,

22 tweets,

10 min read

Read on Twitter

📣 THREAD: On Saturday, @SpeakerPelosi announced the @HouseDemocrats will be unveiling “sweeping legislation to protect people w/pre-existing conditions & lower healthcare costs” tomorrow. I’m 99.9% certain this refers to #HR5155, introduced last year: acasignups.net/19/03/24/its-o… 1/

@SpeakerPelosi @HouseDemocrats Assuming this is accurate, #HR5155 would include 15 provisions to REPAIR and STRENGTHEN the #ACA.

All of these are important, but some would have a more obvious impact than others. The two biggest are 1) removing the 400% FPL subsidy cap and 2) beefing up the subsidy formula.

2/

All of these are important, but some would have a more obvious impact than others. The two biggest are 1) removing the 400% FPL subsidy cap and 2) beefing up the subsidy formula.

2/

@SpeakerPelosi @HouseDemocrats So, how much would making these first two changes reduce premiums? Let’s take a look!

acasignups.net/19/03/25/how-m…

3/

acasignups.net/19/03/25/how-m…

3/

@SpeakerPelosi According to @HealthPocket, the avg. *unsubsidized* ACA-compliant Silver policy premium for a single adult is $376/mo for a 30-year old; $423/mo at 40; $591/mo at 50 and $898 at 60. ACA subsidies are based on the “benchmark Silver” premium, which these should be very close to. 4/

@SpeakerPelosi @HealthPocket These numbers will obviously vary widely by state, carrier, plan, age, etc…but they should be pretty representative overall. Remember, Silver plans cover ~70% of medical expenses. Yes, I know these plans generally include high deductibles—I’ll get to that tomorrow. 5/

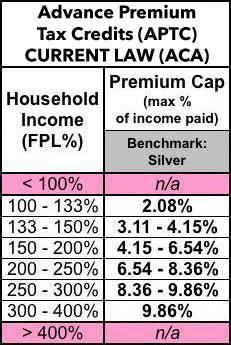

OK, so under the CURRENT #ACA premium subsidy formula, if you earn between 100-400% FPL (roughly $12.5K - $49K/year if you live alone), you're eligible for APTC subsidies on a sliding scale. If you're below 100% FPL, you're *supposed* to be on Medicaid (below 138% really). 6/

Unfortunately, 14 states still haven't expanded Medicaid, and a few which have done so are trying to gum up the works. That's a discussion for another thread, although it's *partly* addressed by #ACA 2.0 as well. 7/

Meanwhile, at the *upper* end, if you earn even $1 MORE than 400% FPL, under current law you're not eligible for ANY financial assistance. This is called "The Subsidy Cliff" and it's been one of the biggest sources of anger/complaints about the ACA over the past few years. 8/

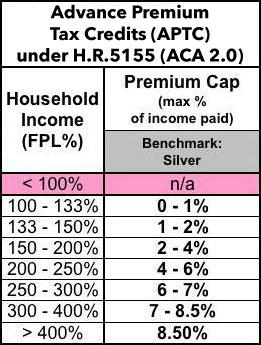

So, how does #HR5155 address these issues? Here's the revised subsidy formula. As you can see, it removes the upper 400% FPL cap while also reducing the % of income that enrollees have to pay for the benchmark Silver plan. It also eliminates the lower-end 100% FPL cliff... 9/

...so that those who cross over the 100% FPL income threshold (in non-expansion states) don't immediately have to start paying 2% of their income. Instead of ranging from 2-10% w/subsidies cut off over 400% FPL, it ranges from 0-8.5% with no hard eligibility cut-off point. 10/

