There is a lot of debate going on about what negative interest rates mean for banks and how it’s bad, but (life) insurers are often forgotten. So here’s a thread about this because I think it's HUGE.

Arguably it’s an even bigger issue for life insurers than for banks and that’s probably why Allianz’s CEO was very vocal about it recently.

More anecdotic: the CFO of a German large bank once told me that the ECB would only stop its monetary adventures once a German insurer goes bust… So what is this all about?

The problem is this: in a nutshell, to check if they are solvent, insurers discount their liabilities at market interest rates and compare this to the market value of their assets.

BUT they usually have much longer duration on their liabilities than on their assets. So, the lower the rates, the higher the economic value of their liabilities – not always matched by a higher value of their assets.

The problem is complexified by the fact that market interest rates barely go beyond 30 years (50 years if you want to stretch a bit, but with shitty liquidity) whereas insurers' liabilities often go much beyond that.

So how do you calculate a market rate to value those liabilities? Enters the famous UFR – Ultimate Forward Rate. This is a hypothetical rate set by the regulators and supposed to reflect the rates at the longest possible horizon.

Rates are then interpolated from market values to that rate. All good, you think? Well, there are two catches.

The first one is “when do you start to interpolate”? 20y ? 30y? 50y? Surely it does not make a big difference, you might think? Think again.

The second one is: “what the level of the UFR”? Mmmm let’s see. I’m opening my Bloomberg, I can see € 50y swap is 0.3%. So I guess the UFR is what… 0.5% maybe ? 0.7% tops ?

AHAHAHAHAHAHA it’s 3.9%. The UFR level is a f**** joke. IT IS NOT EVEN REMOTELY LOOKING LIKE REAL WORLD INTEREST RATES ; which mean that all insurer liabilities are grossly undervalued.

Any idea of the financial impact? Well, the EIOPA just released a nice report yesterday on Solvency 2 review (878 pages if you have spare time) and they focused on this quite a bit.

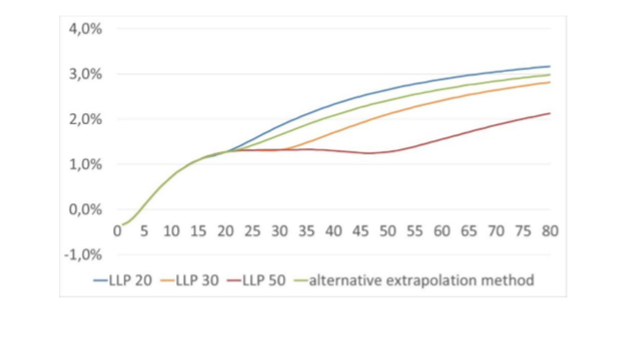

Here’s a chart illustrating the magnitude of the interpolation problem, e.o.y. 2018, when rates were still “high” (15y at 1%) and the UFR at 4.05% (LOL.)

You can see how massive the impact of the interpolation choices is. (LLP means Last Liquid Point and the number is the maturity of that point in number of years.)

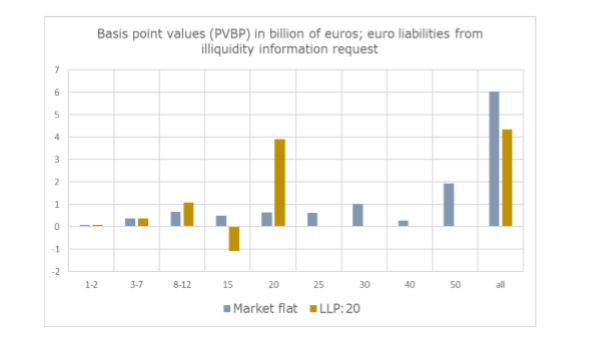

OK, but that’s just a curve. Is there an actual € impact of all this? Here’s an extraordinary chart from EIOPA. Y-axis is *billion* euros for the sample of insurers surveyed by EIOPA. It is the impact in billion euros of a 0.01% move of the € curve.

Yes, you read this correctly. 0.01%. One basis point. The blue bar “All” tells you how much the economic values of insurers liabilities move when rates go down 0.01%. The brown bar tells you how much the “regulatory” values of insurers liabilities move when rates go down 0.01%.

The difference is almost 2bn€ per basis point! 2 000 000 000€ for a tiny 0.01% move !!! Insurers totally misrepresent the interest rate risk they are taking!

So the EIOPA is aware of this and proposed a few alternatives summarized in that chart

One big thing to notice on this chart: it's all very nice and the interpolation methods do change, but it's still TOTALLY F**** disconnected from reality which is that rates are at 0.3% today, not 4% !!!!!

And yet, those changes alone produce those results: change in SCR ratios for EU insurers in those approaches.

Hellooooo Germany? Are you still alive? Netherlands not too happy too. The impact is just massive… and this is why EIOPA will probably conclude it’s best not to change anything.

And again, this is still with totally fake interest rate levels! They’re not brave enough to show the impact of using real interest rates.

So the conclusion to all those opposing ECB policy: don’t bother lobbying the ECB, lobby the EIOPA and get them to make the Solvency rules realistic. I can guarantee you that the monetary policy will change in a week😊

I should point out one last thing : large listed insurers are more aware of this than smaller non listed ones and have much less exposure to this issue.