,

35 tweets,

11 min read

Read on Twitter

Finally getting around to doing a thread about my working paper: The worst of both worlds? Dual-registered investment advisers. Generally, there are two types of financial advisers: fiduciaries and brokers 1/ papers.ssrn.com/sol3/papers.cf…

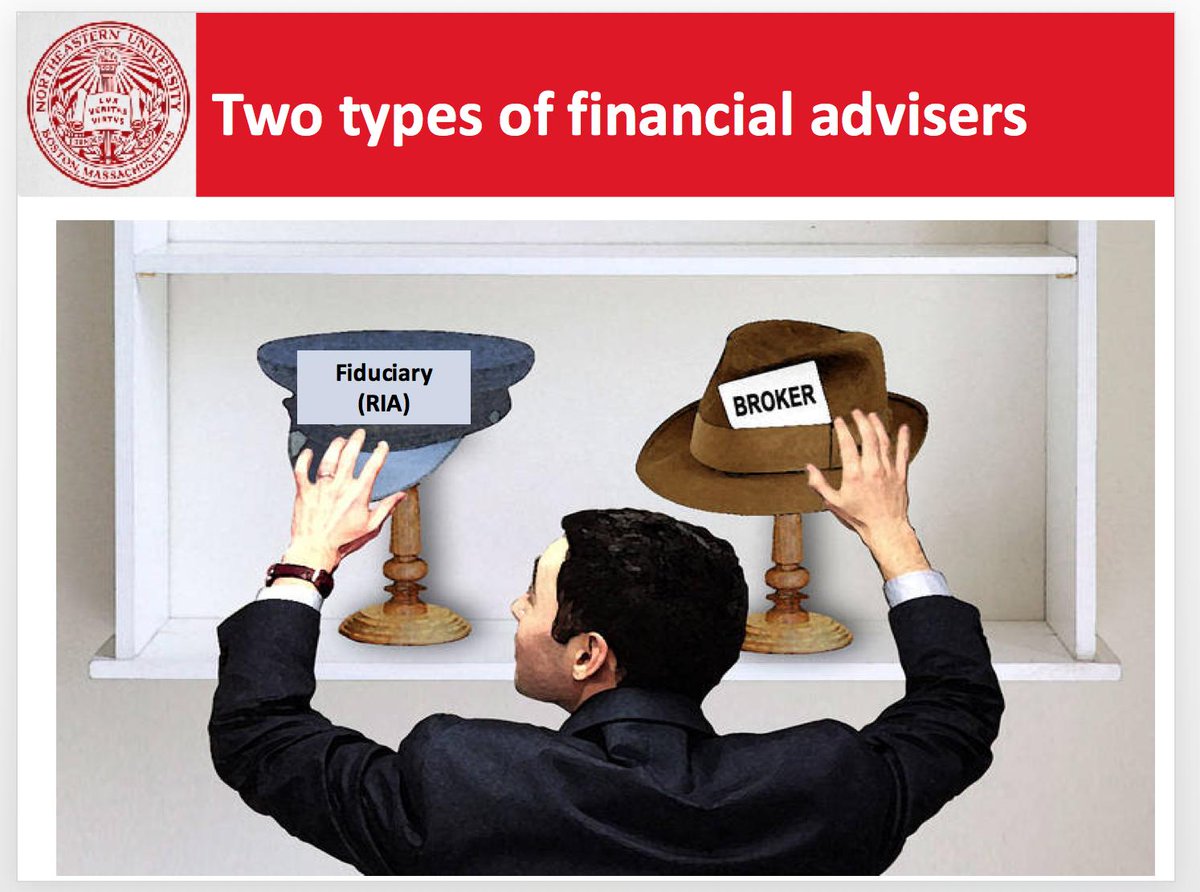

Fiduciaries have a duty of care and loyalty, to act in clients' best interests. Brokers face a less stringent suitability standard. 2/

In practice, the key distinction between the two types of advisers relates to the way that they charge fees. Fees as a percent of assets are designed to help mitigate conflicts. 3/

