SBI Cards IPO: long thread on valuation disasters in Indian markets & how these rip off the retail investors: Basic stats first:

13 crore shares offered out of total of 93 crore stocks. 14% float at Rs 750 per share is valuation of Rs 70 thousand crore to SBI Cards. #sbicards

13 crore shares offered out of total of 93 crore stocks. 14% float at Rs 750 per share is valuation of Rs 70 thousand crore to SBI Cards. #sbicards

This US $ 10 Billion market cap. They say this is the only card company getting listed so a great opportunity. We’ll see some numbers & benchmarks internationally. At FY'19 profits of Rs 862 crore & EPS =Rs 9.43, we get a Price Earning ratio of 80 !!

I know many will justify citing the growth prospects. I have a few questions to explore.Firstly, what is the highest PE of any mature financial company in India? Look at HDFC bank, Kotak, etc & we see much modest PEs of 25 to 35 for HDFC Bank & Kotak. And they are richly valued.

But there is a track record of 20 yrs & more for these banks. Many argue that credit cards is a growing industry & has huge potential to penetrate, unlike some mature retail banks that are settling at much modest growth numbers of 20% now. PE multiples have accordingly matured.

Do you think that credit card is different than retail banking & is in a super-normal growth phase in India? Think again. You just need to read beyond the headlines & dig in more data. SBI cards has been around for more than 20 years now in market.

And last 20 years have seen the card industry mature & evolve reasonably well. It has hit the maturity phase quite sometime back in terms of penetration. Look at the table below to understand this:

In-fact there are many players who chose to shrink in size after 2008 rather having paid the price of reckless growth that the Indian market is not ready for. Citi, ICICI, Amex, StanC & HSBC prove the point that card industry in Indian has limited penetration potential.

See how the overall credit card lending shrank during 2009 & 2015. The red block is getting thinner. Same story happened with education loans that grew & then reached maturity soon enough. Then just receded from that point.

HDFC did well as it issued cards only to the bank customers where it has an implied collateral of bank deposits. As long the FD is intact, the customer won’t default on the card. If they do, well the bank & manage the rest. That strategy proved right.

SBI cards has a different problem through. While SBI has crores of customers, most are not credit worthy & have marginal balance. Additionally, most SBI customers are old generation conservatives that don’t like to use digital payments at all. A small anecdote fits well here.

I can recall 2003 when SBI cards issued free cards to all PPF customers under some agreement. The sales pitch was simple – “Sir, SBI is issuing free credit card since you hold a PPF account. Branch mgr wants us to give you this gift ! Just sigh here pls.” Boom. A card is created.

This policy got close to a million new customers to SBI cards but at what cost? Card company doesn’t make money by issuing cards. It wants people to use cards for credit. The card usage for PPF customers of SBI was not even 20%. So 80% of those never used the card even once.

So, this talk of having access to SBI customer database is a tried tested theory that doesn’t work. Well it works to get the new card issues in the short run but lack of such card usage doesn’t get any money to SBI cards eventually. So it is just a window dressing.

I see a similar narrative being built now. SBI cards IPO document doesn’t include much details around the history before 2015. The years before that were all about a shrinking industry, all this when the overall credit in retail was having a best of time.

It’s just in the last few years that the industry has again seen some fresh spends & new cards. However, most banks are staying away from any reckless growth, They all have learned the history well & will expand only a limited pace that the market can absorb.

Everyone wants to be rational. However, when you’re looking to list thru an IPO, the priorities are different. SBI Cards issues cards outsmarting every competitor. It doubled the workforce every year for last 2 years. See the employee expenses in 2017, 2018 & 2019 below.

Why does this happen ? Well because someone wants to issue cards at much faster pace vs the competition. Other banks don’t care as they want profitable growth with stable rates. But SBI cards wants a profitable exit, not sustainable growth. So, we get this.

While HDFC bank, is happy with stable market share, Kotak is in-fact reducing the cards to optimize profitability, one player is in a tearing hurry to issue cards, It issues 45% of credit cards in India in the most recent month reported. Who is this player in a hurry ?

