,

38 tweets,

16 min read

Read on Twitter

1/ Part 3 of 4

In Part I we talked about how US stocks and bonds are primed for low future returns.

Investors should take their medicine, lower expectations, save more, and spend less.

In Part I we talked about how US stocks and bonds are primed for low future returns.

Investors should take their medicine, lower expectations, save more, and spend less.

2/ In Part II we offered one solution by expanding the opportunity set to a global asset allocation portfolio.

Investors shouldn't obsess over the exact asset mix, but rather focus on cost aware implementation for low fees and taxes.

Investors shouldn't obsess over the exact asset mix, but rather focus on cost aware implementation for low fees and taxes.

3/ In Part III today, we're going to chat about how to improve upon this basic global allocation.

But first, get out a pen or pencil. Ready?

Write down the % of your stock portfolio you have in US stocks (or local country if abroad)...

Got it?

But first, get out a pen or pencil. Ready?

Write down the % of your stock portfolio you have in US stocks (or local country if abroad)...

Got it?

4/ Your number is likely 80%. How do I know that?

I wrote a book on stock market valuations (free here: cambriainvestments.com/investing-insi…), and I used to give speeches and ask people the same question.

We'd collect the responses live, and the answer was always the same: 80%.

I wrote a book on stock market valuations (free here: cambriainvestments.com/investing-insi…), and I used to give speeches and ask people the same question.

We'd collect the responses live, and the answer was always the same: 80%.

5/ So what's wrong with that?

It's a really, really dumb idea.

It even has a behavioral description: home country bias.

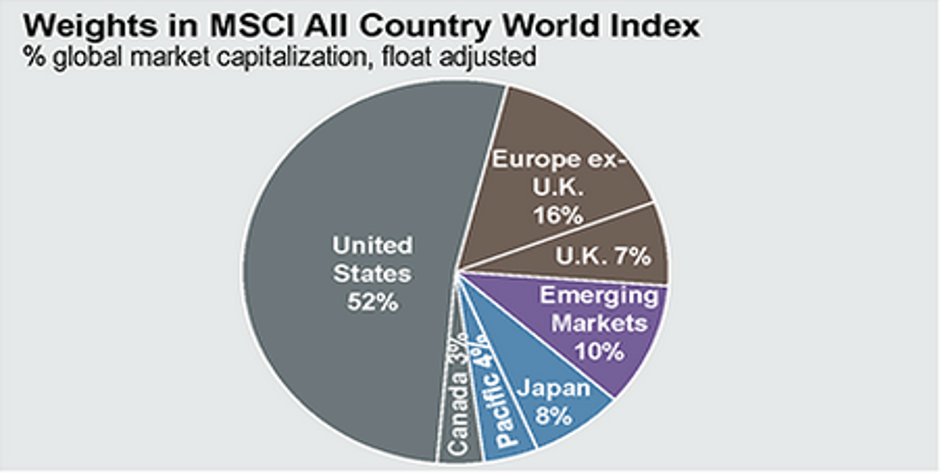

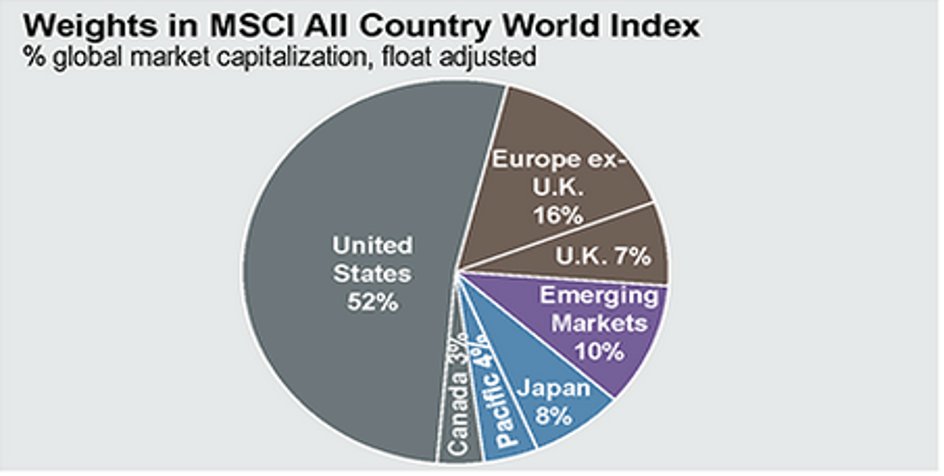

If you look at the global stock market weighted by size, the US is about half, but most of you invest 80%.

It's a really, really dumb idea.

It even has a behavioral description: home country bias.