In practice, about 81% of fiduciary (aka registered investment adviser, aka RIA) assets are managed by firms that act as both brokers and fiduciaries. 4/

Here's a list of the top 10 dual registrants as of 2016, with detail on assets, employees, accounts, and whether they accept retail clients (which I define as under $100,000 in assets under management (AUM)). 5/

Here's a chart of AUM by dual RIAs, the top dual RIAs, and independent RIAs. Note the heavy concentration of AUM among a small number of firms. 6/

Dual RIA revenues (top 50 firms) have shifted from commission to fee based over time. 7/

Why the big shift from commission to fee-based? See the flowchart below for the answer! 8/

In this project, I am trying to understand the performance of retail (mutual fund) clients of dual registrants. I argue that dual registrants will prefer the institutional share classes of the (load) mutual funds that they already sell to their brokerage clients. 9/

Primer on mutual fund distribution below. In general, the institutional share classes of mutual fund families have no commissions (with a few exceptions) and are available to retail clients of RIAs. The fund family will waive the minimum investment for these clients. 10/

I provide evidence that typical dual RIA will prefer the institutional share classes of the load funds they already sell. Dual RIAs explicitly state this in their Form ADV Part 2; further, these are the fund families that provide revenue sharing (kickbacks (not 12b-1s!!!) 11/

Mutual fund flows from load share classes (and some direct share classes) flock to institutional share classes, especially after 2007. The chart below includes actively managed balanced and stock funds. 12/

When I break out institutional share classes by fund family: 1) institutional, also has a load share class, 2) institutional, also has a no load share class, and 3) institutional, no other classes, the majority of flows go to institutional, also has a load class 13/

Why do we care? Well, as I will show later, the institutional share classes of load fund families, especially those that revenue share (which are precisely the share classes that dual RIAs prefer), are the worst performers. 14/

This slide summarizes my key findings: 1) dual RIAs have significant conflicts of interest 2) dual RIAs charge higher fees to their retail clients than ind. RIAs, 3) the funds they prefer tend to underperform. 15/

Caveat here! I am an academic and I'm looking at averages. My results do not imply that ever single dual registered adviser underperforms. However, I provide strong evidence that, on average, retail clients of dual RIAs pay more and do underperform. 16/

Continuing: I use Form ADV Parts 1 and 2 to collect data. I hand collect data from Form ADV Part 2 (Part 1 is machine readable). My analysis focuses on the largest dual RIAs and independent RIAs. 17/

More about my data...18/

I mentioned revenue sharing before. Revenue sharing is money paid to dual RIAs from fund family profits. It is not a commission. It is used for promotional activities and often to be listed on dual RIAs preferred fund lists that are distributed to advisers. 19/

A bit more about revenue sharing: I focus on fund families that revenue share the most, where revenue sharing absolutely goes beyond simple "shelf space." In my analysis, I focus on the revenue sharing fund families that dual RIAs mention the most frequently. 20/

This is Morgan Stanley's revenue sharing disclosure (ADV Part II): 21/

These are the top 10 revenue sharing families (in my paper, I consider a family a big revenue sharer if they are mentioned by at least five dual RIAs). 22/

Summary stats! Dual RIAs are very big. They are also more likely to cross-sell insurance products. In regressions (not shown) I show that dual RIAs that accept retail clients are the most likely cross-sell insurance products. 23/

More summary stats! Dual RIAs more likely to have affiliated mutual funds and to perform less due diligence on these funds. Again, regressions find that this result is strongest for dual RIAs that accept retail clients. 24/

More: Dual RIAs are more likely to use revenue sharing fund families and to include these funds on their preferred lists. Dual RIAs charge their retail clients higher fees (at least this is what they report!!) 25/

So far: Dual RIAs have more conflicts. 26/

What about performance? Recall, I am using the institutional share classes of load fund families as a proxy for dual RIA retail client performance. Summary stats: broker sold retail underperform, direct sold retail outperform. Aggregated, institutional are in the middle. 27/

Here, I break out institutional into: 1) also has broker sold, 2) also has direct sold, 3) single. Also has broker sold underperform. (My performance measure is the intercept from a regression of fund performance on 11 Vanguard index funds to proxy for different exposures 28/

