,

476 tweets,

80 min read

Read on Twitter

In the ancient story of money a new chapter is being written… here we will explore the mysterious forces of Money, Bitcoin and Time.

This thread is breakdown of my recently published 3-part essay titled 'Money, Bitcoin and Time':

medium.com/@breedlove22/m…

Let’s go 👇🏽

This thread is breakdown of my recently published 3-part essay titled 'Money, Bitcoin and Time':

medium.com/@breedlove22/m…

Let’s go 👇🏽

1. THE SIMPLE TRUTH ABOUT MONEY: Money is the most successful story ever told by humans. It is a reflexive narrative: meaning it has value only because everyone believes it, and everyone believes it because it has value. Money is a story that continues to be written…

2. When humans began to exchange with one another, they intuitively discovered the division of labor which allows people to focus on their relative advantages and concentrate on their chosen craft. This led to the invention of better tools.

3. Tools, or technologies, are mechanisms that increase productivity by amplifying the returns on human time directed at production. You can chop more wood per man hour using an axe than you can with your bare hands.

4. As people made and exchanged more tools, time savings increased and specialization deepened. Specialization sparked innovation, because it encouraged the investment of time in tool-making tools, such as whetstones used for making sharper axes.

5. This enabled people to create superior tools, which increased productivity even further. That saved more time, which people used to specialize and trade even more, which increased the division of labor even further and so on - thereby creating a positive feedback loop:

6. Human exchange is to cultural evolution what sex is to biological evolution. By exchanging and specializing, innovations come into existence and spread. At some point, human intelligence became collective and cumulative in a way that happened to no other animal.

7. Language, and later writing, allowed us to pass our collective learnings to each successive generation. Written language allowed us to manifest and share our belief systems. Eventually, we began to organize ourselves around stories like math, nations, corporations and liberty.

8. Money is an emergent property of human exchange that solves problems inherent to trade and accelerates the rate of human exchange. Money, as the vital lubricant for human exchange, was among the first stories we used to collectively organize ourselves.

9. The simplest way for people to exchange value is to trade actual goods, say guns for boats, in a process known as direct exchange or barter. This is only practical in small groups of people where few goods are exchanged.

10. In larger groups of people, there are more opportunities for individuals to specialize in production and trade with more people, which increases the aggregate wealth for everyone.

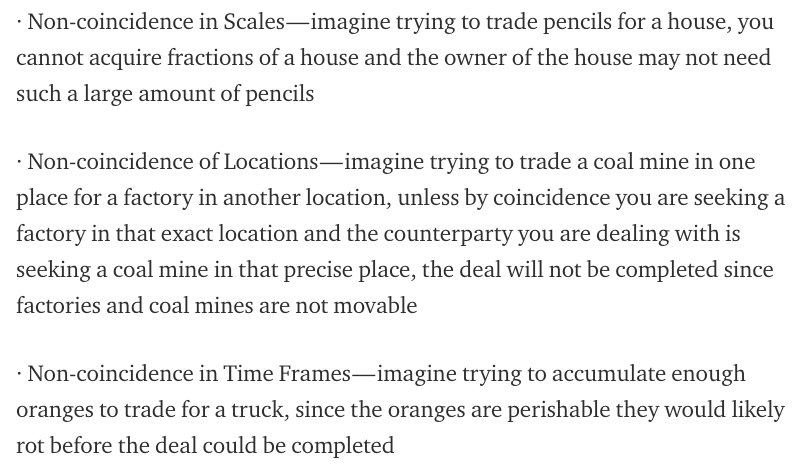

11. Larger groups of people exchanging goods mean larger markets, but also creates a problem of non-coincidence of wants – what you are seeking to acquire by trade is produced by someone who doesn’t want what you have to offer. This problem has three distinct dimensions:

12. The only way to resolve this three-dimensional problem is through indirect exchange, where you seek to find another person with a good desired by the counterparty and exchange your good for theirs only to, in turn, exchange it for the counterparty’s good to complete the deal.

13. The intermediary good used to complete the deal is called a medium of exchange - the first function of money. Over time, people gradually converge on a single medium of exchange (or, at most, a few media of exchange).

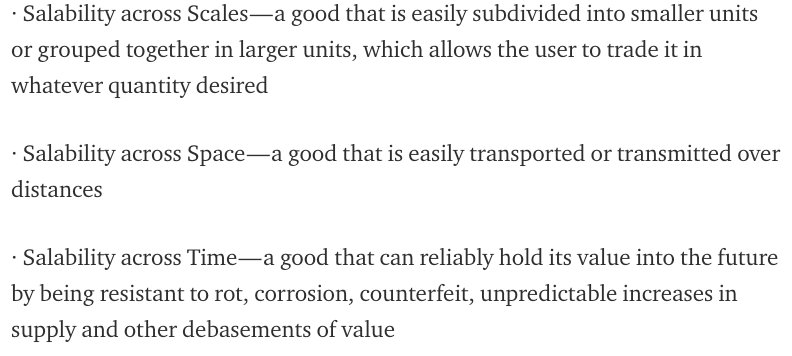

14. Money is the most liquid asset within a trade network because it provides its users maximum optionality in exchange. In this sense, money is said to have the highest salability, meaning the ease with which it can be sold on the market at any time with the least loss in price.

15. The relative salability of monetary goods can be assessed in terms of how well they address the three dimensions of the non-coincidence of wants problem:

16. The third element, salability across time, determines a good’s utility as a store of value – the second function of money. Since the production of each new unit of a monetary good makes every other unit relatively less scarce, it dilutes the value of the existing units.

17. Hard money is more trustworthy as a store of value precisely because it resists intentional debasements of its value by others and therefore maintains salability across time. The ratio which defines the hardness of a monetary good is called the stock-to-flow ratio:

18. For a good to assume a dominant monetary role in an economy, it must exhibit superior hardness with a higher stock-to-flow ratio than competing monetary goods. Particular goods become money based on the interplay of people’s decisions - let's consider money's social aspects.

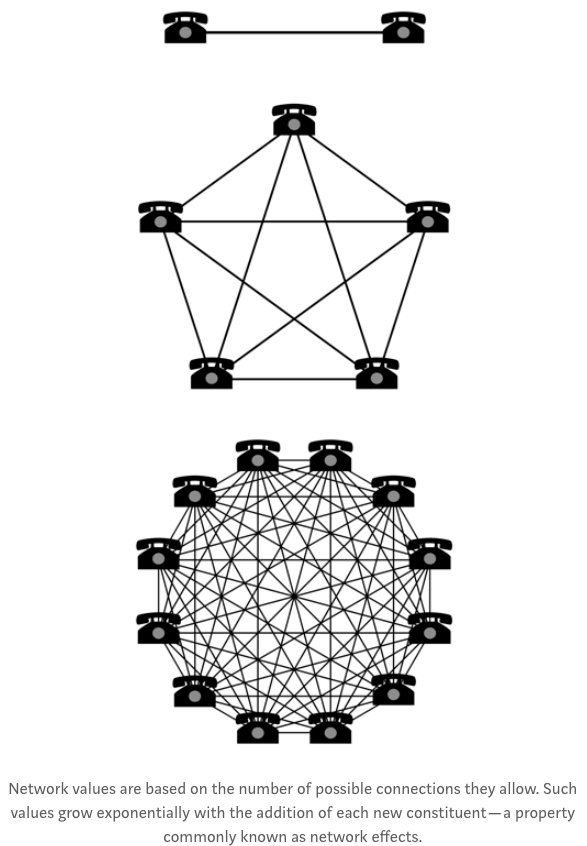

19. Money, as a value system which connects people across space and time, is the original and largest social network.

20. Similar to the telephone and modern social media platforms, a monetary network becomes exponentially more valuable as more people join it because the number of possible connections it allows is proportional to the square of the number of its total network participants:

21. In a monetary network, more possible connections mean more salability and a broader scope of trade. Participants in a monetary network are connected by their use of a common form of money to express and store value.

22. Intuitively, a monetary good that holds value across time (hard money) is always preferable to one that loses value (soft money). This causes people to naturally and rationally gravitate to the hardest form of money available to them.

23. Further, since human exchange is a singular communal phenomenon suffering from a three-dimensional non-coincidence of wants problem, any monetary good that can solve all three dimensions of this problem will win the entire (or vast majority) of the market.

24. Network effects accelerate people’s natural coalescence around a single monetary technology since larger monetary networks support higher salability of the monetary good involved.

25. As we will see, markets have naturally and spontaneously selected for the monetary good which best satisfies a variety of desirable traits that determine how useful a particular monetary good is as a form of money:

26. Hardness is the singular trait that takes primacy over all others in determining a good’s suitability for playing a monetary role as hard money provides its users peace of mind that their stored value cannot be stolen.

27. Money, as an expression of value, has remained conceptually constant but has evolved to inhabit many different goods over time.

28. Like language, which was first spoken, then written and now typed, the meaning expressed by money remains the same while its modality continually evolves. As the monetary technologies we use to express value change, so too do our preferences.

29. In economics, a critical aspect of human decision making is called time preference, which is the ratio at which an individual values the present relative to the future. Time preference is positive for all humans, as the future is uncertain, and the end could always be near.

30. Therefore, all else being equal, we naturally prefer to receive value sooner rather than later. People who prefer to defer current consumption and instead invest for the future are said to have a lower time preference.