If you look at the global stock market weighted by size, the US is about half, but most of you invest 80%.

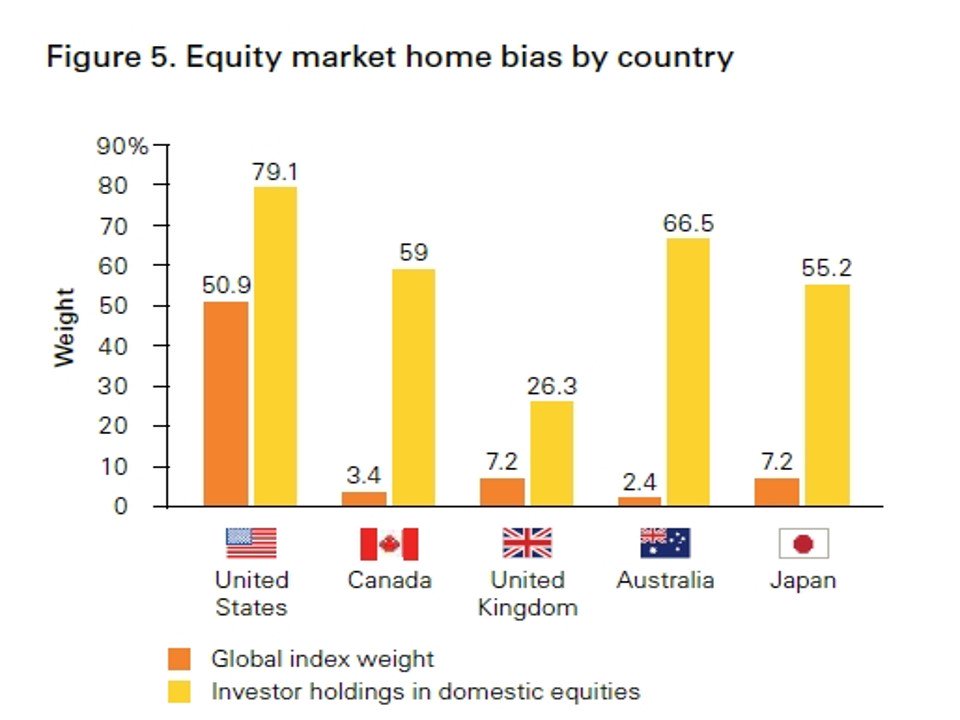

6/ Now, you are not alone.

This happens all around the world and is even more egregious elsewhere since most countries have a much smaller % of total market cap.

Chart from @Vanguard_Group

This happens all around the world and is even more egregious elsewhere since most countries have a much smaller % of total market cap.

Chart from @Vanguard_Group

7/ EVERYONE overweights their own markets...why?

They feel a false sense of comfort with "what they know". It's what they grew up with and see every day.

(And probably the same reason I'm a @broncos fan)

Let me explain why this is a really dumb idea.

They feel a false sense of comfort with "what they know". It's what they grew up with and see every day.

(And probably the same reason I'm a @broncos fan)

Let me explain why this is a really dumb idea.

8/ 52% is the true index weight.

If you're investing 80% that means you are making a massive active bet that that US stock market will outperform the rest of the world.

(Pat yourself on the back if you've been lucky and done this the past 10 years)

Bad idea - let me explain.

If you're investing 80% that means you are making a massive active bet that that US stock market will outperform the rest of the world.

(Pat yourself on the back if you've been lucky and done this the past 10 years)

Bad idea - let me explain.

