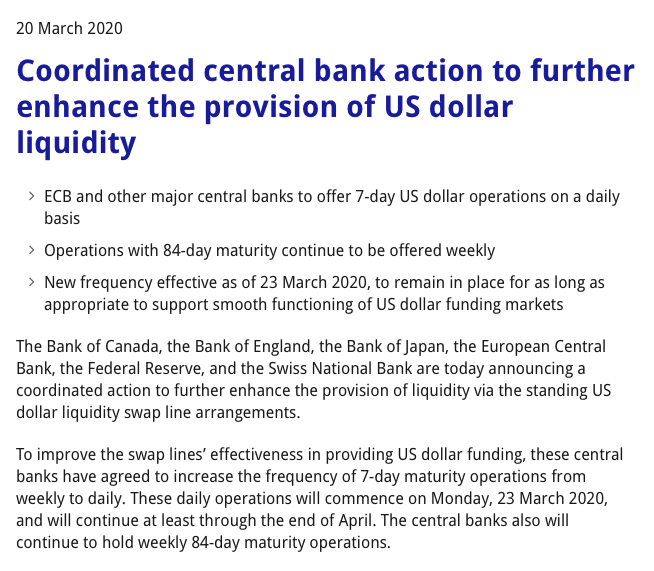

short explainer of daily swap lines with @ecb example:

European banks need dollar financing for their dollar assets (loans, bonds, derivative positions etc) or for their clients.

Usually, in non crisis times, they get dollars from USD repo markets or from fx swap markets.

European banks need dollar financing for their dollar assets (loans, bonds, derivative positions etc) or for their clients.

Usually, in non crisis times, they get dollars from USD repo markets or from fx swap markets.

in crisis times, willingness to provide dollar funding shrinks in private markets.

some European banks can borrow directly from US Federal Reserve, but mostly will go to ECB.

The Fed then agrees with the ECB to open up a swap line. for both, it's matter of financial stability

some European banks can borrow directly from US Federal Reserve, but mostly will go to ECB.

The Fed then agrees with the ECB to open up a swap line. for both, it's matter of financial stability

The first leg of the swap: the ECB creates a Euro account for the Fed, the Fed a dollar account for the ECB, at an agreed exchange rate (more accurately, accounts exist and get credited). They 'lend' to each other.

Second leg at future point in time, this transaction unwinds.

Second leg at future point in time, this transaction unwinds.

if exchange rates fluctuate for the duration of the central bank swap, the one whose exchange rate depreciates has to pay the other in what is known as a margin call.

won't bore you with the details but IMF can here

imf.org/external/pubs/…

won't bore you with the details but IMF can here

imf.org/external/pubs/…

how does @ecb lends the USD it has in its Fed deposit?

it started with weekly operations for 84 days maturity: it lends USD to European banks every week, in 3 months loans against collateral .

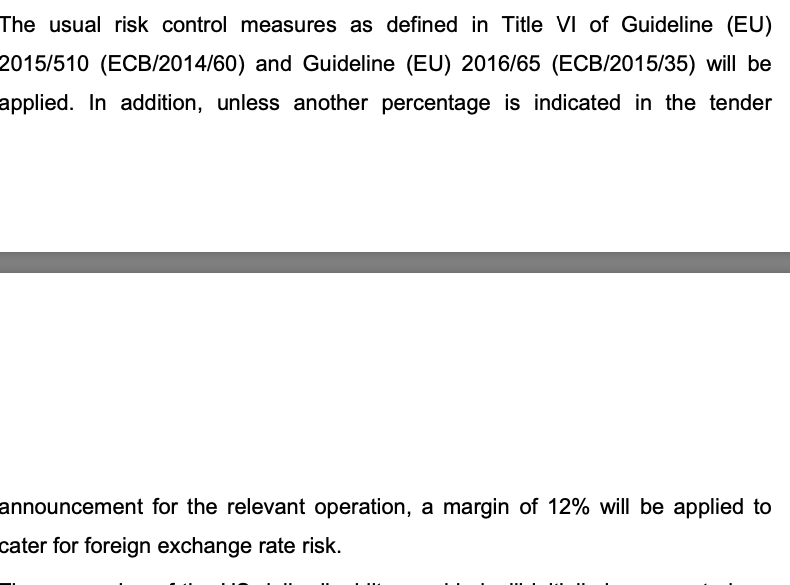

to access USD loans, banks have to provide collateral securities, in EUR or USD.

it started with weekly operations for 84 days maturity: it lends USD to European banks every week, in 3 months loans against collateral .

to access USD loans, banks have to provide collateral securities, in EUR or USD.

the devil, as usual, is in collateral valuation that @ecb applies (but shouldn't):

1. ECB asks 12% haircut related to fx risk (for every USD100, it requires banks to give USD120 of collateral at market value).