31. The lowering of time preference is closely related to the hardness of money and is also exactly what enables human civilization to advance and become more prosperous. In regard to time preference, hard money is important in three critical aspects:

32. Only humans with a lower time preference can decide to forgo a few hours of fishing and opt to build a superior fishing pole, which cannot be eaten itself, but in the future will enable better results (in both quality and quantity) per hour of human effort spent fishing.

33. Investments in the future, like building a fishing pole, create compounding effects which allow further investment. In this way, investment increases capital good stocks which increases productivity. Amazingly, this effect also transforms into a positive feedback loop:

34. From this perspective, it becomes clear that the most important economic decisions any individual faces are related to the trade-offs they face with their future self. Eat less fish today, build a fishing boat tomorrow. Read today, have knowledge tomorrow. etc...

35. These individual relationships with our future selves is the microcosm of the societal macrocosm. As society develops a lower time preference, its prospects of prosperity improve in tandem.

36. As we have seen, hard money is superior at holding its value across time. Since its purchasing power tends to remain constant or grow over time, hard money incentivizes people to delay consumption and invest for the future, thereby lowering their time preference.

37. Paradoxically, a world that consistently defers consumption will actually end up consuming more in the long run as its increased savings would increase investment and productivity, thus making its citizenry wealthier in the future:

38. As we will show later, when the gold standard was forcibly ended by governments, money not only became much softer, but it also fell under the command of politicians who are incentivized to operate with high time preferences as they strive for reelection every few years.

39. This is why politicians continue to mandate the use of soft government money, despite the long-term harm it causes to an economy, ensuring that it remains the dominant form of money in the world (we will see soft government money’s unnatural ascent to world domination later).

40. When a form of money becomes globally dominant, it finally serves the third function of money – unit of account. History shows us that this function is the final evolutionary stage in the natural ascendancy of monetary goods that achieve a dominant role. As Jevons explains:

41. Today, the US Dollar is dominant and serves as the global unit of account as prices are most commonly expressed in its terms. This consistency of expression simplifies trade and enables a (somewhat) stable pricing structure for the global economy.

42. Prices are an essential communicative force in economics. As economic production moves from a primitive scale, it becomes harder for individuals to make decisions without having a fixed unit of account with which to compare the value of different objects to one another.

43. Price signals are the coordinating force of free market systems. Each individual decision maker can faithfully rely on the prices of goods relevant to their production process, as the prices themselves are a distillation of all known market realities into a single variable.

44. Each individual’s buy and sell decisions, in turn, further shape prices which carry this altered information back out into the market. Price signals are to market participants what light is to the eye.

45. The wisdom of the crowd is always superior to the wisdom of the board room. There is simply no way to recreate the adaptivity and collective intelligence of markets by installing a centralized planning authority.

46. How would they decide who should increase production and by how much? How would they decide who should reduce consumption and by how much? How would they coordinate and enforce their decisions in real time on a global scale?

47. In this sense, prices are the economic nervous system that disseminate knowledge across the world and help coordinate complex production processes. Without accurate price signals, humans could not benefit from the division of labor and specialization beyond a small scale.

48. Specialization, guided by reliable price signals, enables producers to improve their efficiency of production and accumulate capital specific to their craft. The most productive allocation of human efforts is only determinable by an accurate pricing system in a free market.

49. Also (as we will see later), this is exactly why capitalism prevailed over socialism, because socialism lacked an economic nervous system.

50. But before diving into the economic aspects which underpinned this historic ideological struggle and seeing how it is still relevant today, we first need to understand the evolutionary forces that have shaped money throughout history.

51. Throughout history, money has taken many forms - seashells, salt, cattle, beads, stones, precious metals and government paper have all functioned as money at one or more points in history.

52. Different monetary technologies are in constant competition, like animals competing within an ecosystem. Although instead of competing for food and mates like animals, monetary goods compete for the belief and trust of people.

53. Believability and trustworthiness form the basis of social consensus – the source of a particular monetary good’s sovereignty from which it derives its market value along with the trust factors and permissions necessary to transact with it.

54. Free market competition is ruthlessly effective at promulgating hard money as it only allows those who choose the hardest form available to maintain wealth over time.

55. This market-driven natural selection causes new forms of money to come into existence and older forms to fade into extinction.

56. Like biologically-driven natural selection, in which nature continuously favors the organisms which are best suited for success in their respective ecologies…

57... this market-driven natural selection is a process in which people naturally and rationally favor the most believable and trustworthy monetary technologies available in their respective trade networks.

58. There are many examples of market-driven natural selection favoring the hardest form of money, including West Africans using aggry beads in the 16th century and the failure of the silver standard going into the 19th century.

59. Let’s consider the ancient Rai Stone monetary system of Yap Island:

59a. Rai Stones were large disks of various sizes with a hole in the middle that weighed up to eight thousand pounds each.

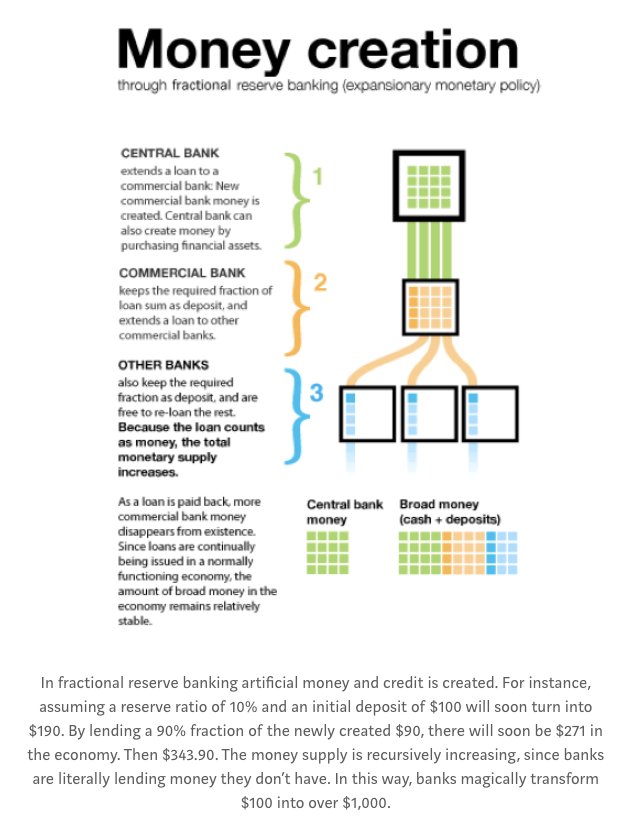

59b. Acquiring these stones involved a labor-intensive process of quarrying and shipping. Procuring the largest Rai Stones required workforces numbering in the hundreds. (Such skin in the game is necessary for hard money systems to function properly).

59c. Once the stones arrived in Yap, they were placed in a prominent location where everyone could see them. Owners of the stones could then use them as payment by announcing to the townsfolk the transfer of ownership to a new recipient (similar to Bitcoin's distributed ledger).

59d. Rai Stones solved the three dimensions of the non-coincidence of wants problem for the Yapese by providing:

59e. This monetary system worked well until 1871, when an Irish-American captain named David O’Keefe began using superior tools, boats and explosives to procure Rai Stones with relative ease.

59f. Other opportunists followed and soon the flow of Rai Stones increased dramatically. By using modern technologies to acquire Rai Stones more cheaply, foreigners were able to compromise the hardness of this ancient monetary good.

59g. The market naturally selected against Rai Stones because, as their stock-to-flow ratio declined, they became less reliable as a store of value and thus lost their salability across time, which ultimately led to the extinction of this ancient monetary system.

60. Eventually and unsurprisingly, gold - with the highest stock-to-flow ratio of any monetary metal - was naturally selected for by the market due its superior hardness. Gold was complemented by silver for its lower value to weight ratio and thus higher salability across scales.

61. Metal coinage became the world's first standardized hard money system:

62. The drawback of gold was its physicality, which reduced its salability across scales and space. Banks intervened to enhanced gold’s salability across scales and space by taking custody of physical gold and issuing gold-backed bank notes and checks:

63. With all of the critical salability characteristics gathered under a gold standard monetary system, it flourished globally and outcompeted silver and other softer monetary technologies on its way to becoming globally dominant.

64. With the highest stock-to-flow ratio of all the monetary metals, gold is the hardest physical form of money that has ever existed, which explains its success as hard money throughout history.

65. Even with advances in mining techniques, gold still has a relatively low and predictable flow, as evidenced by its annual supply growth since 1970:

66. In the 19th century, the term cash referred to central bank gold reserves, which was the dominant self-sovereign monetary good at the time. Cash settlement referred the transfer of physical gold between central banks to execute final settlement.

67. In this way, physical gold is considered to be cash money, meaning that it is a self-sovereign asset under the full control of its possessor and does not result from the liability of anyone else.

68. Central banks can only settle with finality in physical gold, and still do so periodically in the modern era, since it is the only form of money that requires no trust in any counterparty, is politically neutral and gives its holders full sovereignty over their money.

69. By the end of the 19th century, the network effects of the gold standard had taken hold, encouraging most of the industrialized nations of the world to officially adopt the gold standard.