This regression analysis shows that fund dollars flow to the institutional share classes of revenue sharing fund families (subset of the institutional share classes of broker sold fund families). Flows 15% higher per yr for these share classes compared to direct sold. 29/

This regression shows that performance of the institutional share class of load fund families underperform direct sold share classes. 30/

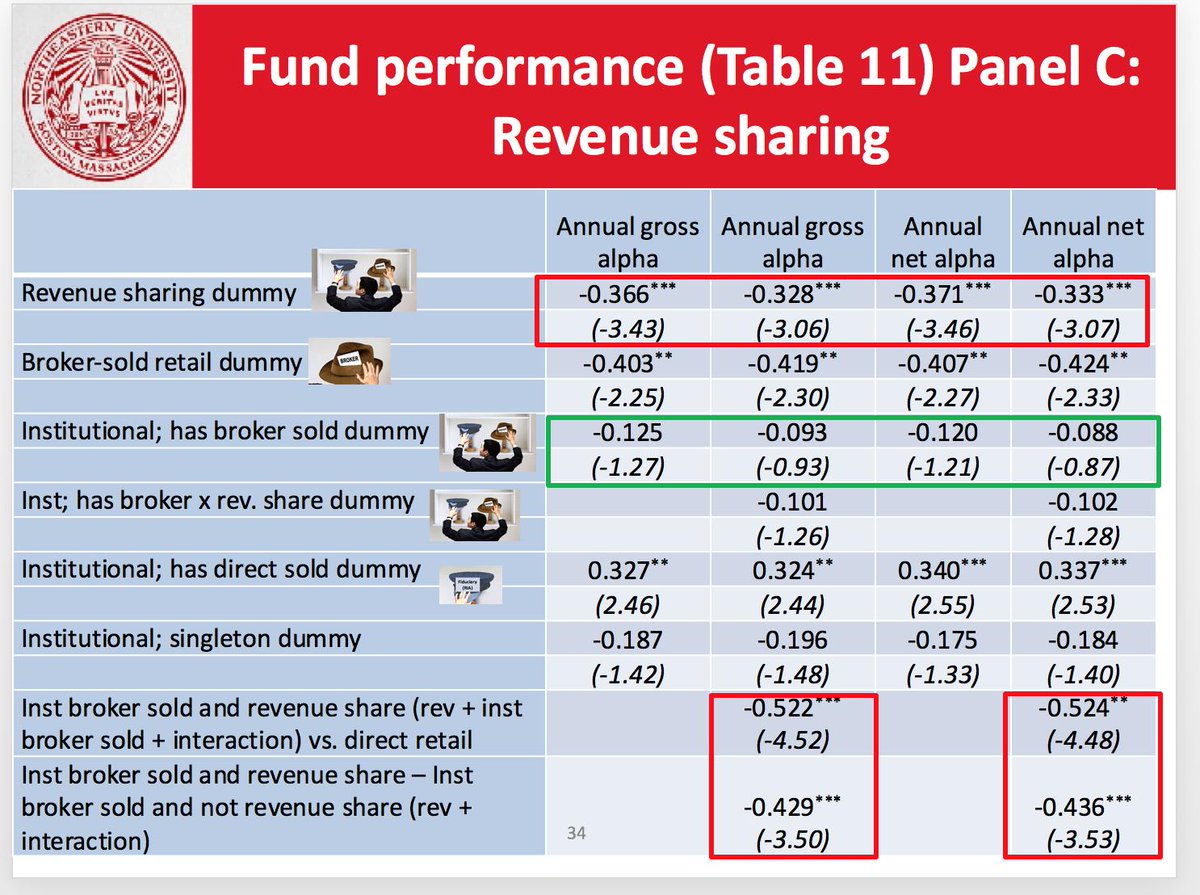

This slide shows that the subset of revenue sharing institutional share classes of load mutual funds underperform direct sold funds by 52 basis points (bp) per yr, and underperform institutional share classes of load mutual funds that do not revenue share by 42 bp/yr. 31/

