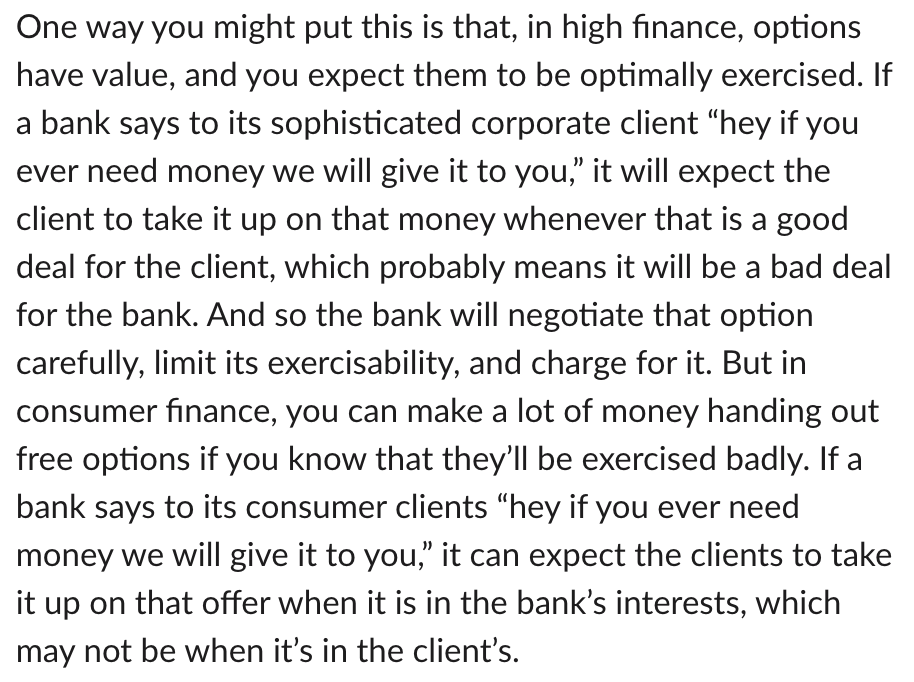

Matt Levine's column interesting as always. I'd like to point to one bit in particular, which is applying optionality to bank decisions to extend credit.

(Optionality is one of those great financial lenses which you can apply to *so* many things fruitfully.)

(Optionality is one of those great financial lenses which you can apply to *so* many things fruitfully.)

When you buy an option (or receive one for services rendered, a common case in tech), you're buying the right but not the obligation to be able to engage in a transaction in the future at a locked in price.

There is deep, rich literature and experience on pricing these.

There is deep, rich literature and experience on pricing these.

To a first approximation, Matt is probably right with respect to claims that sophisticated financial firms understand option value and exercise it close to optimally. Consumers largely do not.

I think it's worth mentioning that a optionality is a great lens for the world but the abstraction is occasionally a leaky one.

In particular, true options are *durable.*

In particular, true options are *durable.*

If the option blows up in the face of the party writing it (generally a financially sophisticated party), they are precommiting to *still paying you as promised.*

They can e.g. buy them back from you at a mutually agreeable price or otherwise offset exposure, but can't default.

They can e.g. buy them back from you at a mutually agreeable price or otherwise offset exposure, but can't default.

This is crucially different than offers of credit, which *are often not* true options, and that's useful to understand as consumers of them.

A bank (or other lender) which offers revolving lines or credit facilities keeps track of both all draws and all notional exposure.

A bank (or other lender) which offers revolving lines or credit facilities keeps track of both all draws and all notional exposure.

In the event economic circumstances for your lender change or their view of your risk profile changes, unless they've contractually committed availability to you, they probably can retroactively change your limits at basically any time allowed by your contract.

If you do not remember this being a central feature of the discussion your lawyers had with their lawyers, *probably did not* successfully negotiate guaranteed access to the thing credit they have offered to extend you.

This is true for consumers and businesses alike.

This is true for consumers and businesses alike.

Many businesses have been burnt when the macro environment changes from widespread availability of credit to non-availability quickly, including sophisticated financial firms. (Reluctance of the repo markets to offer capacity as widely Tuesday as Monday contributed to the GFC.)

You can mitigate this, as a consumer of credit (B2C or B2B) by having multiple independent funding sources and, of course, by keeping a cash buffer around.

Historically it was operationally difficult for banks to adjust credit lines, but that better adoption of technology (data sources about credit risk, data science applied to your transactions and bank's proprietary data, overall better IT posture) allows this to be *fast*.