70. By virtue of operating on a hard money basis, most of the world witnessed unprecedented levels of capital accumulation, free global trade, restrained government and improving living standards. The French called this period La Belle Époque:

71. Incapable of resisting the temptation of wealth expropriation by tampering with the money supply, banks soon began issuing more notes than their gold reserves could justify, thus initiating the practice of fractional reserve banking.

72. This banking model facilitated the creation of money without any skin in the game (the softest form of money possible) and enabled the money multiplier effect which, contrary to its name, is a terrible thing:

73. As 20th century wars raged, so did the printing presses. Governments and their central banks continued to grow more powerful with each new bank note printed as their citizens grew poorer.

74. Due to a unilateral decision of President Nixon in United States, governments finally severed the peg to gold entirely in 1971. Which brings us to the modern form of dominant money: government fiat money.

75. Fiat is a Latin word meaning decree, order or authorization. This is why government money is commonly referred to as fiat money, since its value exists solely because of government decree.

76. This is an imperative point: it was possession of gold (self-sovereign, hard money) that gave governments the power to decree the value of their fiat money (soft money) in the first place.

76a. Governments were only able to achieve “sovereignty” because they drew this power from their possession of gold. Paradoxically, people were coerced into discarding the gold standard and adopting soft government fiat money only because of their belief in gold as a hard money:

76b. This is proof that it is possible to create a synthetic asset and endow it with monetary properties, whether by decree or by market-driven natural selection. Governments did so by stealing gold from citizens, thus empowering them to create fiat money and decree its value.

76c. As we will later see, Satoshi Nakamoto did so by creating Bitcoin and releasing it into the marketplace as a self-sovereign money free to compete for the trust and belief of the people based on its own merits.

77. Unlike to the flow restrictions associated with gold mining, there are practically no economic restraints preventing a government from printing more fiat money (no skin in the game).

78. As is to be expected, soft government money has an abysmal track record as a store of value. This becomes abundantly clear when we look at its inflationary effects on the price of gold.

79. An ounce of gold in 1971 was worth $35 USD, and today is worth over $1,200 USD (a decrease of over 97% in the value of each dollar due entirely to inflation). Worse still, inflation is the primary driver of economic inequality in the world.

79a. The constantly increasing supply of government money means its currency depreciates continuously, as wealth is stolen from the holders of the currency (or assets denominated in it) and transferred to those who print the currency or receive it earliest.

79b. This transfer of wealth is known as the Cantillon Effect: the primary beneficiaries from expansionary monetary policy are the first recipients of the new money, who are able to spend it before it has entered wider circulation and caused prices to rise.

79c. Generally, this is why inflation hurts the poorest and helps the bankers, who are closest to the spigot of liquidity (the government fiat money printing press) in the modern economy (h/t @APompliano).

80. A centrally planned market for money like this completely contradicts the principles of free market capitalism. In a socialist system, the government owns and controls all means of production.

81. This ultimately makes the government the sole buyer and seller of all capital goods in its economy. Such centralization stifles market functions, like price signals, and makes decision making highly ineffective.

82. The point here is not to trumpet free market capitalism over socialism, but rather to clearly explicate the difference between the two ways of allocating resources and making production decisions:

83. A free market is one in which buyers and sellers are free to transact on terms determined solely by them, where entry and exit into the market are free and no third parties can restrict or subsidize any market participants.

84. Most countries have (relatively) free markets. But no country in the world today has a free market for money, which is the most important market in any economy.

85. In a free market for money, the exact amount of savings equals the exact amount of loanable funds available to borrowers for the production of capital goods.

86. In the free market for money, the opportunity cost of saving is foregone consumption, and the opportunity cost of consumption is foregone saving – an indisputable economic reality that cannot be changed with central planning.

87. Most often, central banks are trying to spur economic growth and consumption, so they will increase the supply of loanable funds and lower the interest rate (the “price” of money):

88. With the price of loanable funds (the interest rate) artificially suppressed, producers take on more debt to start projects than there are savings to finance these projects.

89. These artificially low interest rates don’t provide any benefit to the economy, rather they simply disseminate distorted price signals that encourage producers to embark on projects which cannot realistically be financed from actual savings.

90. This creates a market distortion (in other words, blows up another bubble) in which the value of consumption deferred is less than the value of the savings borrowed.

91. The excess supply of loanable funds, backed by no actual deferred consumption, initially encourages producers to borrow as they believe the funds will allow them to buy all the capital goods necessary for their project to succeed.

92. As more producers borrow and bid for the same amount of capital goods, inflation sets in and prices begin to rise. At this point, the market manipulation is exposed since the projects become unprofitable after the rise in capital good prices and suddenly begin to fail.

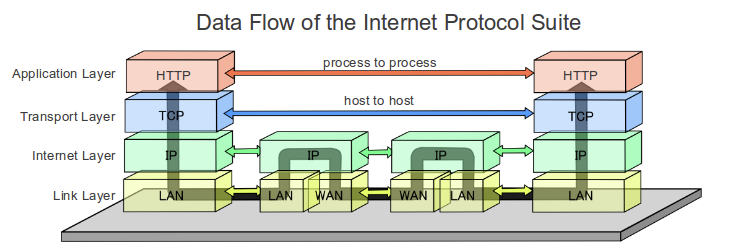

93. An economy-wide simultaneous failure of overextended projects like this is called a recession. The boom and bust business cycle we have all grown accustomed to in the modern economy is an inevitable consequence of this centrally planned market manipulation.

94. Only central planning of a soft money supply and its pricing mechanism can cause widespread failures in an economy like this, as an economy based on hard money remains firmly rooted in economic reality and resists market distortions.

94a. The United States and Europe saw a great illustration of this process when the dot-com bubble of the late 1990s was replaced by the housing bubble of the mid-2000s.

95. As with all well-functioning markets, the price of money must emerge through the natural interactions of supply and demand. Healthy markets require functional nervous systems, as market participants must have accurate price signals to make decisions effectively.

96. Free market capitalism cannot function without a free market for money. Alignment with natural market forces like supply, demand and the price signal is the principal reason free market capitalism prevailed over socialism.

97. This severe inadequacy of the socialistic central banking model and government fiat money came to the forefront of global consciousness in the wake of the Great Recession that began in 2008.

98. Due to gigantic market distortions driven by artificially low interest rates and credit ratings agencies with no skin in the game, US subprime real estate became the largest bubble in modern history.

99. When it finally bursts, its affects were globally systemic, and central banks all over the world (predictably) began increasing their money supplies in an attempt to reflate their broken economies:

100. It was in the depths of the Great Recession that an anonymous individual named Satoshi Nakamoto introduced the open-source software project called Bitcoin to an online group of cryptographers.

101. After ten years of virtually perfect operation, the Bitcoin network has gone from $0 to $80B in value stored on its network and has cleared $1.38T in total transactions.

102. It is clear that Bitcoin, as a monetary technology, is now competing successfully in the marketplace and is being used by many for real world purposes.

103. THE SIMPLE TRUTH ABOUT BITCOIN: Bitcoin is the hardest form of money ever invented. It has successfully brought the advantages of physical cash money into the digital realm. The next chapter in the story of money is being written in a new language…

104. Bitcoin seems easy to understand at first (it’s just magic internet money, right?), however truly grasping its significance is a formidable task. Once you think you have Bitcoin figured out, you’ll see it from another perspective and realize how little you actually knew.

105. Bitcoin has been called many things – digital gold, tulip mania 2.0, financial revolution, the MySpace of cryptocurrencies, environmental disaster, rat poison squared, apex predator of monetary technologies, the model-T of cryptocurrencies and a superior species of money.

106. But it turns out that, in context of the history and nature of money, Bitcoin appears to be a distinct evolutionary leap forward.

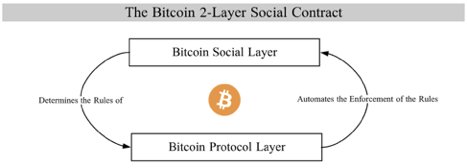

107. Bitcoin is not an internet application like MySpace, it is an internet protocol. Bitcoin is not the model-T of cryptocurrencies, it is a more like a global freeway system. Bitcoin is not like any type of gold coin, Bitcoin is more like the element gold.

108. This may sound mind blowing at first. Most innovations of this magnitude sound this way in the beginning as we struggle to communicate using outdated terms and analogies that cannot possibly convey their importance.

109. In light of its inherent complexity and novelty, we will view Bitcoin from many different perspectives in an attempt to create a mosaic of understanding in the minds of our readers. First and foremost, Bitcoin is digital cash money.

110. Bitcoin is the first truly digital solution to the problem of money. It is the world’s first digital cash (in the original sense of the word cash discussed earlier) meaning that it is under the full control of its owner and can be used for final settlement (like gold).

110a. Put another way, Bitcoin is digital cash money, a self-sovereign asset that contains within it all the trust factors and permissions necessary to transact with it. Bitcoin is not the liability of any counterparty, hence its nickname – digital gold.

110b. Like gold, Bitcoin is a supranational form of money, meaning that no government needs to decree its value or permit its use, nor can it be eliminated unilaterally by regulation (more on regulation later).

111. As one perspective of its monetary significance, Bitcoin can be understood as the successful fusion of the advantages associated with physical cash payments with the efficiencies and certainties enabled by digital technology.

111a. Cash payments have the advantage of being immediate, final and requiring no trust on the part of either transacting party in each other or any other intermediary.