already hiking up the price of dollar liquidity

1. ECB asks 12% haircut related to fx risk (for every USD100, it requires banks to give USD120 of collateral at market value).

already hiking up the price of dollar liquidity

reason why ECB moved to 7day USD loans on a daily basis?

procyclicality

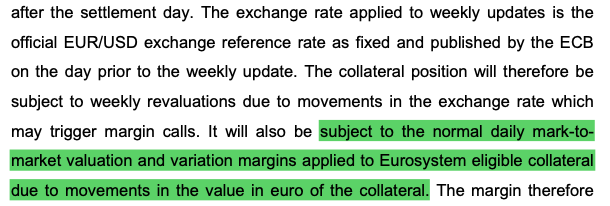

2. For loans longer than 7 days, ECB updates exchange rate and calls margin if USD stronger.

increasing funding pressures on borrowers

procyclicality

2. For loans longer than 7 days, ECB updates exchange rate and calls margin if USD stronger.

increasing funding pressures on borrowers

pro-cyclicality already baked into @ecb collateral framework:

3. For any repo loan, ECB marks collateral to market. If price falls, ECB asks the bank to make up for the difference (margin call).

increasing funding pressures on borrowers.

3. For any repo loan, ECB marks collateral to market. If price falls, ECB asks the bank to make up for the difference (margin call).

increasing funding pressures on borrowers.

in sum, banks prefer shorter USD loans from @ecb because in very uncertain times, these loans can actually magnify, instead of easing, market pressures:

1. FX related haircut

2.weekly margin calls on fx movements for loans>1 week.

2. daily margin calls on EUR/USD collateral

1. FX related haircut

2.weekly margin calls on fx movements for loans>1 week.

2. daily margin calls on EUR/USD collateral

you reasonably ask: why the hell does ECB need protection against collateral/fx risk?

it doesn't - collateral valuation is there to ensure that when borrower defaults, it can sell collateral security & recover your cash.

But ECB selling = mayhem.

it doesn't - collateral valuation is there to ensure that when borrower defaults, it can sell collateral security & recover your cash.

But ECB selling = mayhem.

central banks are there to protect liquidity - as @Lagarde put it in @FT - not worsen it by selling securities of its bankrupt counterparties.

collateral valuation comes from 1990s push for private repo markets, and nearly destroyed the euroarea in 2008 onlinelibrary.wiley.com/doi/abs/10.111…

collateral valuation comes from 1990s push for private repo markets, and nearly destroyed the euroarea in 2008 onlinelibrary.wiley.com/doi/abs/10.111…

there is also a hierarchy of central bank swaps: in contrast to the Fed now, in 2008 ECB has treated Eastern European central banks as 'subordinated' central banks in what I described a while ago as 'our currency, our banks, your problem'

fessud.eu/wp-content/upl…

fessud.eu/wp-content/upl…

the ECB treated CEE central banks as private commercial banks and wildly overstepped its mandate in the famous Troika austerity-led programs in Eastern Europe.

In contrast, the Swiss central bank treated EE central banks as peers.

Orban never forgot it.

In contrast, the Swiss central bank treated EE central banks as peers.

Orban never forgot it.

ECB’s position riddled with conflicts of interest.

Ssubsidiaries of euro area banks dominating CEE financial systems had large EUR rollover needs. CEE central banks asked for ECB swap lines when currencies started falling

Ssubsidiaries of euro area banks dominating CEE financial systems had large EUR rollover needs. CEE central banks asked for ECB swap lines when currencies started falling

ECB said niet to official swaps - its participation in Troika bailout negotiations meant it would not extend unconditional support, via swaps, to CEE central banks.

like Fed saying to ECB, I won't lend to you unless I get a say in how Euro countries design corona rescue packages

like Fed saying to ECB, I won't lend to you unless I get a say in how Euro countries design corona rescue packages

in the immortal words of Yves Mersch, then at CB of Luxemburg, now ECB Executive Board:

'The ECB cannot be a small god for everyone and for everything... no mandate to be a regional United Nations agency'

bit of postcolonial monetary discourse to MS required to adopt euro!

'The ECB cannot be a small god for everyone and for everything... no mandate to be a regional United Nations agency'

bit of postcolonial monetary discourse to MS required to adopt euro!

compare ECB and Swiss Central Bank fx lending arrangements and ask yourself why Eastern Europeans arent joining a Swiss monetary union.

Only one accepted their own currency securities. The other wanted EUR securities.

Only one accepted their own currency securities. The other wanted EUR securities.

ECB position got so bonkers that Latvia ended up borrowing euros in swap lines from Denmark and Sweden, two non-Euro member states!

reader, you don't get a prize for guessing which Eurosystem central bank opposed ECB swap lines to CEE central banks.

(end of 'short' thread).

(end of 'short' thread).