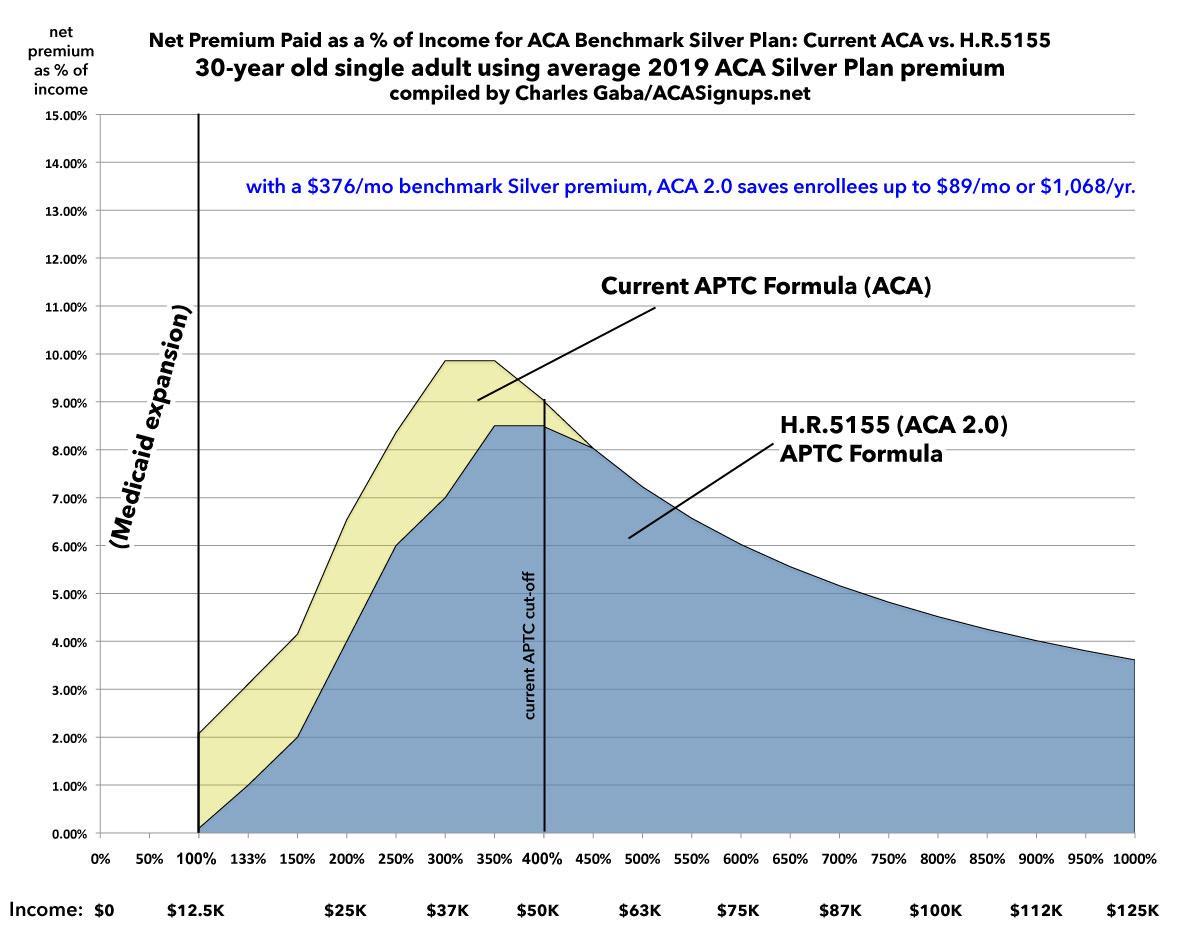

So what does this look like in practice? Remember, I'm using HealthPocket's 2019 average premiums for a SINGLE ADULT. Family plans would vary depending on household members, ages etc.

OK, let's start out with a single 30-year old...the so-called "Young Invincible". 11/

OK, let's start out with a single 30-year old...the so-called "Young Invincible". 11/

The avg. Silver premium for a 30-year old is $376/mo.

Currently, if they earn $25K/year, they only have to pay $136/mo.

Under #ACA 2.0, they'd only have to pay $83/mo, saving an additional $636/year.

If they earn $37K, they'd go from paying $308/mo to $219, saving $1,068.

12/

Currently, if they earn $25K/year, they only have to pay $136/mo.

Under #ACA 2.0, they'd only have to pay $83/mo, saving an additional $636/year.

If they earn $37K, they'd go from paying $308/mo to $219, saving $1,068.

12/

At 30 years old, the 400% FPL cap isn't really a factor since benchmark premiums barely hit the income threshold anyway. Here's what it looks like visually: The light area is the % of income paid under the CURRENT formula; the dark area is how this would change under #HR5155. 13/

OK, so that's up to $1,000 or more saved for 30-year olds. Actually, in all 4 cases, the premium reduction for those earning 100-400% FPL would be the same...anywhere from around $250 - $1,100 in additional savings per enrollee per year or more in some states. 14/

Next, the 40-year old: They'd save $250-$1,100 if they earn between 100-400% FPL...but look what happens at $50,000 income: They go from paying full price ($423/mo) to getting $69/mo in subsidies, saving over $800/year. At this age, subsidies taper off at around 450% FPL: 15/

At 40, the "subsidy cliff" looks more like a speed bump...but just wait.