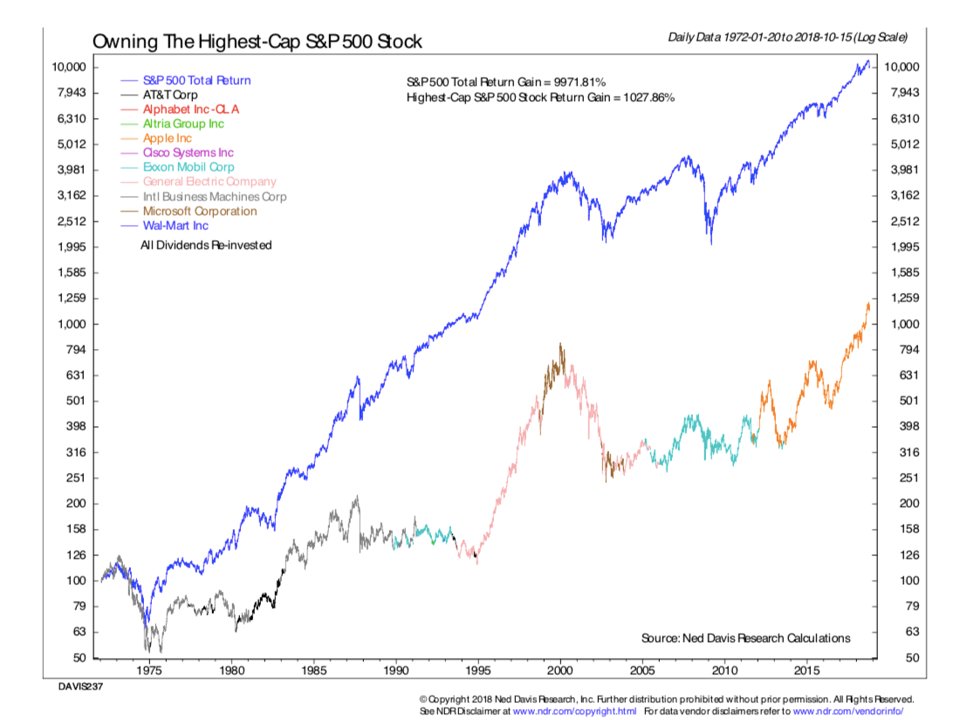

9/ The culprit is market cap weighting. This is "the market" according to the TRUE passive investor.

But why is market cap weighting sub-optimal?

Here's a chart from @NDR_Research that compares the S&P 500 to investing in the largest stock in the market at the time.

But why is market cap weighting sub-optimal?

Here's a chart from @NDR_Research that compares the S&P 500 to investing in the largest stock in the market at the time.

10/ It's a laundry list of the top American companies like @walmart, @IBM, @Google, and @Microsoft.

And it's a HORRIBLE idea. It underperforms the S&P500 by a mile...now why?

nbc.com/saturday-night…

And it's a HORRIBLE idea. It underperforms the S&P500 by a mile...now why?

nbc.com/saturday-night…

11/ It's just capitalism and its creative destruction and it's the way it should be.

By the time @apple becomes a $1 trillion company, don't you think there's a bunch of other companies that would like to make phones and billions of $ per year?

By the time @apple becomes a $1 trillion company, don't you think there's a bunch of other companies that would like to make phones and billions of $ per year?

12/ But there's also a flaw with market cap weighting in that there is no tether to fundamentals.

This surprises many people but the market index is just price. That's it, no earnings or revenue measures, just price.

So a market cap index often overweights expensive stocks.

This surprises many people but the market index is just price. That's it, no earnings or revenue measures, just price.

So a market cap index often overweights expensive stocks.

13/ @RA_Insights has some great research on the topic where they show investing in the largest stock in each market or sector goes on to underperform by 3 percentage points per year for a decade!

mebfaber.com/2016/09/07/epi…

mebfaber.com/2016/09/07/epi…

14/ This is why almost ANY weighting methodology should outperform - including equal weight, fundamental weight, or index where the CEO eats hamburgers or cheeseburgers.

But let's chat about one of my preferred weighting methods, VALUE.

But let's chat about one of my preferred weighting methods, VALUE.

15/ So years ago we wondered if the CAPE ratio from Part I would work equally well globally as it does in the US.

But no one calculated or published these so we went out and did it for all the major countries in the world.

Here is the chart through about 2015...

But no one calculated or published these so we went out and did it for all the major countries in the world.

Here is the chart through about 2015...

16/ (A number of sites now publish these and you can find my favorite valuation resources below from

@CAPE_invest

theideafarm.com

@Barclays

@RobertJShiller

@AswathDamodaran

globalfinancialdata.com

mba.tuck.dartmouth.edu/pages/faculty/… …

@CAPE_invest

theideafarm.com

@Barclays

@RobertJShiller

@AswathDamodaran

globalfinancialdata.com

mba.tuck.dartmouth.edu/pages/faculty/… …

17/ Now notice a few things.

Most of the valuation metrics in general move together (not surprising that stocks are broadly correlated.)

But often at times there is a wide spread of some monster and low valuations.

Most of the valuation metrics in general move together (not surprising that stocks are broadly correlated.)

But often at times there is a wide spread of some monster and low valuations.

18/ Market historians can certainly pick out the grandaddy of all bubbles on the left side of the chart where Japan hit almost 100.

And guess what? If you followed market cap weight you went and put most of your money in a stock market trading at a CAPE of 95. Sound reasonable?

And guess what? If you followed market cap weight you went and put most of your money in a stock market trading at a CAPE of 95. Sound reasonable?

19/ Remember the BRICs? That was a popular marketing concept in the mid 2000s when India and China were trading in CAPEs 40-60 range.

No wonder the returns have been horrible since.

