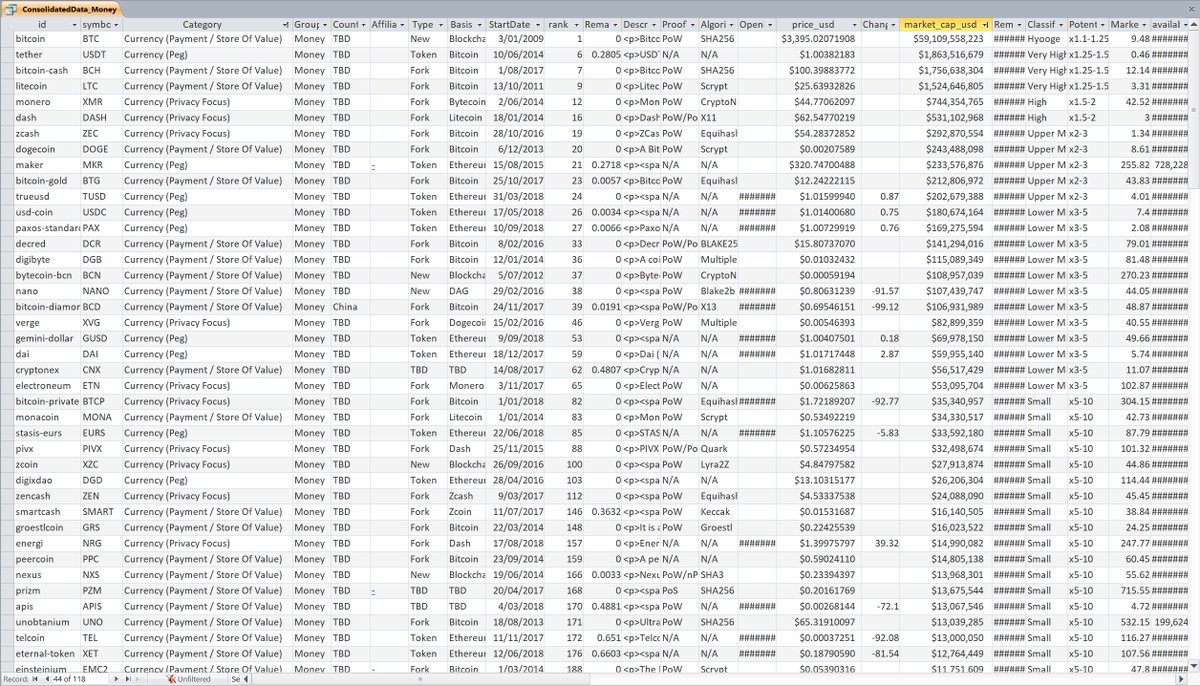

Look to the top 200 on @CoinMarketCap, you will notice that almost all value has accrued to native blockchain tokens which aim to achieve one thing & one thing alone:

Currency status.

Currency status.

The ultimate example is $BTC. Bitcoin's market capitalisation is backed by the most:

1) Trust -> PoW & stable monetary policy

2) Scaling -> Lightning Network

3) Applications built on top of its network -> not dApps, but cApps like spot/futures exchanges and custody solutions.

1) Trust -> PoW & stable monetary policy

2) Scaling -> Lightning Network

3) Applications built on top of its network -> not dApps, but cApps like spot/futures exchanges and custody solutions.

Bitcoin focuses on one thing only: currency, with a strong use case as an SoV.

For this, it has been rewarded; crowned King of the cryptoasset market.

For this, it has been rewarded; crowned King of the cryptoasset market.

The same applies to "smart contract platforms".

These are also fundamentally currencies, except with the enhancement of programmability.

This widens the scope for applications - and hence for adoption - at a scale greater than that of non-programmable money.

These are also fundamentally currencies, except with the enhancement of programmability.

This widens the scope for applications - and hence for adoption - at a scale greater than that of non-programmable money.