This makes the process more efficient and less risky for lenders, which at the margin should counsel them to offer higher limits to more marginal customers than they'd otherwise be comfortable with.

But those limits "mean less" than many people might assume they do.

But those limits "mean less" than many people might assume they do.

Example: there is one particular US bank that I've used in a personal capacity for a very long time. I'm a pretty good credit risk.

Back in I think 2012, when I was also a pretty good credit risk, they were uncomfortable giving me any more than $X of total exposure.

Back in I think 2012, when I was also a pretty good credit risk, they were uncomfortable giving me any more than $X of total exposure.

Over the last few years, I've not had bank-legible changes in circumstances, but should still read as "Yep, still a pretty good credit risk."

Their messaged appetite for exposure to it is something like 3~4 times more than $X, and $X wasn't a small number either.

Their messaged appetite for exposure to it is something like 3~4 times more than $X, and $X wasn't a small number either.

That is likely downstream of "Well, we're not *really* taking on 4X of risk from you. You barely even saturated the $X for most of your years with us. If your financial circumstances change extraordinarily rapidly and you go crazy with charging things, we'd derisk *in seconds.*

So why do banks offer you "more credit than you need"?

I mean, to make money, but the mechanisms are more interesting than that.

One is to protect their share of wallet.

I mean, to make money, but the mechanisms are more interesting than that.

One is to protect their share of wallet.

Banks broadly do not believe they have material edges in underwriting consumers: if you are a) a very good credit risk and b) use a lot of credit, banks perceive that it is highly likely all of their competitors will believe the same two things about you, particularly over time.

(An interesting market opportunity for banks is specializing in people whose circumstances are specialized such that the technology which enables the last tweet, such as credit reports and FICO scoring, does not correctly bucket them as low-risk but where they still borrow lots.)

So if banks think "Well, if we don't extend credit at the margin our competitors certainly will", whereas previously they might be OK losing the opportunity for your business to protect their risk profile, these days they want you to *know* you have headroom on your card.

"I don't want to lose a single business trip worth of expenses to Amex just because they were worried about going over and MOST PARTICULARLY I do not want Amex to get their transactions *next month, too* because of an opportunity to change habits or stored cards."

That is also downstream of the increasing computerization of user spending behavior: previously, the jargon was literally "We want to be 'top of wallet'; the card our customer habitually reaches for first."

The expectation is all other cards are a short distance away in wallet.

The expectation is all other cards are a short distance away in wallet.

When your business runs transactions monthly on AWS or you personally have a card installed on Apple Pay, though, the difference between "top of wallet" and the next card is *gigantic*.

Your "next card" isn't on the system charging you money and probably isn't on *you* either!

Your "next card" isn't on the system charging you money and probably isn't on *you* either!

You'll note that "Ahah, they are trying to trick you into spending more than you can afford" is a very different narrative from "Ahah, they are hoping you concentrate more of your transactions on them this month, pay back quickly, and come back for more next month."

There exists a heterogeneity of strategies and a wide distribution in customer behavior. Some banks (and some products at a particular bank) might be caricatured as being more of the first, and some more of the second. And some are both, for different people.

Financially unsophisticated people, including very smart financially unsophisticated people, often believe "Banks can't make any money from you if you are a responsible user of credit. They want you to get in over your head."

This is false as stated.

This is false as stated.

Banks sell financial services. Sometimes the pricing is a little opaque to the end user, because it is subsidized by someone else.

If you consume a lot of financial services, and banks are eagerly courting your business, it is *probably not* because they're bad at math.

If you consume a lot of financial services, and banks are eagerly courting your business, it is *probably not* because they're bad at math.

A concrete example: which of the following two customers is more lucrative?

A: Spends $10k. This strains them; they can pay back the minimums, but it will take them years to pay off, at a 15% APR the whole while.

B: Spends $10k monthly. Never pays a cent in interest.

A: Spends $10k. This strains them; they can pay back the minimums, but it will take them years to pay off, at a 15% APR the whole while.

B: Spends $10k monthly. Never pays a cent in interest.

Answer: depends *almost entirely* on what it cost the bank to acquire and keep B's business, because B is *printing money* via interchange.

A contributes about ~$1.3k of revenue per year (plus $200~$300 in month 1).

B contributes about $2.5~$3k annually.

A contributes about ~$1.3k of revenue per year (plus $200~$300 in month 1).

B contributes about $2.5~$3k annually.

(Should insert a *plausibly* before "contributes" because there are actually a lot of different interchange rates the issuer could be receiving depending on product, jurisdiction, card brand, regulation, etc, and I should clarify "I'm being very handwavy on math here.")