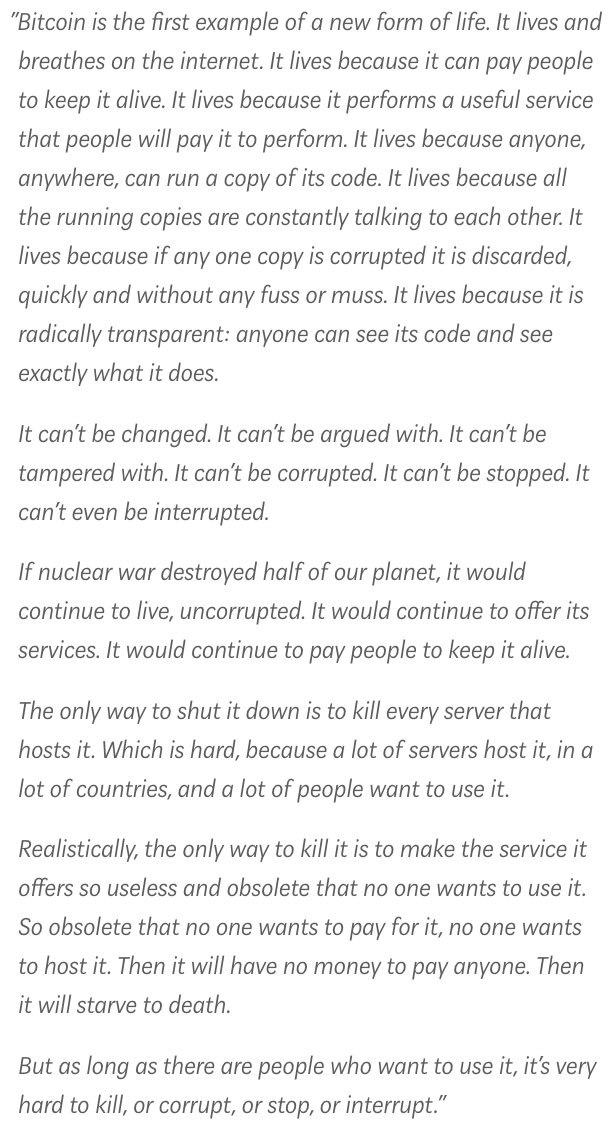

111b. The drawback of cash payments was the need for transacting parties to be physically present in the same space and time, which increases risks associated with physical custody, especially for larger transactions.

111c. As more business is conducted remotely, thanks to ever-advancing telecommunications technologies like the internet, physical cash transactions become increasingly impractical.

111d. Since the inception of computers, the nature of all digital objects is that they were infinitely replicable. This meant that no digital object could be provably limited in quantity.

111e. For instance, when you “send” and email, you are actually sending a copy, as you still have the email in your sent folder. Before Bitcoin, there was no way to send a digital good that could not also be resent elsewhere at a later time.

111f. This presented an intractable issue for direct digital payments known as the double-spend problem. Without a trusted third-party intermediary to verify the payer was not double spending, digital payments were not possible.

111g. The nature of digital objects also meant creating a digital cash was impossible, since its monetary units could be reproduced endlessly and would therefore suffer from unlimited inflation.

111h. Before Bitcoin, people had to rely on physical laws (rarity and chemistry, in the case of gold) or jurisdictional laws (government and central bank monopolies) to regulate money supplies.

111i. Nakamoto successfully made Bitcoins the first digital objects that were verifiably scarce. As the world’s first instance of digital scarcity, Bitcoin was able to solve the double-spend problem and become the world’s first functional digital cash money.

112. Here we will focus on Bitcoin’s monetary properties and its relevance in the story of money. However, some basic technical knowledge of Bitcoin is warranted to fully appreciate the importance of the innovation that is digital cash money.

112a. Bitcoin is open-source software, meaning its source code can be inspected by anyone. This makes Bitcoin a language, its source code and transaction history are universally transparent and can even be printed onto paper.

112b. To become a Bitcoin network member, known as a node, all that is necessary is to download and run the software on a computer.

112c. By becoming a node, the entire Bitcoin transaction history will be recorded on your machine and updated in perpetuity, just as it is on every other node in the world. This is the essence of Bitcoin’s decentralized architecture.

112d. The Bitcoin network, similar to the internet, lives everywhere and nowhere. Everywhere meaning on every machine, and nowhere meaning no centralized point to attack or shutdown.

112e. Every transaction has to be recorded by every node on the network so that they all share one common ledger of balances and transactions (remarkably similar to the Rai Stone system used by the Yap Islanders).

112f. Transactions are grouped together approximately every ten minutes in what is known as a block. Each block is then added to the previous block of transactions, forming a chronological chain of inextricably linked blocks that stretches all the way back to the Genesis Block.

112g. This is commonly called the Bitcoin blockchain. The blockchain is the common ledger of which each node maintains its own copy (commonly known as the distributed ledger).

112h. Each node verifies the accuracy of every other node’s transaction inputs and truth is established by consensus. In this way, the Bitcoin network relies 100% on verification and 0% on trust.

113. Economic incentives and disincentives are used to maintain truthful records in the blockchain, it what is an ingenious application of the skin in the game concept (h/t @nntaleb). Nodes compete to solve complex mathematical puzzles in a process called proof-of-work.

113a. Nodes are incentivized to perform this computing task because the first one to solve the proof-of-work is awarded a batch of newly issued Bitcoin and the transaction fees generated within the latest block of transactions – called the block reward.

113b. Nodes expend processing power (in the form of electricity) to solve these complicated mathematical problems, although considerably less and much more efficiently than the systems that support gold and government money today:

113d. Proof-of-work energy expenditure is the thermodynamic bridge from the physical to the digital world. It transmutes the fundamental commodity of the universe, energy, into digital gold (h/t @danheld).

113e. This energy expenditure is essential to the functioning of the Bitcoin network, as it disincentivizes node dishonesty.

113f. If a node attempted to include a fraudulent transaction in a block, other nodes would reject it and it would incur the cost of processing power without the prospect of earning the block reward.

113g. As we have learned, the costs and risks related to the mining of this monetary metal is necessary for it to maintain its hardness (skin in the game). Similarly, mining using proof-of-work is the only known method of creating digital cash money.

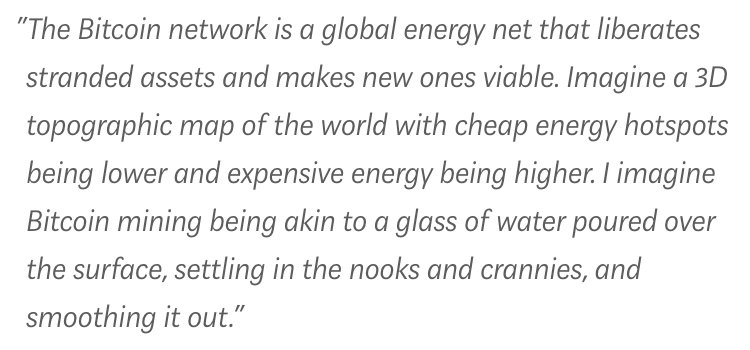

113h. The Bitcoin network provides a perpetual economic incentive for everyone in the world to invent more efficient methods of harnessing energy. This global incentive will increase the rate of innovation in energy technologies. As Bitcoin expert @nic__carter puts it:

114. As more nodes compete to solve the proof-of-work puzzle, the difficulty automatically increases so that new blocks are added on average once every ten minutes.

115. This automatic algorithmic change is called the difficulty adjustment and is perhaps the most ingenious aspect of Bitcoin.

115a. As we have seen, when a form of money appreciates, people are immediately incentivized to increase its new supply flow, which reduces its stock-to-flow ratio and compromises its hardness.

115b. With Bitcoin, an increase in its price does not lead to the production of more Bitcoin beyond its transparent and predictable supply schedule.

115c. Instead, it simply leads to an increase in processing power committed by miners which in turn makes the network more secure and difficult to compromise.

115d. Like a vault that becomes harder to crack the more money that is stored within it, Bitcoin offers people an incredibly effective means of value storage. Here, we depict the entire process of a Bitcoin transaction:

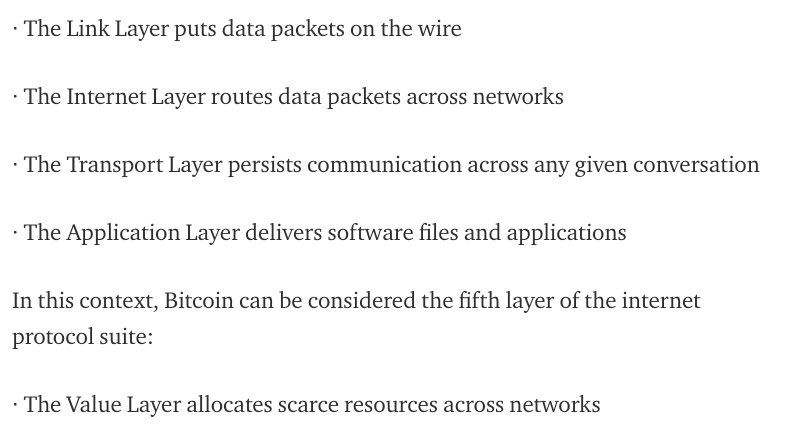

116. “The internet of value” is a popular moniker to describe Bitcoin. In reality, the Bitcoin protocol can be considered an integral and newly evolved layer of the commercial internet (h/t @naval):

116a. In the same way the internet is a set of open-source protocols for exchanging data, Bitcoin is an open-source protocol for exchanging value. It is also trustless, as any machine can accept it from any other securely and at virtually zero cost.