No wonder the returns have been horrible since.

20/ In general sorting on value works great. It's not @elonmusk level rocket science.

Paying less for something is usually a better idea than paying more, whetether it's classic cars, houses, stocks, or 1989 Ken Griffey Jr. @UpperDeckSports cards...

Paying less for something is usually a better idea than paying more, whetether it's classic cars, houses, stocks, or 1989 Ken Griffey Jr. @UpperDeckSports cards...

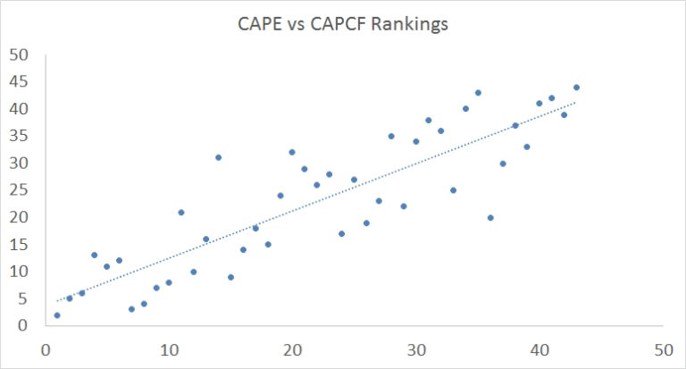

21/ And again, before you flip out about CAPE...recall that the value indicator doesn't really matter.

We track a bunch of long term metrics on theideafarm, and here is a chart of 45 countries ranked by CAPE and CAPCF (cash flow).

Pretty tight correlation.

We track a bunch of long term metrics on theideafarm, and here is a chart of 45 countries ranked by CAPE and CAPCF (cash flow).

Pretty tight correlation.

22/ Again, why does this matter?

Well because mean reversion is the most powerful force in investing.

Just when you think you are hot sh!t, the market has a way of humbling you...and when things look bleakest, better times are often ahead...

Well because mean reversion is the most powerful force in investing.

Just when you think you are hot sh!t, the market has a way of humbling you...and when things look bleakest, better times are often ahead...

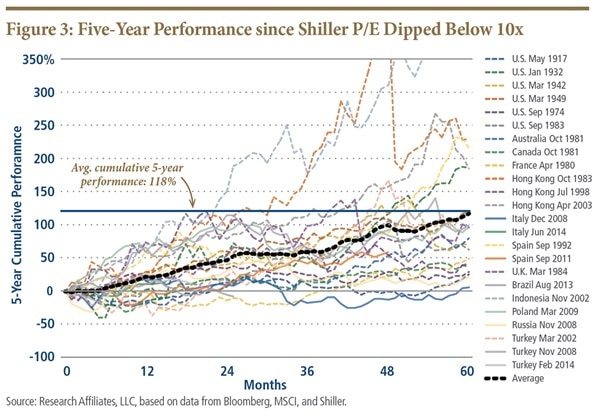

23/ We found that investing when there is blood in the streets, ie CAPE < 7 had future 5 year returns of >20%.

When investing in true bubbles, CAPE > 45, future 5 year returns were negative.

Similar chart below from @PIMCO

When investing in true bubbles, CAPE > 45, future 5 year returns were negative.

Similar chart below from @PIMCO

24/ So where are we now? Here are the CAPE ratios for some countries ending September (surely lower now!)

Russia 7

Turkey 9

Czech 10

Poland 12

Portugal 13

Spain 13

Brazil 13

For Emerging 17 (lower depending on index)

For Developed 21

US 32

Russia 7

Turkey 9

Czech 10

Poland 12

Portugal 13

Spain 13

Brazil 13

For Emerging 17 (lower depending on index)

For Developed 21

US 32

25/ So, the bad news, is the US is expensive....(2nd highest in the world.)

The good news, most of the world is normal to cheap, and emerging markets are really cheap. The cheapest bucket is screaming cheap.

The good news, most of the world is normal to cheap, and emerging markets are really cheap. The cheapest bucket is screaming cheap.

26/ So how do we take advantage of these valuation spreads?

I guarantee it’s not to jump off @twitter, call your husband/wife/clients and say “I just read this brilliant thread by this handsome fellow online, let’s go buy Russian and Turkish stocks!”

I guarantee it’s not to jump off @twitter, call your husband/wife/clients and say “I just read this brilliant thread by this handsome fellow online, let’s go buy Russian and Turkish stocks!”

27/ The problem with investing in the cheap countries is this: let’s say you do well, improve your returns a bit.

Client or spouse maybe thinks you are slightly smarter.

If you do poorly, then you’re likely fired or divorced, as what IDIOT would go and buy Russian stocks?!