SBI Cards

SBI Cards

Lending business however works very differently. You can always grow by lending money fast. The real fun actually starts later when you have to get the money back. Doesn’t look like a top priority for the company as of now.

So, the below growth numbers in spends & market share doesn’t impress me. If HDFC & Kotak with their proven lending practices are not growing, I would worry if some else is. SBI Cards is stable till 2017 & then suddenly grew by 100% in 2 years till 2019. Not a consistent trend.

Notice another pointer in the date above. Citibank with just 6% of cards share has 13% or spends. SBI cards takes 18% cards share to generate a 16% share in spends. Citibank is chasing profitable customers & is almost not increasing its cards base.

SBI just wants to increase cards issued. The fact that many may not even open the envelope is not important for now it seems. I would less impressed by the “reach & depth” of SBI branch network. Those are not the credit card customers you need.

Another look at the channel sales data throws the same conclusion. Look how the share of sales from SBI branch channel has increased from 35% in 2017 to 45% in 2018 to 55% in 2019. Hmmm…..more PPF cards I guess. Will that issuance make money ? I doubt it.

Armed with this background, lets get back to the IPO valuation. Is it worth a buy ? Let’s see.

So, with a FY’19 PE of 80 , if someone tries to sell me the story of growth in cards issued over last 5 yrs(which basically is in last 2 years), I’m not going to buy it.

So, with a FY’19 PE of 80 , if someone tries to sell me the story of growth in cards issued over last 5 yrs(which basically is in last 2 years), I’m not going to buy it.

The stable cards base of SBI cards is 3.6 Mn that it had till 2017, just before the window dressing started ¬ the 8 to 10 Mn number that SBI wants us to believe. The growth in last 2 years will produce lots of dead cards but not profits.

I see the rise in spends but that’s keeping in line with industry trend. The peak however is quickly reached in India & delinquencies follow soon-after. If HDFC, Kotak, have stabilized, I don’t see why SBI could grow so fast & not profitably. And it has seen bad debts in 2008.

Finally at US $ 10 Billion valuation, I think it is quite generously valued. While there are no Indian card companies listed, we can compare this broadly to Discover Financial & Capital One in USA.

Discover with $ 74 BN in credit card assets is valued with market cap of $ 20 BN. SBI cards with assets of just $ 3 BN is valued at $ 10 Billion ??? Someone is definitely being very bullish here.

Just to put this number in context, see the market cap of Indian banks below:

HDFC Bank - $ 92 BN

ICICI Bank - $ 45 BN

Kotak Bank - $ 44 BN

Axis Bank - $ 28 BN

IndusInd Bank - $ 11 BN

Do you think that credit card arm of SBI is equal to entire IndusInd bank & 1/3 of Axis bank?

HDFC Bank - $ 92 BN

ICICI Bank - $ 45 BN

Kotak Bank - $ 44 BN

Axis Bank - $ 28 BN

IndusInd Bank - $ 11 BN

Do you think that credit card arm of SBI is equal to entire IndusInd bank & 1/3 of Axis bank?

Fair valuation for PE firm CA Rover looking to pull capital invested. For investors, I guess you’ll be buying something at 3 times the actual price. Will I put my money on it? Absolutely not. There is no money left on the table. And I don’t believe in paying for PE firm profits.

Detailed answer on quora. qr.ae/p7d789. I thought you'll like this thread @deepakshenoy @moneybloke @szarabi

Some bullish folks argue that a forward PE of 45 is cheap for #sbicardIPO . Carlyle group invested Rs 2000 crore in 2017 end for 25% stake. It’ll now be valued Rs 18,200 crore ! That’s 9 times in 2 years ? I don’t think Indian card industry changed so much in 2 yrs. Do you ?

