,

23 tweets,

5 min read

Read on Twitter

I posted this string yesterday. It was supposed to include 22 tweets. Someone Dm'd me that it seemed like the thread was cutoff. Indeed it was. I only saw 11 of the 22 posts. No idea what Twitter is up to, but here is the original thread again in its entirety.

1/ There has been some discussion the past few days with respect to Tesla’s recent equity raise, particularly the convert hedge and the impact that might have had on the demand for the equity in this deal.

2/ That subject has been well covered well by others elsewhere. I wanted to address here the overall capital markets story, especially for the equity.

3/ As a former capital markets banker I can tell you that book building is about the art of deception. No one, except the company and the book runners, knows who is truly involved and who isn’t. Not during the deal, not after. A buyer knows his allocation, that’s it.

4/ Bankers are supposed to protect confidentiality. They are also supposed to paint a picture, create demand and reward buyers with a deal that trades up after the break. It is a game and all the players know how the game is played.

5/ In only the rarest of instances do bankers open the kimono and let their accounts know if a deal is struggling. And in those instances, favors are called in and often repaid, which is why the favor is granted in the first place.

6/ You want the next hot IPO or secondary? You have to buy the pigs too. Now, in no way am I implying Tezzla’s recent deal struggled. However, I do think there is more here than meets the eye.

7/ In the discussion about the recent equity raise and convert, the relevant number is the roughly net $300mm in proceeds that indeed went out the door to fund the convert hedge. Leaving $450mm for the general public. $425mm less Musk’s purchase.

8/ The color I gathered on the deal was “it wasn’t as high a quality book as the previous equity raise” which to me means no Fido and T Rowe. I believe Fido bought up to 5% of the last deal, possibly more.

