1/ The VIX Premium (Cheng)

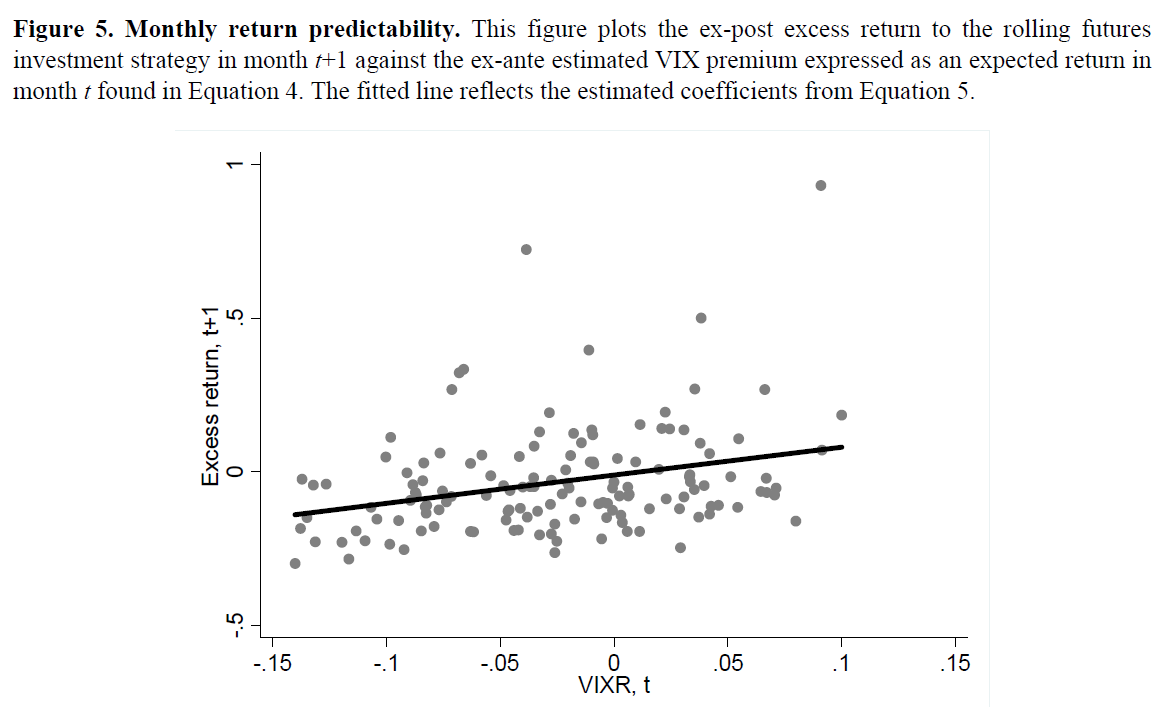

"Ex-ante estimated premiums predict ex-post returns to VIX futures with a coefficient near one, and falling ex-ante premiums predict increasing ex-post market and investment risk, creating profitable trading opportunities."

papers.ssrn.com/sol3/papers.cf…

"Ex-ante estimated premiums predict ex-post returns to VIX futures with a coefficient near one, and falling ex-ante premiums predict increasing ex-post market and investment risk, creating profitable trading opportunities."

papers.ssrn.com/sol3/papers.cf…

2/ "When ex-ante measures of risk have risen, the estimated VIX premium has tended to fall or stay flat before rising later.

"Low estimated premiums are typically followed by low realized premiums and vice versa.

"Results are similar across a wide range of forecast models."

"Low estimated premiums are typically followed by low realized premiums and vice versa.

"Results are similar across a wide range of forecast models."

3/ * Front-month VIX contract rolled each month

* VIX premium is estimated as the difference between the futures price and the forecasted VIX price based on an ARMA(2,2) model (estimated using out-of-sample daily data)

* VIX premium is linearly scaled to premium per 21-day period

* VIX premium is estimated as the difference between the futures price and the forecasted VIX price based on an ARMA(2,2) model (estimated using out-of-sample daily data)

* VIX premium is linearly scaled to premium per 21-day period

4/ "The VIX premium initially falls or stays flat before rising later when risk rises, posing a puzzle for standard models of risk/return."

This holds outside of the 2008 crisis, for other VIX forecast models, other contracts along the term structure, and other measures of risk.

This holds outside of the 2008 crisis, for other VIX forecast models, other contracts along the term structure, and other measures of risk.

5/ The effect does not appear to be unique to the ARMA forecast model that the author initially used:

6/ In response to a 1-standard deviation shock to realized volatility, "the premium decreases on impact before rising again in the full sample. In the 2010-onwards sample, the initial decline in the premium reverses in the first month."

7/ "Futures prices rise by less than the conditional forecast in response to a risk shock. For a large shock, the forecast increases so much more than the futures price that the premium becomes negative (and expected returns become positive)."

8/ "If anything, falling premiums predict higher risk... Premiums and risk do not move together, and if anything, have moved with the opposite sign. A short investor who sees estimated premiums falling can close his position and sidestep ex-post low-profit, high-risk situations."

9/ After transaction costs (bid-ask spreads), timing strategies based on the sign of the forecasted VIX premium have historically worked (positive Carhart alphas).

Skewness and drawdowns are also improved.

Skewness and drawdowns are also improved.

10/ "The long/short strategy provides an annualized alpha of 10.9% that is not statistically different whether the strategy is long or short."

11/ "Dealers and asset managers (institutional investors, pension funds, insurance companies) tend to expand long futures positions as the premium rises, while hedge funds and other reportable traders expand short futures positions."

12/ "Increases in risk tend to lead to reductions in long positions by dealers and asset managers (and reductions in short positions by hedge funds).... This is consistent with shocks acting to *reduce* hedging demand.

"Traders respond similarly to VVIX shocks."

"Traders respond similarly to VVIX shocks."

13/ "Increases in systemic risk measures are associated with dealers closing positions, and these measures also increase with market volatility.

"Declines in customer demand and dealer risk appetite help explain why dealer hedging declines when risk rises."

"Declines in customer demand and dealer risk appetite help explain why dealer hedging declines when risk rises."

14/ "VIX futures returns are consistent with those of short-term forward variance strategies. They are correlated with measures of spot 30-day variance risk premiums and share common variation that helps explain other asset prices."