A lot of general reader interest in my covenant erosion piece yesterday. Which was really nice! So I thought I'd do a thread to explain why it's such an important issue and why bond fund managers get so emotive about it. ft.com/content/410133…

So what are covenants? In simple terms, they are terms in junk bonds that stop the companies from taking actions that would be bad for the bondholders.

Investment grade bonds generally don't have them, because they are big trustworthy companies. In contrast, you don't want to lend money with no strings attached to a company with a real chance of going bust.

High-yield bonds have what are known as "incurrence covenants". These stop companies from taking negative actions like incurring too much debt or paying out a large dividend to the owners.

Bonds don't typically have "maintenance covenants". Loans traditionally have these stricter covenants, which don't just stop companies from raising additional debt, but require borrowers to stay within set leverage ratios etc every quarter.

The (widely misused) term "cov-lite" refers to leveraged loans which don't have maintenance covenants and instead have a bond-like incurrence covenant package. Here's a piece I wrote about Blackstone taking cov-lite into the middle market: ft.com/content/6f18c3…

Private equity firms (unsurprisingly) are one of the main users of leveraged loans and high-yield bonds. The whole concept of the LBO (leveraged buyout) was only made possible by Michael Milken's invention of junk bonds in the 1980s.

Private equity firms are focused on "maximising value" for their LPs (and *cough* their GPs!). Maximising shareholder value often comes at the expense of bondholder value. You can see where this is going...

Luckily for the private equity firms, the ECB buying IG corporate bonds has squeezed the whole market and pushed new buyers into HY.

At the same time, institutional money is flooding into (now largely cov-lite) leveraged loans.

At the same time, institutional money is flooding into (now largely cov-lite) leveraged loans.

When a lot of money is flowing into an asset class, standards naturally slip. Fund managers are under pressure to invest and are more likely to accept things they wouldn't previously. Or they are looking at five deals at once and simply don't have the time to catch everything.

A common refrain is "Well, if you don't like it, don't buy it!". Which is fine... if you know what you're buying. But the fact is, even the most sophisticated investors cannot spot all the hidden trapdoors in hundreds of pages of documentation.

Bankers often say "investors put a price on aggressive covenants". The theory is here that a company raising a bond that allows it to pay more dividends than usual to its PE owner will be charged higher interest rates by investors.

But how can you put a price on something that is hidden? PE firm's lawyers have become specialists at burying “carve-outs” deep in the hundreds of pages (sometimes 1000+) of documentation accompanying a bond sale.

Carve-outs are exceptions to the rule that are supposed to be narrow, but lawyers can make them incredibly broad with a couple of subtle tweaks.

For example: last month Lowell-GFKL (a "credit management services" company, or "debt collector" in plain English) raised a bond, which tried to include a subtle but incredibly nasty tweak to a standard term.

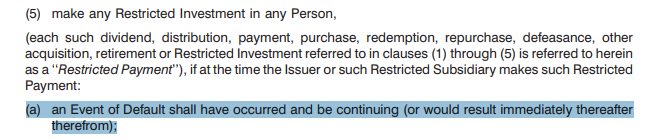

High-yield bonds typically have a restriction that stops a company from paying out dividends to its owners if it has defaulted. I do not have to explain why this is important!

This halt on "restricted payments" is usually drafted as: "a Default or Event of Default shall have occurred".

Lowell's deal deleted the "Default" part, to just leave "Event of Default"

Lowell's deal deleted the "Default" part, to just leave "Event of Default"

To a layman, this sounds the same. But there is an incredibly important distinction.

If you miss an interest payment, it's a default. But the formal "event of default" doesn't happen until 30 days later, as the bonds have a grace period.

If you miss an interest payment, it's a default. But the formal "event of default" doesn't happen until 30 days later, as the bonds have a grace period.

By deleting the default part, the company could miss an interest payment, and then strip a load of cash out of the business before formally defaulting. That is really bad!

The good news: investors noticed this on Lowell-GFKL's deal and made them put "default" back in, restoring the protection.

The bad news: several deals last year had the "default" part deleted, but the buyside didn't notice.

The bad news: several deals last year had the "default" part deleted, but the buyside didn't notice.

Can you imagine what it's like to be doing business with a counterparty that is constantly trying to trick you?

"Oh sorry guys, you didn't notice that we deleted two words on page 363 of the documentation, so you can't stop us hollowing out the business before default!"

"Oh sorry guys, you didn't notice that we deleted two words on page 363 of the documentation, so you can't stop us hollowing out the business before default!"

When caught out on covenants, PE sponsors and the bankers running their deals often say "Sure, the optionality is there, but we'd never actually use it!"

But when the shit hits the fan, PE firms do use this optionality. Remember that thing about maximising value for LPs?

But when the shit hits the fan, PE firms do use this optionality. Remember that thing about maximising value for LPs?

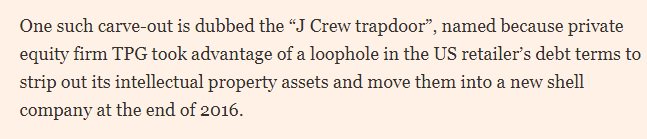

The most famous recent nasty carve-out is called the "J Crew trapdoor". This is because TPG used such a term to pull the rug out from underneath the US retailer's lenders.

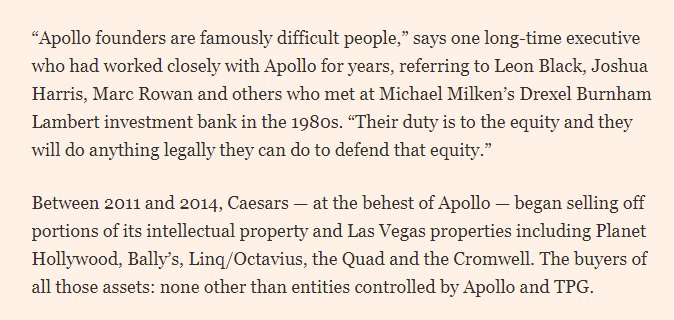

When bankruptcies get messy, private equity firms will use every avenue they can to take assets away from their lenders. Caesar's bankruptcy is a case study in this, see @sindap's big read:

ft.com/content/a0ed27…

ft.com/content/a0ed27…

The problem is, in contrast to the US, European high-yield hasn't really had a proper default cycle in a long while. European investors don't have much recent experience of being fucked on covenants, so they have less incentive to focus on it.

If the default cycle picks up, however...

Well. Anyway. Now hopefully you know why covenants are important!

Well. Anyway. Now hopefully you know why covenants are important!