Who am I to say no to @fwred? So here it is!

@fwred The ECB (SSM) just released its annual SREP results. As a reminder, it’s the annual assessment of risks large banks are facing with the corresponding capital requirement add-on (called the “P2R”). Lots of very useful info this year.

@fwred Imho, the big picture is this: NPLs are the worry of the past. Now the SSM will focus on governance, OpRisk and profitability. The profitability issue will obviously feed the thinking on the ECB’s strategic review as <0 rates are a culprit.

@fwred OpRisk is a also a big issue for two reasons: managing OpRisk is very expensive (compliance costs etc.) and the industry hopes that Basel 4 implementation in the EU will water down some expensive Basel provisions on OpRisk.

@fwred This includes some important choices to make on the OpRisk RWA formula parameters. Not too sure about the EC’s leniency on that, now. (Again: this is a BIG issue, number-wise.)

@fwred Looking at the report now, step by step. First, capital.

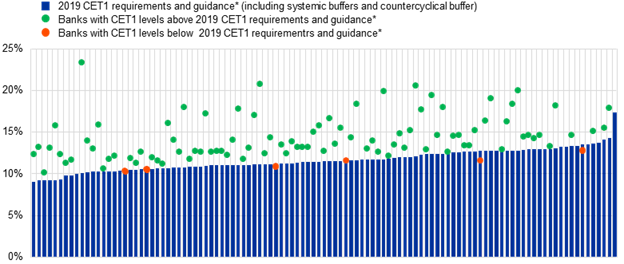

@fwred As usual, you guys want to know who the bad boys are. Well, we’ve got 7 of them this year! One bank refused to disclose its P2R (and this can’t be good) and six had capital below their P2G.

@fwred What’s P2G? Very good question. It’s the Pillar 2 guidance, which is an expectation from the SSM that the bank will keep capital above that level, but not a legal requirement.

@fwred The difference is important, because if you are below the P2R you face distributions constraints (e.g. no bonus or dividend) whereas you don’t face any if you are below the P2G – apart from feeling the breath of the supervisor on your neck.

@fwred Last year, only 1 bank was below the P2R – and we had no data on P2G. This year here’s the P2G chart with the 6 weakest links, but it’s impossible to know who they are because P2G are not public.

@fwred What else do we learn from the capital bit of the process? Not much. Capital requirements have barely changed, global P2G at 1.5% of RWA and global P2R at 2.1% of RWA.