Client or spouse maybe thinks you are slightly smarter.

If you do poorly, then you’re likely fired or divorced, as what IDIOT would go and buy Russian stocks?!

28/ It’s simple Career/Matrimony risk.

Which is why people like buying the expensive countries where all the economic data is great (ahem US), and avoiding the bad countries where all the economic data is usually awful, revolutions, depressions, invasions, etc.

Which is why people like buying the expensive countries where all the economic data is great (ahem US), and avoiding the bad countries where all the economic data is usually awful, revolutions, depressions, invasions, etc.

29/ One of my favorite investing quotes from friend @markYusko, “Investing is the only place where when things go on sale, everyone runs out of the store”!

30/ It’s important to invest in a basket of these countries (we do 12) and only update it once a year.

Rebalancing more actually hurts. This deep value strategy takes a looonnnggg time to play out.

Rebalancing more actually hurts. This deep value strategy takes a looonnnggg time to play out.

31/ But just as important as buying the cheap stuff is avoiding the expensive. People often miss this.

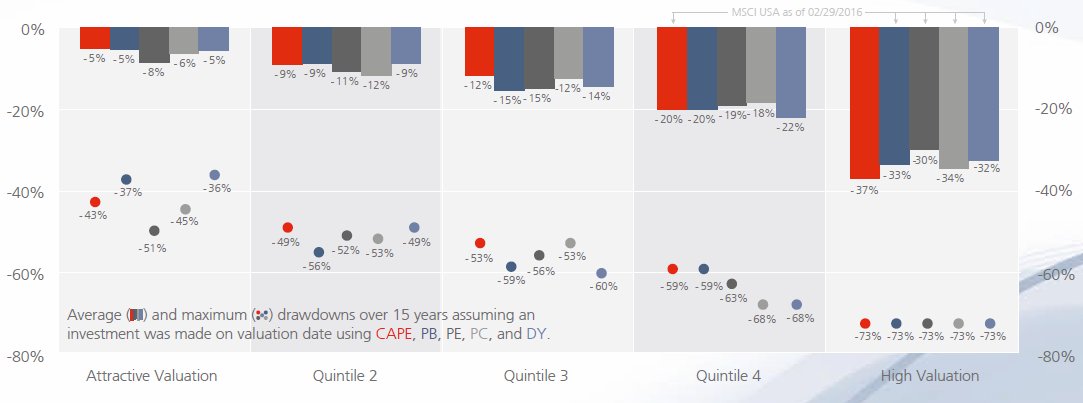

Lots of studies have shown that buying expensive markets leaves you more exposed to a big fat drawdown in the next 5 years…here's @CAPE_invest

Lots of studies have shown that buying expensive markets leaves you more exposed to a big fat drawdown in the next 5 years…here's @CAPE_invest

32/ So what is the practical take away here?

We had two good podcast discussions with Rob Arnott and @HowardMarksBook lately where they discussed the concepts of “over-rebalancing” and “calibrating” a portfolio.

mebfaber.com/podcast/

We had two good podcast discussions with Rob Arnott and @HowardMarksBook lately where they discussed the concepts of “over-rebalancing” and “calibrating” a portfolio.

mebfaber.com/podcast/

33/ You could just take our global market portfolio from Part II and replace the equity portions with some value weighted strategies.

Volatility and drawdown were roughly the same, but returns inched up a few percentage points.

The problem? You're gonna look DIFFERENT.

Volatility and drawdown were roughly the same, but returns inched up a few percentage points.

The problem? You're gonna look DIFFERENT.

34/ It's really hard for people to be too different. But to add alpha you have to be CONCENTRATED, WEIRD, and DIFFERENT.

But you also can’t pay too much. If you’re expecting alpha of 2%, but pay 2% in fees to achieve that, you are better off in market portfolio paying zero.

But you also can’t pay too much. If you’re expecting alpha of 2%, but pay 2% in fees to achieve that, you are better off in market portfolio paying zero.

35/ It's particularly important now as the spread between the US and the rest of the world are YUGE. We haven't seen spreads this wide since the 1980s, but then no one wanted US stocks!!

36/ And the cheapest bucket too....

37/ PART III Summary:

The global market portfolio is a great starting point, but tends to be suboptimal due to market cap weights. This is especially true right now as the US stock market is one of the most expensive in the world, so consider value tilts in your portfolio.

The global market portfolio is a great starting point, but tends to be suboptimal due to market cap weights. This is especially true right now as the US stock market is one of the most expensive in the world, so consider value tilts in your portfolio.

38/ PART IIII tomorrow: the hardest part in all of this.