Below my new short paper on Argentina and sovereign debt restructuring challenges: papers.ssrn.com/sol3/papers.cf…

@AGelpern @MattHGoldmann @astridiversen @mweidemaier @colbyLsmith @RobinWigg @TimRSamples @KPatricio1 @Martin_M_Guzman @ManuelidesY @jzettelmeyer @Brad_Setser @PIIE 1/18

@AGelpern @MattHGoldmann @astridiversen @mweidemaier @colbyLsmith @RobinWigg @TimRSamples @KPatricio1 @Martin_M_Guzman @ManuelidesY @jzettelmeyer @Brad_Setser @PIIE 1/18

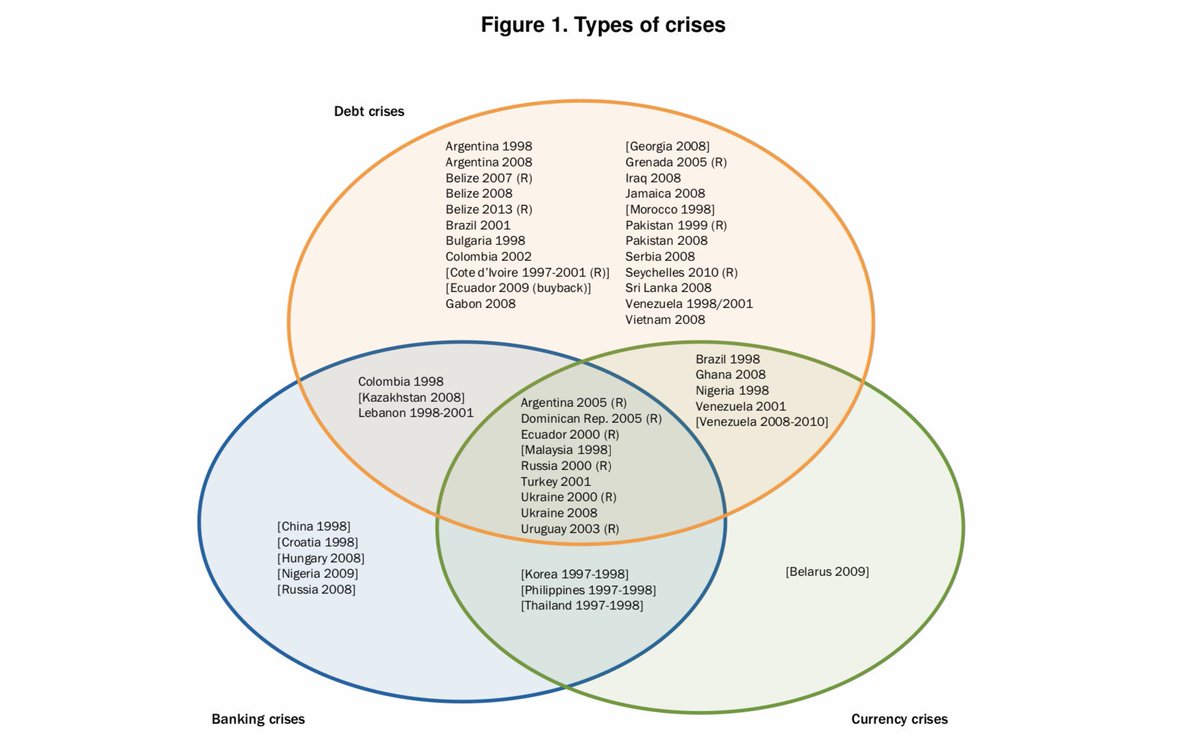

Argentina currently finds itself in a vulnerable financial and fiscal situation and a sovereign debt restructuring has become a real possibility - not only for financial markets but also the new administration. ft.com/content/ec4cb3… 2/18

The Republic of Argentina’s total outstanding debts, including debts of public sector agencies, such owed to the private sector, and debts to multilateral and bilateral debt, amount to USD337 billion, or 80.7% of GDP. argentina.gob.ar/sites/default/… 3/18

Argentina has a complex financial indebtedness structure which includes, in essence, the following types of instruments:

1)Domestic debt,

2)International sovereign bonds,

3)IMF loans, and

4)Credit facilities with multilateral and commercial financial institutions. 4/18

1)Domestic debt,

2)International sovereign bonds,

3)IMF loans, and

4)Credit facilities with multilateral and commercial financial institutions. 4/18

Since 2016, Argentina has issued a total of 51 international sovereign bonds with a total issued amount of USD135 billion, of which 45 bonds with a face value of USD121 billion are currently outstanding. Of these bonds, 2 are denominated in CHF, 5 in EUR and 44 in USD. 5/18

As regards IMF loans, the IMF completed its latest Review of Argentina’s program in July 2019, allowing the disbursement of another USD4.3 billion, bringing total disbursements since June 2018 to USD44.1 billion (3/4 of the amount available under the SBA (USD57 billion)). 6/18

Bloomberg data on multilateral, bilateral, and commercial loans denominated in USD seems somewhat less reliable. Leaving those concerns aside, the total outstanding amount of USD loans, excluding IMF loans, stands at approximately USD17.2 billion. 7/18

With respect to Argnetina's debt maturity profile, the chart below is instructive - it essentially shows that several big (local & foreign currency) payments are due in 2020 and 2021 and large IMF loan repayments in 2022 and 2023. 8/18

The design of a debt restructuring will, among other factors, be informed by the legal risks associated with a large-scale debt swap - particularly the risk of holdout creditors seeking to disrupt the negotiations (by virtue of litigation in New York courts). 9/18

While there are few legal obstacles when it comes to the reprofiling or restructuring domestic-law debt (which do not even include acceleration or cross-default clauses), the same is not true for foreign-law bonds. 10/18

The biggest issue at this stage, which M. Gulati @mweidemaier and @AGelpern have aptly discussed, is that thethe Collective Action Clauses in the pre-2016 bonds ("Kirchner bonds") have different voting thresholds than the post-2016 bonds ("Macri bonds"). 11/18

The price differential between these two types of bonds suggests that holdouts are speculating that they may block the restructuring of "Kirchner bonds", given that they require two votes (one aggregated vote and one in each series), making blocking tactics easier. 12/18

To add injury to insult, the prospectus language in the "Macri bonds" suggests that they need to be restructured together with "Kirchner bonds", raising difficult design questions if holdouts block the CAC vote in the latter types of bonds. 13/18

bloomberg.com/news/articles/…

Another legal issue to be considered is that "Kirchner bonds" have almost the same pari passu clauses as the infamous 1994 FAA that was the basis for the NML v. Argentina litigation (see FT article below).

ftalphaville.ft.com/2013/08/23/161… 14/18

Another legal issue to be considered is that "Kirchner bonds" have almost the same pari passu clauses as the infamous 1994 FAA that was the basis for the NML v. Argentina litigation (see FT article below).

ftalphaville.ft.com/2013/08/23/161… 14/18

As regard IMF loans, it is worth recalling that the IMF enjoys de-facto preferred creditor status (PCS). While the IMF’s Articles of Agreement make no reference to the Fund’s PCS, States have accepted the IMF’s de-facto priority for decades (with some exceptions). 15/18

However, the IMF Stand-by-Agreement didn't include any cross-default clauses, which means that a default on IMF loans would not trigger any acceleration rights for international bondholders. The same seems to be true for loans provided by other multilateral lenders. 16/18

Overall, Argentina still finds itself in a legally superior position compared to its 2001 default: CACs have become more resilient to holdout tactics and U.S. courts have partially reversed the unconventional rulings that brought Argentina to its knees in 2014. 17/18

Sovereign bond restructurings rest on the basic premise of bondholder democracy: as long as a sufficient majority of creditors accepts a restructuring offer, most legal obstacles can be overcome. Still, holdouts lurk in the corners of Argentina's bond prospectuses. 18/18

Below some links to the super insightful contributions by @mweidemaier/ Gulati and @AGelpern

creditslips.org/creditslips/20…

creditslips.org/creditslips/20…

creditslips.org/creditslips/20…

creditslips.org/creditslips/20…

creditslips.org/creditslips/20…

creditslips.org/creditslips/20…