Perhaps the craze of the ERC20 and tale of a "world computer" has been one big fat distraction from Ethereum's true potential: leveraging the native $ETH token to create decentralised protocols.

Three Ethereum protocols come to mind, all WITHOUT native tokens:

1) @UniswapExchange -> decentralised exchange protocol

2) @MakerDAO -> stablecoin protocol locking up over 1% of the supply of $ETH

3) @compoundfinance -> open source lending protocol.

1) @UniswapExchange -> decentralised exchange protocol

2) @MakerDAO -> stablecoin protocol locking up over 1% of the supply of $ETH

3) @compoundfinance -> open source lending protocol.

And the other side of the picture? Business.

Consider businesses & decentralised protocols built to accept base layer currencies (like $BTC or $ETH).

The very nature of the firm transforms, enhanced by programmatic on-chain dividend redistributions and shareholder governance.

Consider businesses & decentralised protocols built to accept base layer currencies (like $BTC or $ETH).

The very nature of the firm transforms, enhanced by programmatic on-chain dividend redistributions and shareholder governance.

So what will "business on the blockchain" look like? Tokenised real estate, traditional equity or fancy collectibles?

None of this is exciting or revolutionary, and it's not where asymmetric opportunities will be found.

None of this is exciting or revolutionary, and it's not where asymmetric opportunities will be found.

Instead, consider securities otherwise impossible if not for public blockchains.

The ideal example is @NexoFinance, a lending platform regularly redistributing dividends to $NEXO holders.

The ideal example is @NexoFinance, a lending platform regularly redistributing dividends to $NEXO holders.

Despite low liquidity & poor exchange listings, $NEXO maintains strong value relative to its initial offering price and overall market performance in 2018.

Why?

It's fundamentally backed by future on-chain cash flows of $BTC or $ETH.

Why?

It's fundamentally backed by future on-chain cash flows of $BTC or $ETH.

This is the true intersection of business & currency.

Long term, we believe value will accrue to 2 categories:

1) Currencies -> trust & growth as an SoV or MoE

2) Security tokens -> cryptocurrency accepting businesses / open-source protocols redistributing fees on-chain.

Long term, we believe value will accrue to 2 categories:

1) Currencies -> trust & growth as an SoV or MoE

2) Security tokens -> cryptocurrency accepting businesses / open-source protocols redistributing fees on-chain.

Focus on:

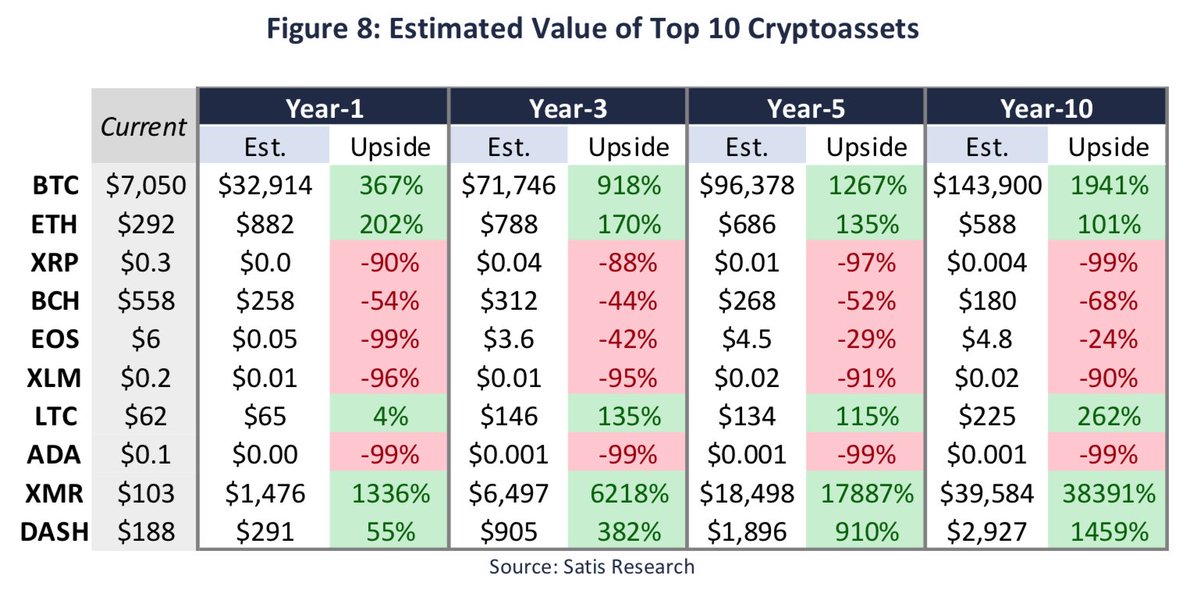

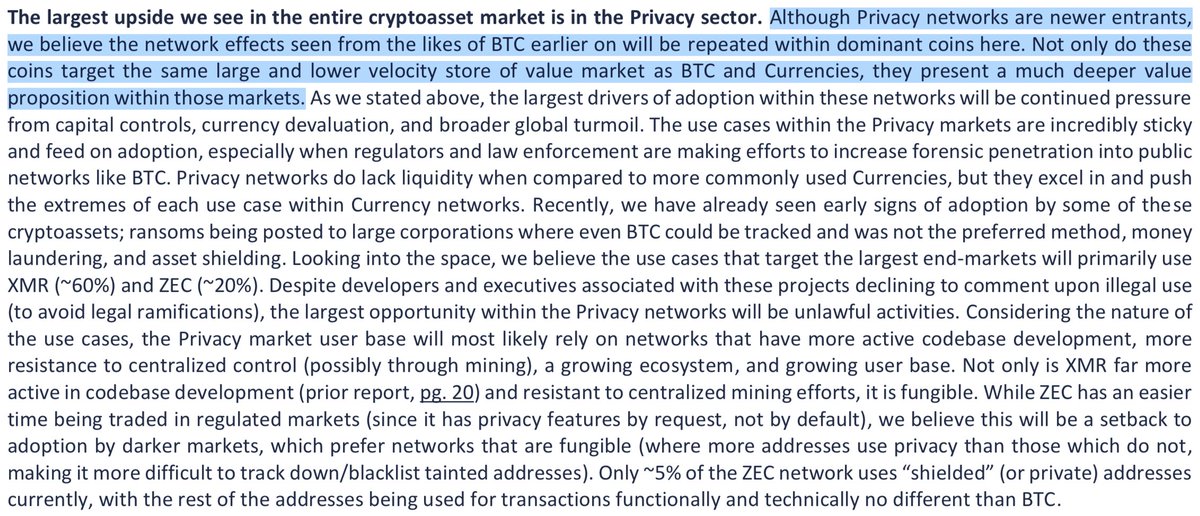

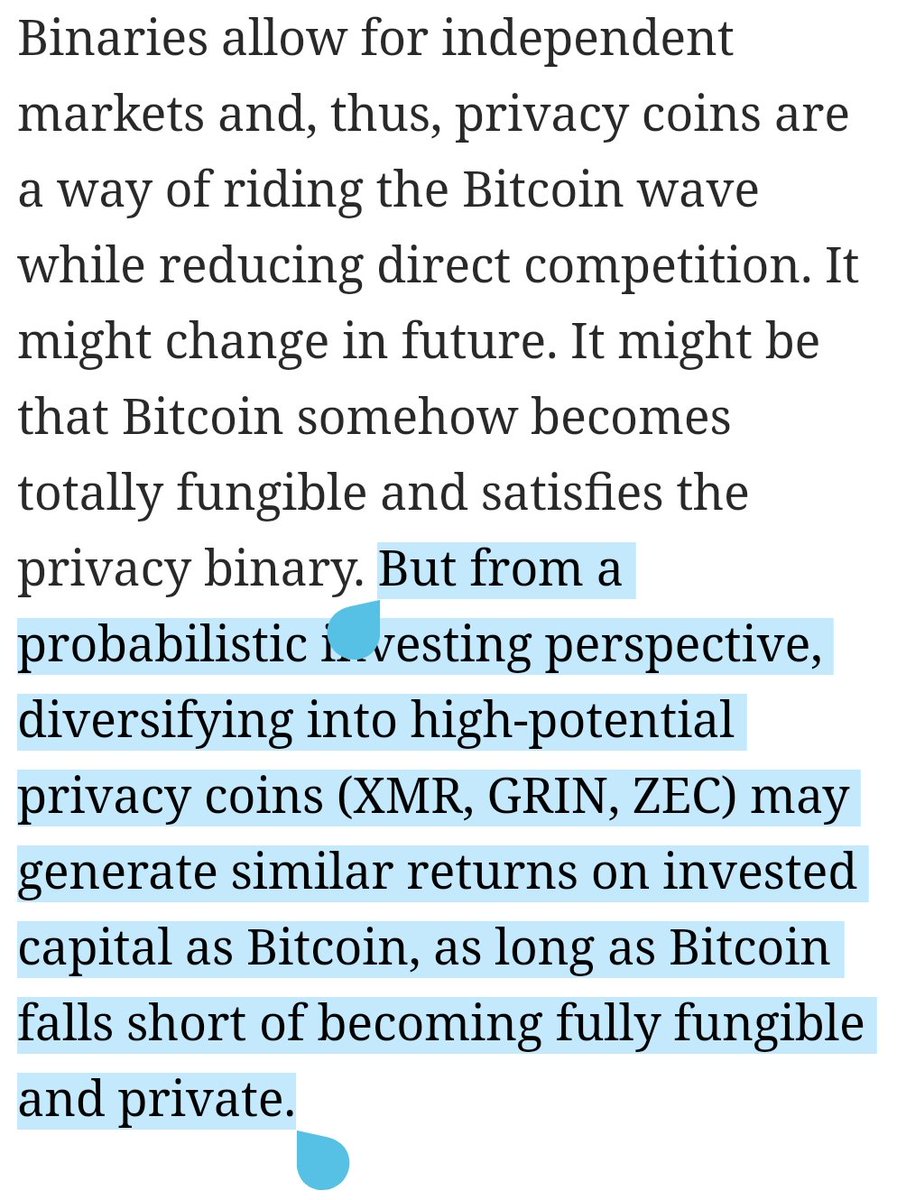

1) Currencies with unique technological propositions and/or aggressive business development. Think $BTC, $ETH, $DCR, $XMR, $ZEC, $XRP, $GRIN, @beamprivacy or $ALGO

2) Security tokens made possible through blockchain, not dressed up startups that couldn't raise VC.

1) Currencies with unique technological propositions and/or aggressive business development. Think $BTC, $ETH, $DCR, $XMR, $ZEC, $XRP, $GRIN, @beamprivacy or $ALGO

2) Security tokens made possible through blockchain, not dressed up startups that couldn't raise VC.

One final mental model:

Think of each cryptocurrency as its own economy.

Just like the existing financial system, each economy has its own central bank - a "decentralized" central bank - bound by the mandate of its protocol and social consensus.

Think of each cryptocurrency as its own economy.

Just like the existing financial system, each economy has its own central bank - a "decentralized" central bank - bound by the mandate of its protocol and social consensus.

What are native on-chain security tokens?

The businesses of these borderless economies.

The businesses of these borderless economies.

$BTC is perhaps the only cryptocurrency without a "central" bank, the largest GDP and the greatest breadth of social scalability.

So if you are thinking about the long term prospects of the industry, the questions are simple:

Which economies will grow the largest, and which economies will grow the fastest?

Which economies will grow the largest, and which economies will grow the fastest?