116b. Bitcoin is also global and permissionless, meaning that any machine can speak its language and no central bank is required to authorize its use. You can think of spoken languages as being permissionless as well, as anyone is free to learn and use them.

116c. In the same way that money is an emergent property of complex human interactions, Bitcoin is an emergent property of complex interactions occurring between people, machines and markets.

116d. Even if Nakamoto and Bitcoin never existed, it would still be necessary for us to invent the concept of cryptoassets to enable machines to exchange value to facilitate digital economies, use smart contracts and provide the substrate necessary for the ‘internet of things’.

117. Bitcoin is the hardest form of money ever invented. Its money supply is enforced mathematically and, like the other rules of Bitcoin, cannot be broken or changed. Only 21 million Bitcoins can and will ever exist.

118. This strictly limited supply makes it the first monetary technology exhibiting absolute scarcity. Before Bitcoin, only time itself had achieved the property of absolute scarcity.

119. Since increased demand for Bitcoin cannot affect its supply, it can only be expressed in its price. Bitcoin has perfect price inelasticity of supply, meaning that it has zero supply-side response to increases in its price.

120. Unlike gold and all other physical commodities, where an increase in demand will inevitably lead to larger supplies being produced over time, Bitcoin can only express an increase in demand by becoming more expensive (and a more secure network).

121. With a totally inflexible supply schedule, as long as Bitcoin is growing quickly, its price will behave like that of a startup company stock undergoing meteoric growth.

122. Should Bitcoin achieve sufficient market penetration that its growth slows down, it would become a stable monetary asset expected to appreciate slightly each year as demand increases due to productivity and population growth – like any mature hard money should.

122a. As expected, over the long-run we are already seeing a decrease in Bitcoin’s price volatility:

123. Bitcoin’s immutable monetary policy ensures that its supply will continue to grow at a decreasing rate and will reach its maximum of 21 million units sometime in the year 2140:

123a. Once the last Bitcoin is mined, its stock-to-flow ratio will become infinite as its flow will completely and irreversibly cease. Bitcoin will inevitably become the world's first monetary good with hardness reaching infinity.

123b. Bitcoin’s decreasing growth rate means that the first 20 million coins will be mined by the year 2025, leaving the last 1 million to be mined over the subsequent 115 years:

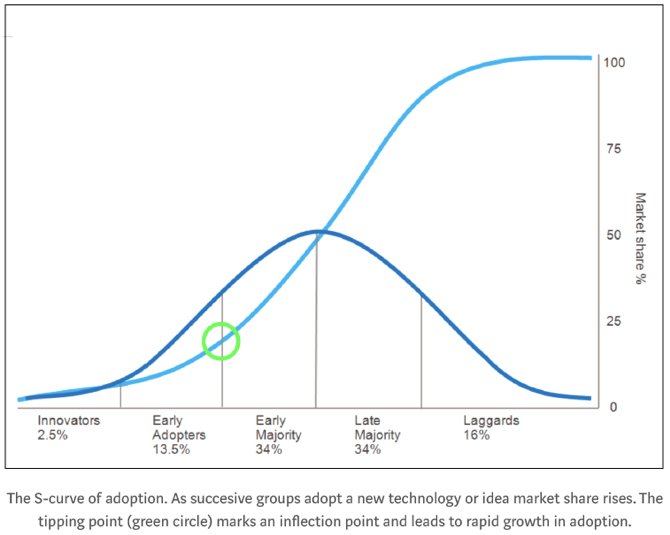

123c. With an immutable dis-inflationary (and ultimately deflationary) monetary policy, Bitcoin is uninflatable money in a world where wealth is continuously stolen via inflation.

123d. As is the case with its other immutable laws, Bitcoin’s monetary policy is enforced by the inviolable laws of mathematics. Inevitably, Bitcoin will surpass gold around the year 2020 to become the hardest form of money in history:

124. The informational nature of Bitcoin makes it highly resistant to centralization and confiscation which, unlike the gold standard, protects it from being compromised as a hard money system.

125. Throughout history, moving a society away from a hard money system has been a harbinger of economic crisis and societal decay, an outcome that can be explained as a social contract rescission (h/t @hasufl).

126. Social contract theory starts with an assumed hypothetical state of nature full of violence that is unbearable for people to live in.

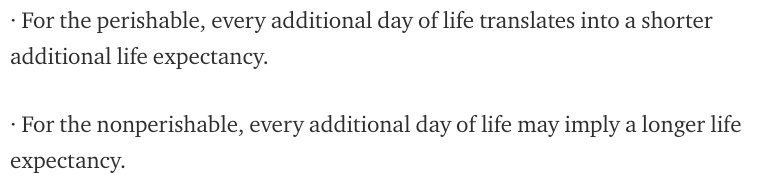

126a. Driven by a desire to improve their circumstances, people come together and collectively agree to sacrifice some of their freedoms to establish a social contract and empower an institution to protect them.

126b. Government is the result of a social contract: people sacrifice some of their freedoms to give the state control over the monetary system and armed forces. The state, in turn, uses that power to manage the economy, redistribute wealth and fight crime.

126c. In the United States, our current social contract grants the government monopoly control of money (via the Federal Reserve) and violence (via the Police and Military).

127. Similarly, money itself can be thought of as a social contract. If enough people are unhappy with a barter economy, they can collectively agree to use money instead.

127a. This social contract entails sacrificing certainty (requiring trust that dollars will maintain their value over time) in exchange for convenience (using dollars as a medium of exchange).

127b. The social contract for money, as we have seen, emerges and evolves spontaneously based on market-driven natural selection. New social contracts centered on particular monetary goods - such as seashells, salt or gold - rise and fall with the tides of history.

127c. Each person continuously decides which outcomes they prefer and how best to achieve them. If enough people seek the same outcome, we call the result a social contract.

128. The invention of Bitcoin can be regarded as a new implementation of the social contract for money. Nakamoto settled on the following rules for this new implementation:

129. Historically, social contracts intended to protect people, such as governments and their central banks, eventually became controlling and or turned abusive. When a social contract loses sufficient trust of the people, it falls apart or is overthrown, by ballot or by bullet.

130. This dynamic has resulted in a continuous cycle of rising and falling social contracts throughout history. Bitcoin is intended to break this cycle in two ways:

130a. Instead of seeking security from a powerful central entity that can be corrupted or overthrown, Bitcoin creates a hyper-competitive market for its own protection. It turns security into a commodity and the security providers (miners) into harmless commodity producers.

130b. By requiring its security market participants (miners) to incur real world costs to generate their economic reward (skin in the game), Bitcoin incentivizes the market to reach consensus over who owns what at any given point in time.

131. As a monetary social contract and technology, the Bitcoin social contract is composed of two distinct, self-reinforcing layers: the social layer and the protocol layer. (h/t @hasufl)

132. The social layer is the social consensus itself, which determines the rules of Bitcoin and establishes its value. The protocol layer simply automates the enforcement of the rules set by the social layer:

133. In this sense, Bitcoin is more than just a technology. Indeed, it is a new institutional form. Viewing it in this way, we are better able to answer some of the more existential questions about Bitcoin. First, who can change the rules of Bitcoin?

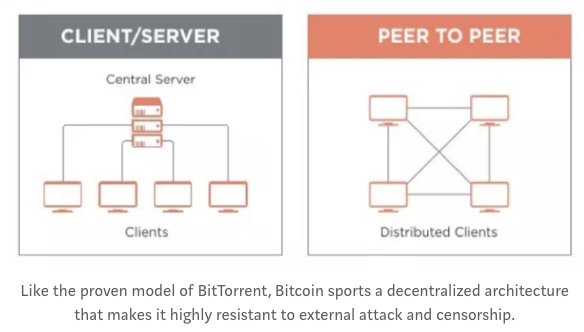

133a. The only way to change the rules of the Bitcoin social contract is to convince people to voluntarily accept your proposed rule changes at the social layer. As each network member is self-interested, they will only adopt rules that benefit them.

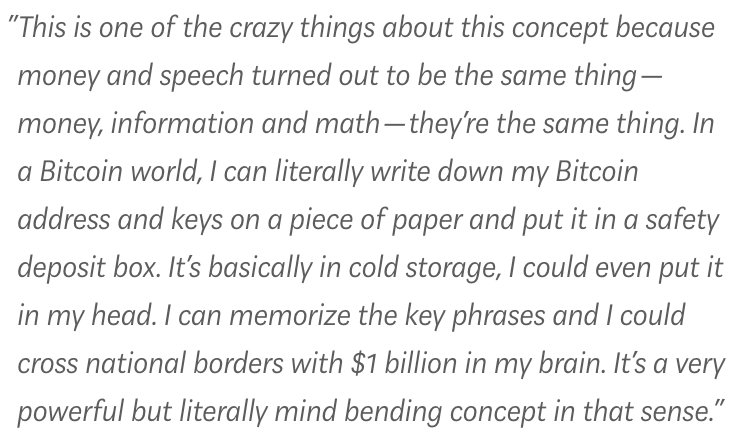

133b. Seeing as its current rules are already optimal for Bitcoin holders (resistance to confiscation, censorship, inflation and counterfeit) it would be extremely difficult to convince a majority of the approximately 30 million network participants to change rulesets.

