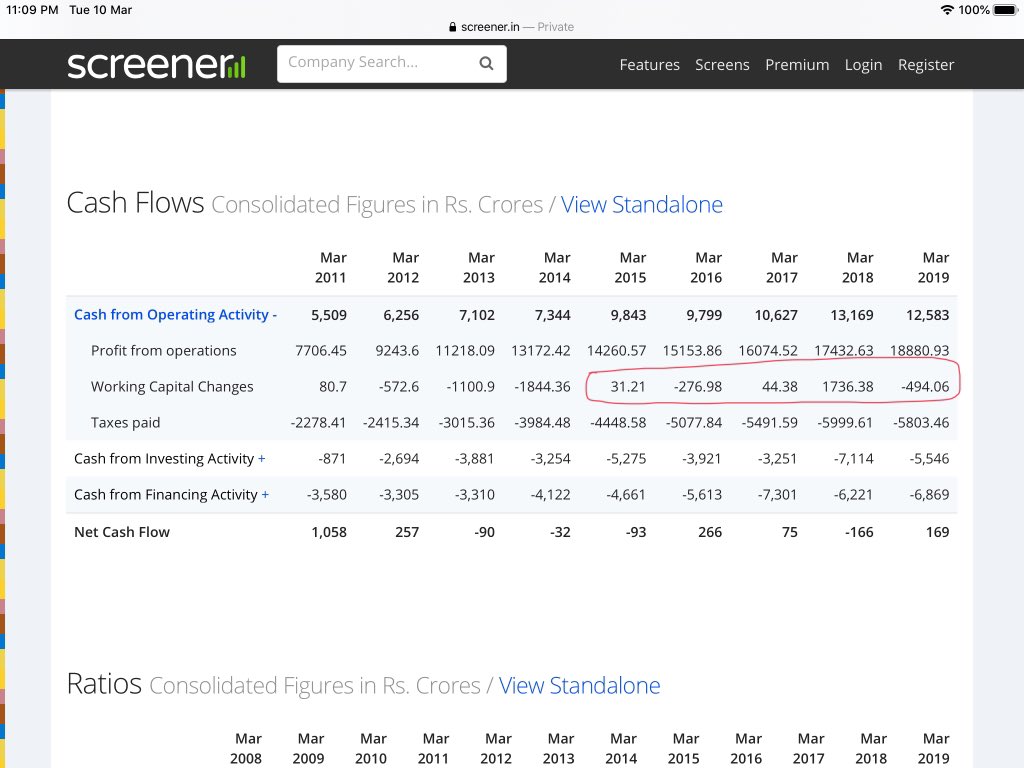

1/N A thread on #ITC.Last 10 year EPS is up from 2.5 to 12.2. Almost 5x. PE peaked out around 50 n now at 14. A 3L Cr market cap company with 0 promoter holding where ESG funds dumped more than 6% which is more than 20k crores. Who has capacity to consume it. CFOs as good as

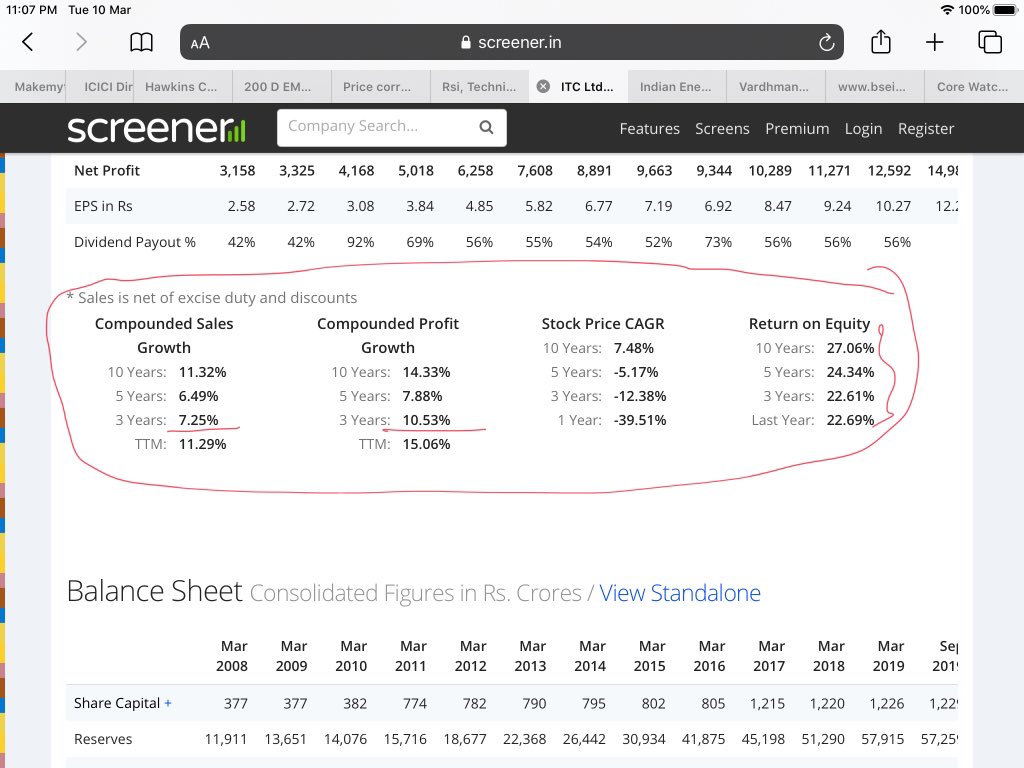

2/N as good as accounting profit. Low debt , decent ROE, not a great capital allocator still 2 businesses apart from civvies ve respectable ROE on relative basis, growth for last 3 years high single to low double digit. Has business not performed or 1. Had investors set to high

3/N expectation at 50 PE ? 2. Text books only tells u that valuation is driven only by cash flows but text books do not tell u that high float becomes a risk when an existing investor wants to exit for reasons beyond cash flow 3. Text books do not tell you what kind of valuation

4/N difference a high float stock with 0 promoter holding in a high market size stock can do 5/N textbooks do tell that buy low and sell high but people crib no return by buying high n sell low (eps up 5x , valuation down to 1/3x). Business might ve it’s own positive n negative

5/N but it’s first the risk reward ratio of investor , his entry, his exit . You can’t buy things at 40-50x n crib management did not perform, it’s you who carry that risk. It took Infosys and Microsoft 8 years to recover their prices of 2000, does not mean they were bad

6/N company or good company, it just means they were bad investment or good investment. Personal View : Have not done L2 research but based on L1 research, 1. it is a company with own set of strengths and issues. 2. M not a believer of predicting future growth but one who likes

7/N to safeguard risk by buying at margin of safety when there is pessimism 3. There r lot of flaws in mgmt n one must factor it in margin of safety but despite that the growth has been Okavango n 20 year return is impressive 4. My personal research says , even for 3-4 years

8/N period, there r factors other than cash flows which impacts valuation n some of those factors r not in favour of ITC - Size, float n fund philosophies 5. One more personal research says , the relation between ROE n return is non linear (will write sometime), it need to be

9/N above 12-15%, below that ROE is a deal breaker, above that the weightage of other factors increases n hence if non cig ROE can be above 15 with other factors supporting its not a bad scenario 6. Mgmt really need to be tracked for their capital deployment in hotel business

10/N. final summary : need to study more but unless float issue gets addressed, difficult for price issue to resolve . However, those who r cribbing ITC has been a wealth destroyer in last 5 years n it’s a poor stock, before looking at stock, they first need to look at own

11/N investment thesis,they had their margin of safety misplaced at 45-50 PE n they miss judged the float risk.