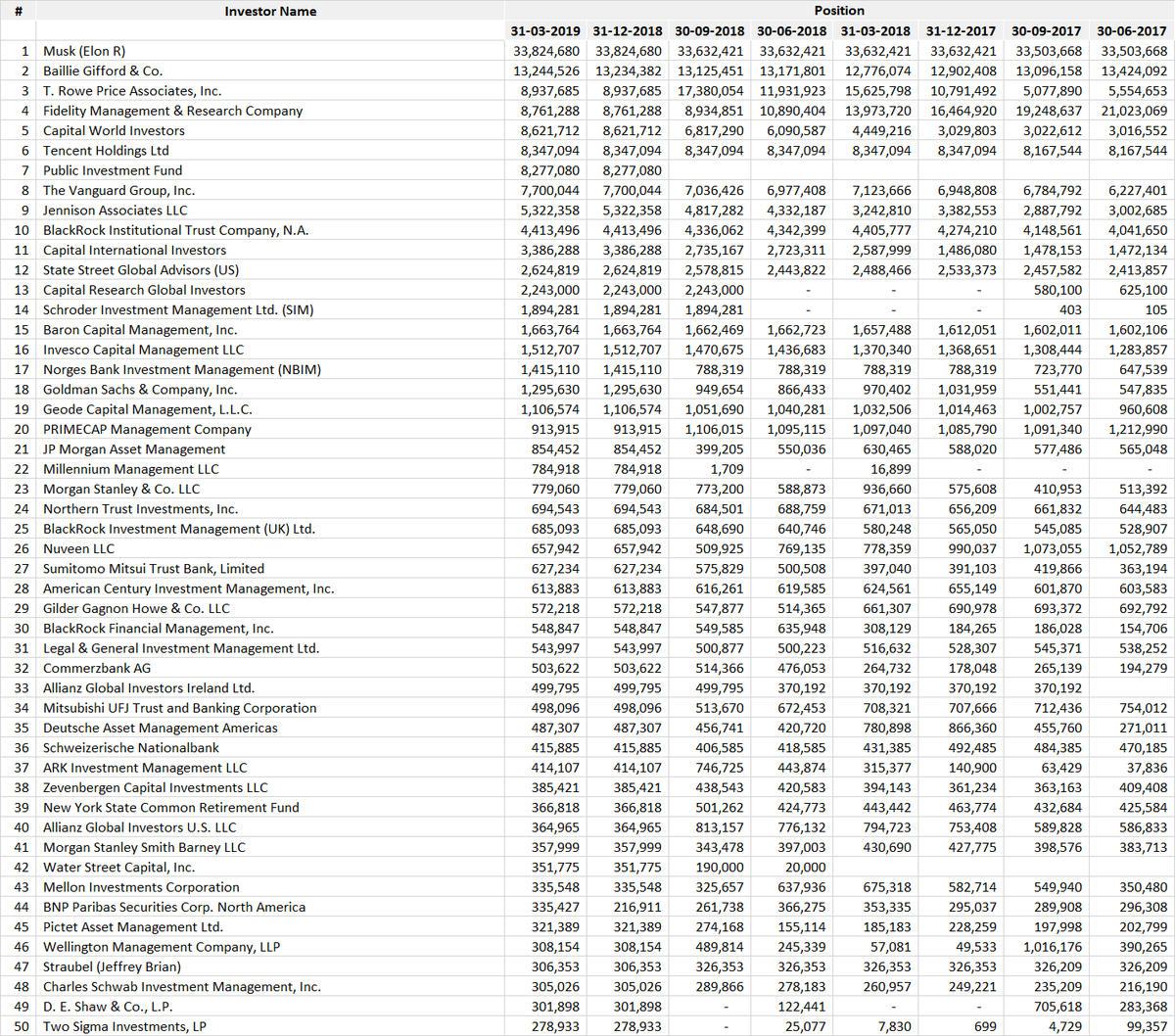

9/ I was also told that “6-8 existing holders bought 70%.” So $300mm divvied up is $40mm-ish each leaving $125mm scattered to others. Attached in the next post (#10) is the most recent shareholder list ranked by changes in share counts as of 3/31/19.

10/ This is Thomson Reuters data which does not update until after all 13F’s are filed. You see here the Saudi money and a big change at Cap World, but not Ellison (don’t ask me why). Column A is the actual rank number by shares held.

11/ Cap World is the subadvisor to the American Century funds, which have been the largest fund buyers of Tesla shares in the last six months (unfortunately for AmCentury shareholders. . .)

12/ Here are the holdings broken out by individual funds, which sometimes can be helpful in painting a better picture of who owns this in size and who has been buying. Highlighted names are actively managed mutual funds (mostly) as opposed to passive vehicles.

13/ Here are the top 50 holders by name and/or fund complex ranked by absolute holdings.

14/ This, IMO, is the tweet that sums it all up. If the upside is so bright, this should have been a $2.0 bil equity raise as it was before the 3 was launched. They cleared $450mm.

15/ We’ve all speculated about how much Tezzla needs just to fund losses and other sundries, and I believe the general consensus is this raise gets them 6-9 months of breathing room unless sales fall apart more.

16/ I have said previously stated the convert market is hardly a bell-weather of demand. While there are indeed long-only convert buyers in the mix, a convert is often a heavily hedged instrument used in a tightly structured rate arbitrage play.

17/ The convert market isn’t telling you this is a great credit. Well guess what? The equity market isn’t either. 6 holders swallowed hard in the hopes they will get treated well in the next hot IPO.

18/ In a stock that trades like water like Tezzla there was absolutely no reason for anyone to buy a deal at no discernible discount. Cap World or anyone else could have bought shares whenever it needed. ARK proved that just a week prior.

19/ This equity print was not a ringing endorsement of the biz. An endorsement would have been 2-3x the size.

20/ So Goldman, MS, Citi and the others are now working overtime to keep this afloat to continue the illusion it was well put away. And will for a few more days. And then we get May’s delivery numbers. The froth on Friday will be short-lived.

21/ Why? Because the fundamental picture hasn’t changed. If it were on the upswing (it isn’t), your anemic $450mm in net equity proceeds would have been $2.0 bil. Doing equity in conjunction with converts was a way to hide paltry equity demand.

This was a desperate raise from a desperate company. Do not be fooled by the price action. If we see 13Fs in August that disprove my conclusions, I’ll be the first to retract. But we won’t. There were no new real buyers.