133c. This asymmetrical governance dynamic, between the cost of campaigning for change and the limited design space left by Nakamoto to further benefit Bitcoin holders, virtually rules out any contentious changes from succeeding as they would never get broad social consensus.

133d. Therefore, the Bitcoin network can be upgraded in ways that align with the collective best interests of its members and is at the same time highly resilient to changes that contradict these interests.

134. Next Question: Can a Software Bug Kill Bitcoin?

134a. In September 2018, a software bug arose in the main implementation of Bitcoin that opened up two potential attack vectors which theoretically could have been exploited to circumvent its counterfeit and inflation resistance properties.

134b. Bitcoin developers quickly fixed the bug before either vector was exploited, however this event left many people wondering what would have happened had the vulnerabilities not been discovered in time.

134c. Had the software bug not been discovered in time, Bitcoin’s blockchain would have undergone a fork – meaning its protocol layer would have been split it into two networks, one with the bug and one without it.

134d. At the social layer, each Bitcoin owner would then choose either the implementation with or without the bug.

134e. To protect the value of their Bitcoin, holders would rationally choose to migrate to the mended network and its blockchain would continue without interruption.

135. Last Question: Can Forks Compromise the Immutability of Bitcoin’s Rules?

135a. Since Bitcoin is open-source software, anyone in the world can copy its code, change it and launch their own version. This is also a chain fork which, as established earlier, affects only the protocol layer of the Bitcoin social contract.

135b. To successfully change the rules of Bitcoin, you must successfully fork its social layer first. Forks like these are difficult to pull off in reality because they require buy-in from thousands of people to be successful.

135c. This asymmetry between the cost of campaigning for ruleset changes and their potential benefit to network participants makes the Bitcoin network exhibit an extremely strong status quo bias when it comes to governance.

135d. Forking Bitcoin’s protocol layer is worthless without forking the social layer from which it derives its rules and market value.

135e. In the rare cases that the social layer itself splits, as was the case with the Bitcoin Cash fork, the result is two weaker social contracts, each agreed upon by fewer people than before.

135f. The failure of the Bitcoin Cash fork (its price has declined from 0.21 to 0.04 Bitcoin over the past year) is yet another battle scar for Bitcoin that pays testament to its governance model and exemplifies the winner take all dynamics inherent to monetary competition.

136. In essence, by believing that mathematics and individual self-interest will persist, we can reliably believe in Bitcoin’s value proposition and its ongoing successful operation.

137. Over the past 10 years, by inventively aligning human self-interest with its own self-interest, the Bitcoin network has managed to grow organically from $0 to $80B in value.

138. Although Bitcoin is intended to be a monetary technology, it is a totally unique compared to other forms of money. Ralph Merkle, famous cryptographer and inventor of the Merkle tree data structure, has a remarkable way of describing Bitcoin:

139. Bitcoin is a technology, like the hammer or the wheel, that survives for the same reason any other technology survives: it provides benefits to those who use it. As a living structure, the Bitcoin network reflects a quintessential manifestation commonly found in nature.

140. The Bitcoin network mirrors one of the most successful evolutionary structures found in nature, the decentralized network archetype (h/t @bquittem):

141. A decentralized form in organic systems confers advantages such as distributed intelligence, invulnerability to singular attack vectors and accelerated adaptivity.

141a. In most forms of life, genes are only passed from parent to offspring in a process called vertical gene transfer.

141b. Certain fungal networks, which are modeled after the decentralized network archetype, are able to steal competitive advantages directly from physical contact with other similar organisms in a process called horizontal gene transfer.

141c. Such organisms exhibit distributed intelligence, meaning they learn at the edges and distribute the lessons throughout their vast networks.

141d. There is a common misconception that an alternative cryptoasset could develop a superior feature that will eventually outcompete Bitcoin.

141e. Similar to certain fungal networks, Bitcoin is able to subsume features that have been proven on the competitive terrain (in the marketplace) from cryptoasset competitors.

141f. For instance, by using the Lightning Joule browser extension and running a full Bitcoin node, you can perform browser-based microtransactions similar to BAT but using Bitcoin instead. This effectively eliminates the need for a cryptoasset like BAT:

141g. This ability accelerates the adaptivity of the Bitcoin network and insulates it from competitive disruption which further reinforces its position as the dominant species of money (the market leader).

141h. The decentralized network archetype found in nature is the antecedent to paradigm shifting innovations throughout history such as the railroad system, the telegraph, the telephone, the power distribution grid, the internet, social media and now Bitcoin.

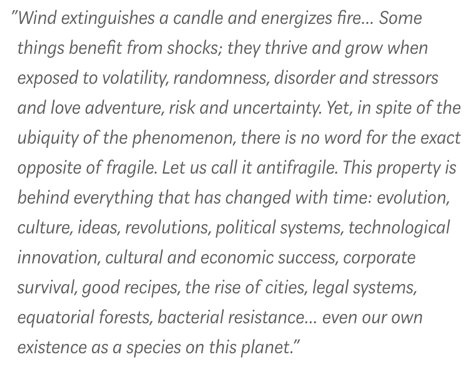

142. An open and decentralized nature also enables Bitcoin to benefit from adversity. In light of its track record, Bitcoin is an excellent incarnation of Nassim Taleb’s concept of Antifragility (h/t @nntaleb):

142a. Fragility can be defined as sensitivity to disorder, whereas robustness is insensitivity to disorder. Antifragility is a property of anything that benefits from disorder, stress or adversity. Since the resiliency of Bitcoin is hardened by hostility, it is antifragile.

142b. The many failed attempts at killing Bitcoin thus far have only made it stronger by drawing attention to attack vectors or vulnerabilities that its global team of self-interested, volunteer programmers can then fix.

142c. These improvements have only increased the network’s operational efficiency. Also, each time it withstands an external attack or a chain fork (as we are witnessing with the failure of Bitcoin Cash), its reputation for network security and immutability is strengthened.

142d. When China took a heavy-handed approach to regulation by shutting down Bitcoin exchanges in 2017, we witnessed several informal exchanges and OTC markets appear following the demise of each centralized exchange.

142e. The regulatory attack also encouraged people to hold Bitcoin for longer periods, as evidenced by a steep decline in sell volumes, which only reduced the amount of Bitcoin being traded and put upward pressure on its price.

142f. Also, these regulatory actions backfired by triggering the Streisand Effect, which is a phenomenon whereby an attempt to hide, remove or censor information has the unintended consequence of publicizing the information more widely, usually facilitated by the internet.

142g. As the world watched the situation in China unfold, both the Bitcoin price and global internet searches for the term Bitcoin reached new all-time highs.

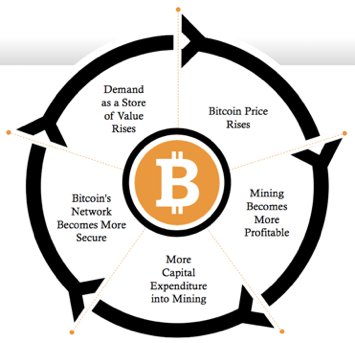

143. All of the adversity Bitcoin has faced so far has only fed its growth. Absent any top-down authority, Bitcoin is organic in the sense that it has grown from the bottom-up based solely on its own merits as money.

144. Network participants are all rewarded economically for their interactions with Bitcoin, which creates a flywheel effect on its price and network security (h/t @aantonop):

145. As the Bitcoin network adapts to better meet the demands of its constituents, it in turn recruits more network participants. This positive feedback loop promotes the sustained growth of its network and fuels powerful, multi-sided network effects.

145a. The basic example of a powerful 1-sided network effect is a social network (or a telephone network, as outlined earlier). The more people on a social network, the more valuable it is for others to be on it, as there are exponentially more possible connections.

145b. It can, however, be disrupted by a competitor that provides a more valuable service to its single customer cohort, the users, who might then transition to the new service (as happened when Facebook disrupted MySpace).

145c. Successful 2-sided markets (like eBay or Craigslist) are significantly more difficult to disrupt. Consumers want to be there because merchants are there, and merchants want to be there because consumers are there.

145d. To disrupt a 2-sided network, you have to simultaneously introduce a superior value proposition for both parties, otherwise nobody moves.

145e. That is why Craigslist, despite its limited innovation over the years, has been able to leverage its early 2-sided lead and is still a dominant website today.

145f. Bitcoin has a unique 4-sided network effect that insulates it from disruption and supports its growth. These are the four constituencies that participate in expanding the value of Bitcoin as a result of their own self-interested interaction with its network:

145g. This 4-sided network effect makes Bitcoin’s first mover advantage seemingly indomitable.

146. As an adaptive monetary technology, Bitcoin's network effects encompass the liquidity of its market, the number of network participants, the community of software developers who support it and its brand awareness.

147. Large investors will always seek the most liquid market for ease of entry and exit. Consumers, merchants and developers tend to join the largest of each of their respective Bitcoin communities, which only reinforces their social interconnectivity and cohesion.

148. Brand awareness is innately self-reinforcing, as any cryptoasset competitor will inevitably be mentioned in comparison to Bitcoin.