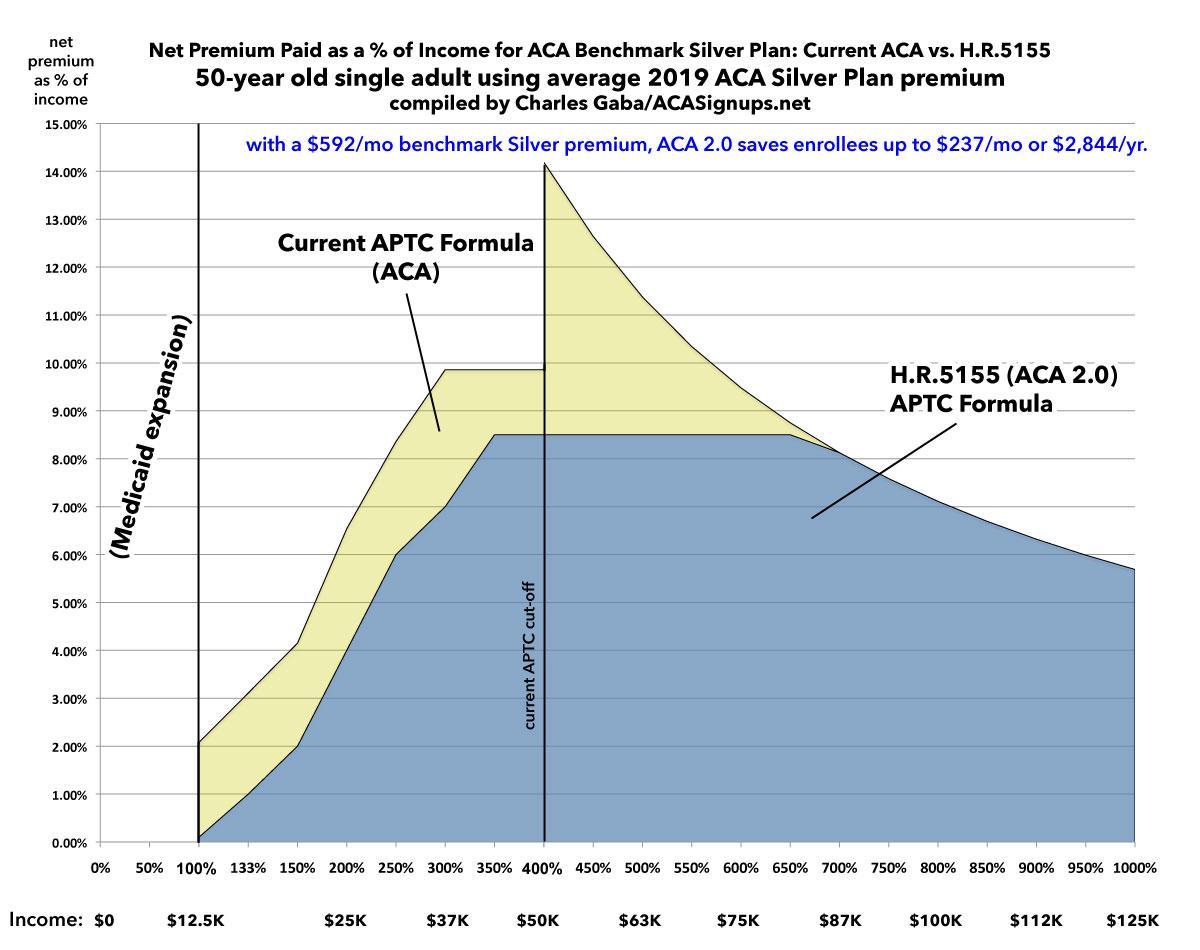

At 50 years old, under the *current* ACA subsidy formula, if you go from earning $49,960 (400% FPL) to $50,000 (401% FPL) your net premium IMMEDIATELY jumps from $376/mo to $592...a 57% spike! 16/

At 50 years old, under the *current* ACA subsidy formula, if you go from earning $49,960 (400% FPL) to $50,000 (401% FPL) your net premium IMMEDIATELY jumps from $376/mo to $592...a 57% spike! 16/

Under #HR5155, by removing the 400% FPL cap, this spike is not only eliminated, but the $50K earner wold pay just $355/mo...reducing their premiums by over $2,800/year.

Here's what that looks like...and now you understand why it's called a "Cliff":

Here's what that looks like...and now you understand why it's called a "Cliff":

That big triangular-shaped area between the 400-650% FPL income range is the source of most of the complaints you've heard about ACA plans being crazy expensive. These are also the people who've been FURTHER hurt the most by Trump/GOP via CSR cut-off & mandate repeal. 18/

BUT SIT DOWN FOR THIS ONE: Check out what happens at *60* years old.

I'm going to just post the chart, because it tells the story better than words can:

I'm going to just post the chart, because it tells the story better than words can:

For a single 60-year old, the Subsidy Cliff is a Chasm. In a worst-case scenario (Natrona County, Wyoming), a 64-year old earning more than 400% FPL currently has to pay an insane $2,050/month at full price. That's nearly $25,000/year, which is insane for most people. 20/

It's so absurd I'm sure it's hypothetical; I can't imagine any 64-year olds in Wyoming are enrolled in an exchange plan today.

Under #HR5155, they'd only pay 8.5% of their income no matter what: $4,250 if they earn $50K; $6,375 if they earn $75K; $8,500 if they earn $100K. 21/

Under #HR5155, they'd only pay 8.5% of their income no matter what: $4,250 if they earn $50K; $6,375 if they earn $75K; $8,500 if they earn $100K. 21/

That's it for now. I'll address other #ACA 2.0 provisions (including addressing deductibles, the family glitch, etc) in the future.

If you find these explainers helpful and would like to support my work, please do so here, thank you! acasignups.net/donate /END

If you find these explainers helpful and would like to support my work, please do so here, thank you! acasignups.net/donate /END