So in just 2 years, Carlyle group walks away with Rs 2500 crore on Rs 2000 cr they invested in 2017. So capital back in pocket with a good 12% return. And they will still hold another Rs 15,700 cr stake left on company. Talk of ten bagger returns, this is how it looks like.

With 9 times investment off the table, enters our retail investor with his love and patriotism for #sbicardIPO and buys the stories of early 2000s like demographic dividend and under-penetrated market. Buys the IPO almost like a scarcity once seen at ration-shops in 1970s.

They say market is a great teacher. If this one makes money for investors, I definitely would have missed some lecture in investing !! Either way, some of us will learn some lessons for sure.....

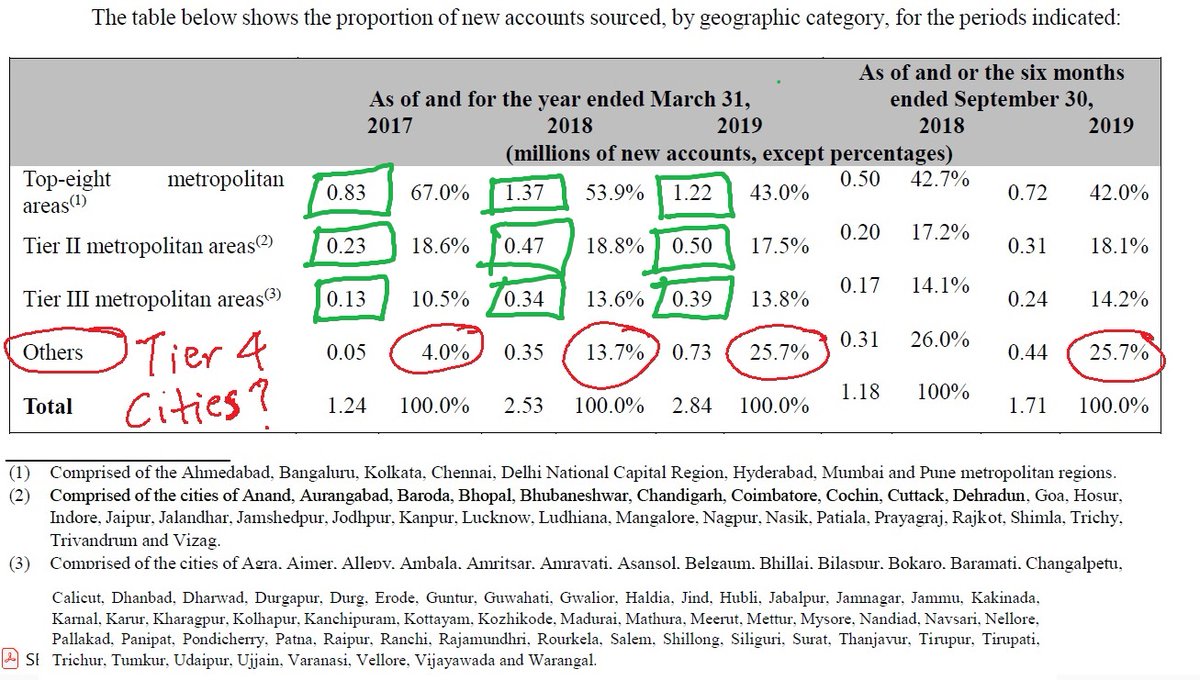

@deepakshenoy So here is the spends story of SBI cards. See the below channel sales split. See the metro & tier 2 city card sales have already stagnated from 2018 to 2019. But the incremental growth comes from "others". SBI card has not explained what others is.

But from 4% in 2017, the "others" contribute 25% of new cards in 2018 & 2019 while sales in metros have stagnated. If companyb is not growing in metros & tier 2, how can growth ever be sustainable ? Others may be either tier 4 cities which is clearly a poor call.

Tier 4 markets are not savvy with credits cards & don't understand it either This explains a sudden spike on SBI card spends in 2018 & 2019 below while other banks are much slower. All this happened in last 2 yrs post PE infusion. This will certainly blow up bad debts going ahead