148a. An aside on Bitcoin’s brand awareness: As we have learned, the value of any money is derived from its social consensus, or the mutually shared beliefs of its users.

148b. Religious undertones are prevalent in most forms of money (In God We Trust on the US Dollar) and they are also part of Bitcoin’s aura (The Genesis Block, Bitcoin Evangelists).

148c. The most important of these quasi-religious ideas is the mythological bedrock Nakamoto laid with his enigmatic appearance in 2008 and then with his mysterious disappearance 3 years later.

148d. Assuming Nakamoto was a lone wolf, it is arguable that his disappearance transformed him from a person into a mythological figure.

148e. This mystery fuels the brand awareness of Bitcoin and reinforces its quality of decentralization, as there is no single individual to vilify, denigrate or otherwise target in an attempt tarnish Bitcoin’s symbolism.

148f. Like a super hero with a secret identity, all we have is the icon of Nakamoto as a cryptic genius – the godhead of Bitcoin.

149. Since money is a social network, the price of a monetary good is a reflection of how widely adopted it has become or is expected to become. The price of a monetary good in excess of its industrial demand is its monetary premium.

149a. This is the only rational basis for the common criticism that Bitcoin is a bubble, as it is purely a monetary technology and has no industrial demand whatsoever (h/t @real_vijay).

149b. However, this premium is the defining characteristic of all forms of money, as all monetary value is based on the optionality it gives its user for exchange across scales, space and time.

149c. Actual bubbles consist of the market distortions in which price exceeds value, like those created by central bank manipulations. If monetary premium is considered to be a bubble, then money is the bubble that never pops.

149d. As a pure bred monetary technology, Bitcoin derives none of its value from alternative uses:

150. Although there is no established price pattern for a digital good that is becoming monetized, Bitcoin’s price appears to follow a fractal (a recursive, self-similar shape) wave pattern of increasing magnitude commensurate with its level of user adoption.

150a. The volatility of this price pattern is exacerbated by Bitcoin’s perfect price inelasticity of supply (as discussed earlier). Each iteration of the fractal wave pattern appears to match the standard shape of the Gartner hype cycle:

150b. Here we show Bitcoin’s entire price history, from a logarithmic perspective, with the Gartner hype cycle fractal wave pattern iterations located inside boxes:

151. These extreme price cycles draw in new Bitcoin owners as each fractal wave crests. Some of these new owners buy in near the peak, only to be crushed in the trough.

151a. Most will capitulate, but those who remain because of their long-term conviction in Bitcoin (typically the most studious of history and monetary evolution among them) become the newest hodlers of last resort.

151b. A good proxy for the depth of these layers is the lowest price Bitcoin hits each year, which indicates the rising collective obstinacy of these hodlers:

151c. The best proxy for the timing of these fractal wave patterns has been the quadrennial Bitcoin inflation rate adjustment, when the amount of new Bitcoin rewarded at the close of each block is reduced by half, an event commonly known as the halving:

151d. The magnitude of each cycle is exacerbated by Bitcoin’s absolutely fixed supply schedule, as increases in demand are expressed exclusively through its price, which historically leads to market frenzies at each peak.

152. The long game for Bitcoin, and its final fractal wave pattern, will begin when and if central banks begin accumulating it as a reserve asset (more on this later).

153. In this way, the bedrock of the Bitcoin network’s expansion is the intransigency of its hodlers of last resort. Although they constitute a small minority of the whole, these stubborn hodlers will contribute to ongoing Bitcoin adoption in a meaningful way.

154. When it comes to group preferences, certain types of minorities – those who stubbornly insist on a particular preference – that constitute even a small level of the total population (often less than 4%) can cause the majority to submit to their preferences.

155. Another clever concept from @nntaleb, called the minority rule, is the result of complex system dynamics, like those inherent to human interaction.

156. The nature of complex systems (society) is that the collective behaves in a way not predicted by its individual constituents (people). The interactions between its constituents matters more than their individual natures.

157. These interactions, while complex, can obey simple rules, like the minority rule (or the rule that barter economies settle on a medium of exchange or that the hardest form of money always outcompetes).

158. Any domain that is disproportionately impacted by the preferences of a small minority is influenced by the minority rule. Such domains include:

158a. Science – Similar to markets which move based on the actions of the most motivated buyers and sellers, science is not based on the consensus of its constituents, it is the minority body of knowledge remaining after removing disproven hypotheses.

158b. Law – A law abiding citizen will never commit criminal acts but a criminal will readily engage in legal acts, and criminal behavior has been shown to be contagious within certain social groups.

158c. Imports – In the United Kingdom, where the (practicing) Muslim population is only around 4%, a very high proportion of the meat we find is halal. Close to 70% of lamb imports from New Zealand are halal. The same population and import proportions hold true in South Africa.

158d. This dynamic of scale can be explained quantitatively. In mathematical physics, renormalization groups are an apparatus that allow us to see how things scale up or down:

159. Languages also often adhere to the minority rule. For instance, French was originally intended to be the language of diplomacy as civil servants from aristocratic backgrounds used it, while English was reserved for those engaged in commerce.

159a. In the rivalry between the two languages, which are still considered two of the international languages (a third, Spanish, was added later because of its widespread use), English won as commerce came to dominate modern life.

159b. There is an asymmetry that those who do not have English as their first language usually know basic English, but native English speakers knowing other languages is less likely.

159c. If a meeting is taking place in an international office in say, Istanbul, among twenty executives from a sufficiently international corporation and one of the attendees does not speak Turkish, then the entire meeting will be run in English (the commercial Lingua Franca).

160. Money is an emergent property, as it is an expected result of complex human interactions within a barter economy. Similar to language, it is a means of expression, only it is used to express value instead of information or emotion.

160a. The US Dollar is the Lingua Franca of money today, as it belongs to one of the world’s largest economies (an economy which also happens to effectively control the global banking system).

160b. As the digital age matures and the world becomes increasingly interconnected, ever-more commerce and administration will be conducted over the internet.

160c. Also, fully interconnected trade networks will level the terrain of commerce and increase free market competition among different forms of money.

161. By considering the minority rule in the context of Bitcoin adoption, we can reasonably expect Bitcoin to increasingly impose its rules on established economies and become the Lingua Franca of digital commerce.

161a. Bitcoin already has the advantage of being the hardest form of money ever invented, and its rules are immutable, which is the highest form of intransigency possible.

161b. It also has unrivaled brand awareness, fed by the mystery of its creation myth, and the support of free market fanatics all over the world which contribute to the growth of the Bitcoin minority.

161c. Once its obstinate minority reaches a certain size, the unbreakable rules of Bitcoin will begin to stubbornly impose themselves on the established economic order.

161d. In the words of Margaret Mead “Never doubt that a small group of thoughtful, committed citizens can change the world; indeed, it’s the only thing that ever has.”

162. In respect to monetary competition, Bitcoin can be regarded as a superior species of money:

162a. Bitcoin is superior in the market for money because it possesses all the ideal features of digital cash money and a market dominant position by virtue of its 1st mover advantage which is fortified from disruption by its open-source design and multi-sided network effects.

162c. With the invention of Bitcoin, the world finally has a synthetic form of money with a stock-to-flow ratio that is guaranteed to increase (until it reaches infinity) and an unstoppable, permissionless payments channel.

162c. Its digital nature makes it salable across space in a way never before seen, as it can be stored in analog, human or computer memory and transmitted at the speed of light.

162d. The deep divisibility of each Bitcoin into 100 million Satoshis makes them supremely salable across scales.

162e. Its informational and nonperishable nature, when considered in combination with its superior hardness, gives Bitcoin unprecedented salability across time. This design makes it an impeccable store of value.

162f. Finally, by eliminating all intermediary control (which is inherent to government money) Bitcoin resists value debasements, censorship and confiscation.

163. Bitcoin is a tool for freedom. As the most accessible asymmetric bet in history, Bitcoin is also a unique investment opportunity.

164. As long as it continues to operate successfully in its current form, Bitcoin will function healthily as the stateless base money protocol for the digital age – which makes it a viable contender in the $100T market for global money:

165. Like a call option, a bet on Bitcoin is asymmetric, meaning that an investor’s downside is limited to 1x whereas their potential upside is 100x or more.

166. Investing in Bitcoin can be considered a bet on its adoption as an uninflatable, politically neutral store of value and as an unstoppable, permissionless payments channel.

167. Bitcoin may also become part of a much bigger wave of innovation. The greatest wealth is created by being an early investor in innovation.

167a. Making such investments requires believing in something before the majority of people understand it – which also often entails enduring mockery, ridicule and criticism for your non-consensus perspective.

167b. As Mark Yusko, one of my favorite hedge fund managers, describes the coming crypto era (h/t @MarkYusko):

167c. The TrustNet can be thought of as the dawn of trustworthy computing (h/t @NickSzabo4)

167d. In theory, it will enable new technologies such as the internet of things, decentralized autonomous organizations, self-owning commercial assets and decentralized internet provisioning (to name a few).

167e. This anticipated innovation wave is consistent with a multi-decade cycle of information technology expansion, consolidation and commoditization (h/t @cburniske):

167f. Bitcoin will likely function as the systemic core and base money system of the Trustnet. In this cycle, all markets that are enabled by this technology will rely on the Bitcoin blockchain as a common value system, final settlement mechanism and temporal anchor point.