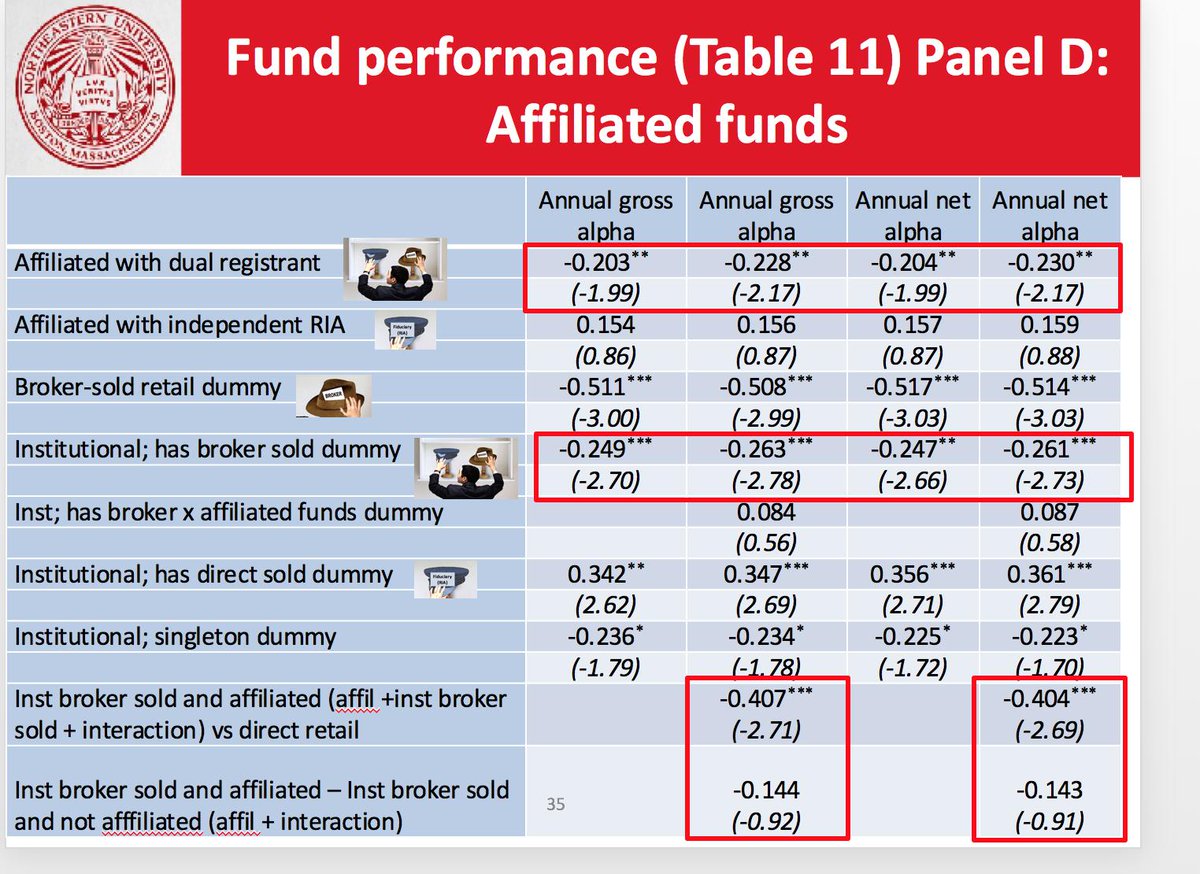

Finally this slide shows that the subset of affiliated institutional share classes of load mutual funds underperform direct sold funds by about 20 bp /yr 32/

Conclusion! Dual RIAs are conflicted and have higher fees. 33/

Dual RIAs that revenue share and serve retail clients have the worst performance of all, but attract the highest flows 34/

Finally: It appears that dual registrants, who are required to act as fiduciaries, aren't consistently behaving in a fiduciary manner. Why does this matter? Clients of these firms are not necessarily being treated in accordance with the spirit of the fiduciary standard. 35/35