168. Bitcoin is a momentous innovation of the digital age. As such, it has many unique characteristics, properties and capabilities never before seen in a monetary technology:

169. Bitcoin has made a major impact in the world in its 10 years of existence, and it still holds a great deal of promise for the future. Given its inextricable relationship with money and Bitcoin, the concept of time is worth exploring more deeply.

170. It turns out that time’s role in our lives, individually and collectively, is the key to understanding prosperity and the ways in which Bitcoin could play a key role.

171. THE SIMPLE TRUTH ABOUT TIME: Time is the ultimate resource. Its absolute scarcity bounds the entirety our stories, both as individuals and societies. As the destroyer of all things and the healer of all wounds, it is the grand paradox of nature.

172. Individually, the only scarcity we face is our limited time on Earth. As a society, the only scarcity we deal with is the total amount of human time, effort and ingenuity available to be directed at the production of goods.

173. This scarce resource, which we will call human time, is the ultimate societal means of production. Humans have never fully exhausted any single natural resource and production has only been limited by the human time directed at production.

174. The price of all natural resources, in terms of human time, has always decreased steadily over the long-run as our technological advancements have dramatically increased our productivity.

175. Not only have we not depleted any natural resource, but the proven reserves (the amount still within the Earth) continue to increase despite our increasing rates of production, as new technologies enable us to discover and excavate ever-more natural resources.

175a. The best evidence of this simple fact is gold: if the annual production of the one of the rarest metals in the Earth’s crust goes up every year, then it makes no sense to consider any other natural resource being scarce in any practical sense.

175b. Echoing back to the fundamental market realities related to deferred consumption and investment – the real cost of anything is always its opportunity cost in terms of goods forgone to produce it.

176. In terms of natural resources, only human time is truly scarce, which makes time the ultimate resource.

177. As more humans exist, there is more human time to direct towards the extraction and production of natural resources.

178. As we have learned, productive output per unit of human time (productivity) can be amplified by leveraging technological solutions to problems (tools).

179. In economics, a tool or technology is considered to be both:

179a. For example, once one person invented the wheel, everyone else could copy its design and make their own, and their use of this design would in no way reduce others’ ability to benefit from it.

179b. Like the candle whose flame burns undiminished even after igniting a thousand others, the benefits of innovation ultimately accrue to everyone without detracting from the innovator in any way.

180. Natural resources and innovation are always and only the product of human time. Therefore, in terms of production, human time is the ultimate resource and essence of value.

181. To keep score, people needed a way to reliably store the value they produce with their time, so that they can exchange it in the future for other peoples’ time, effort and ingenuity.

182. Conceptually then, money is frozen time. It is earned by sacrificing human time and can be traded for commensurate sacrifices from others. The age-old problem faced by people is collectively deciding which monetary technology can best serve this purpose.

183. People, acting in self-interest, live within technological and economic realities that shape their decisions and provide them incentives to persist, adapt, change or innovate.

183a. It is from the countless collisions of these complex human interactions that spontaneous monetary orders have emerged and decayed.

183b. History has shown us myriad cases of a good being subjected to market-driven natural selection, achieving a monetary role and subsequently having its role taken by a superior technology.

183c. Whatever monetary media people chose as a store of value was always subject to being produced in greater quantity, so the producers could acquire the value stored in it.

183d. Gold came close to solving this problem as it is indestructible, expensive to mine and its flow is relatively predictable. However, gold’s physicality led to its centralization within bank vaults and its compulsory replacement with soft government money.

184. Until the invention of Bitcoin, all forms of money were subject to having their value stolen by producers of the monetary good. This made all monetary technologies before Bitcoin imperfect in their ability to store value across time.

184a. Bitcoin’s finite supply makes it the best medium to store the value produced by finite human time. In other words, Bitcoin is the best store of value humanity has ever invented, as it is the only monetary technology that cannot be debased over time.

184b. The informational, intangible and purely digital nature of Bitcoin enables it to achieve absolute scarcity, a property that was previously exclusive to time itself.

184c. The cold hard truth is that the absolute scarcity of Bitcoin makes it the perfect modality for freezing and transacting the only other absolutely scarce resource – time.

185. Innovations of this magnitude are virtually impossible to predict; however, they do follow a familiar adoption pattern called the Diffusion of Innovations (h/t @Melt_Dem):

186. Once a certain rate of adoption is achieved, the innovation reaches a tipping point and its continuous spread becomes practically unstoppable (a concept of preferences closely related to the minority rule discussed earlier).

187. All ubiquitous technologies today, beginning as fledgling innovations themselves, have traversed this path to mainstream adoption. Here we show some of the most impactful innovations since the year 1900 and the rapidity with which they were adopted:

188. Advances in telecommunications and distribution methods have accelerated the pace with which new innovations are adopted. Today, the internet causes breakthrough innovations to spread like a wildfire throughout the minds of people all over the world.

189. As an informational technology, Bitcoin also becomes more trustworthy with every passing day that it successfully operates.

190. Things in this world fall into one of two general categories: perishable and nonperishable. The distinction between the perishable (humans, single items) and the nonperishable is that the latter does not have a natural, unavoidable expiration date.

191. The perishable is typically physical in nature, meaning it is subject to physical degradation, whereas the nonperishable is typically informational in nature.

192. A single car is perishable, but the automobile as a technology has survived for a century and can be reasonably expected to persist for at least another one.

193. An individual human will die, but his genes (which are digital) can be passed on for innumerable generations.

195. The only effective judge of things is time, as time is the ultimate destroyer of all things. The Lindy Effect is closely related to antifragility, as the ravages of time are a potent form of adversity.

195a. Using arbitrary math, if a book is still in print after 50 years, it can be expected to remain in print for another 50 years. If it’s still in print for another 50 years after that, then perhaps it can then be expected to remain in print for an additional 120 years.

195b. At some point, the Lindy Effect may imply an unlimited life expectancy. A book like the Bible, which has been in print for thousands of years, can be reasonably expected to remain in print for the rest of human history.

195c. If you had conducted a survey in 1995 and asked people whether they believed the internet would be a permanent feature of their lives, you would have probably received mixed responses.

195d. If you conducted the same survey today, people would resoundingly agree that the internet is here to stay.

196. So, the longer a technology lives, the longer it can be expected to live. Since Bitcoin is a technology, every day that it continues to successfully operate increases its life expectancy.

197. Further, as we have learned, the core moving parts of Bitcoin are mathematics and human nature – two concepts which are very “Lindy” and can be reasonably expected to persist for the rest of human history.

198. Bitcoin’s ever-growing life expectancy increases its perceived trustworthiness and eventually it will be regarded as a permanent feature of our modern lives in the same way the internet is today:

199. The Lindy Effect is universally applicable across time. The same competitive dynamics that caused the ascent of gold into a monetary role are now driving Bitcoin adoption.

200. In this sense, the future is in the past. As the Arabic proverb says: he who does not have a past has no future.

201. Notwithstanding the past century of central bank coercion, hard money is the norm of human history and we are witnessing its reemergence with the rise of Bitcoin.

202. Threatened by its continued growth, incumbents will ratchet up their efforts to prevent Bitcoin's ascent and protect the monopoly on money enjoyed by central banks over the past century.

203. To protect central bank monopoly positions, governments have resorted to passing onerous laws against their citizens. Governments seek to insulate their national currencies from free market competition employing legal measures such as:

204. With Bitcoin, regulators face a unique dilemma. Bitcoin exists orthogonally to the law, and there is virtually nothing that any authority (or anyone for that matter) can do to affect its operation.

204a. Regulations were designed to govern people and entities and are not equipped to deal with a decentralized network that autonomously proliferates itself.

204b. Regulators are really good at targeting centralized marks, like an individual business or its CEO, and enforcing laws against them. However, regulations have proven to be largely impotent against decentralized services.

205. To understand this point, consider the case of BitTorrent, a decentralized peer-to-peer file sharing service:

205a. Once installed on a computer, BitTorrent enables user nodes to upload and download movies, music and other media directly from one another using encrypted communication channels.

205b. Unlike the failed client-server models of centralized platforms which regulators easily shut down, the BitTorrent protocol never holds any of the media files, it only facilitates the transfer of files between individual users:

205c. Architecturally, the entire software codebase of the protocol exists on every user machine that downloads it, making it virtually impossible for a regulator to target and shutdown as there is no single point of vulnerability (censorship resistance).

205d. By 2009, peer-to-peer file sharing using decentralized protocols like BitTorrent accounted for up to 70% of internet traffic worldwide.

205e. Bitcoin has already exhibited similar properties to BitTorrent as regulators have been incapable of containing the expansion of its network or shutting it down.

206. In essence, open-source software projects like Bitcoin are just information – software written in a computer language called code. Since it is just code, Bitcoin can be printed out, written down, spoken or memorized.

206a. Bitcoin is also a form of money, so it makes money and information the same thing. This concept was summed up nicely by @Naval in 2017:

206b. Since it is simply language, Bitcoin unambiguously falls under the Freedom of Speech Protections offered by the First Amendment to the United States Constitution (see the legal precedent set by PGP in 1995 - h/t @Beautyon_)

206c. Former chairwoman of the Federal Reserve Janet Yellen confirmed “The Federal Reserve simply does not have the authority to supervise or regulate Bitcoin in any way.”