THREAD

The financial crisis of 2008 explained

I have been asked quite often about the crisis – what really caused it, and what are the implications – what should we learn (or have learned) from this? And what is the connection between this and Islamic banking?

The financial crisis of 2008 explained

I have been asked quite often about the crisis – what really caused it, and what are the implications – what should we learn (or have learned) from this? And what is the connection between this and Islamic banking?

Debt, Derivatives and Profit at all costs

Why is this important

First of all, non-finance people generally do not understand (very well) how money and markets work, yet they (we) are the ones who bore the brunt of the crisis.

We have a right to know why it ruined so many lives

Why is this important

First of all, non-finance people generally do not understand (very well) how money and markets work, yet they (we) are the ones who bore the brunt of the crisis.

We have a right to know why it ruined so many lives

and how it could have been allowed to happen. Secondly, it is important to learn the lessons, so we do not repeat it.

But I think we have short memories and it can easily happen again.

But I think we have short memories and it can easily happen again.

Ok, so what happened?

We have to go back to 1933 when the Glass Steagall Act was first passed. It separated investment and commercial banking activities. This was in response to the 1929 crash - the Great Depression. Banks had begun to act irresponsibly,

We have to go back to 1933 when the Glass Steagall Act was first passed. It separated investment and commercial banking activities. This was in response to the 1929 crash - the Great Depression. Banks had begun to act irresponsibly,

give unsound loans, engaging clients to invest in stocks (that the banks had just bought!), and so on.

The aim was to tell banks either to look after customer funds, OR invest and speculate – but you cannot do both!

In,1998, several key parts of this act were removed,

The aim was to tell banks either to look after customer funds, OR invest and speculate – but you cannot do both!

In,1998, several key parts of this act were removed,

after decades of lobbying (by banks, of course). So banks, whose deposits were protected by Federal insurance (FDIC) could now, once again, undertake risky business.

Following the dotcom crash of 2000, US interest rates were as low as 1% (sound familiar?).

Following the dotcom crash of 2000, US interest rates were as low as 1% (sound familiar?).

Asset managers could not get decent yield in traditional markets such as bonds, so they turned to more risky securities, such as mortgage backed securities (MBS)

So, what are MBS?

Simply, they allow banks to give mortgages, and then bundle them together and sell them

So, what are MBS?

Simply, they allow banks to give mortgages, and then bundle them together and sell them

(at a discount) to investors. As long as the homeowners continue to service their mortgages, the investors get a return. Credit rating agencies would helpfully analyse the mortgages and give a credit rating to the bundle of MBS.

This works for banks as it lets them create mortgages, and then sell them quickly, and then they can create more mortgages, and repeat the process.

This was easy money for banks, so they went all out and gave as many loans as they could, and as quickly as they could.

This was easy money for banks, so they went all out and gave as many loans as they could, and as quickly as they could.

In order to do this, they relaxed credit requirements for borrowers.

They gave mortgages to homebuyers of lower credit quality, and these were called sub-prime mortgages. They also skipped on the paperwork requirements, because it was more important to create these mortgages so

They gave mortgages to homebuyers of lower credit quality, and these were called sub-prime mortgages. They also skipped on the paperwork requirements, because it was more important to create these mortgages so

they could package and sell them, and repeat the process. If the risk of default was no longer with the bank, but passed on to MBS investors, then the bank did not care if a default occurred in the future. They were often given a low initial interest rate,

but this would step up in due course.

But nobody thinks that much about the future, right?

This happened a few years before the crash:

But nobody thinks that much about the future, right?

This happened a few years before the crash:

So, these lower quality mortgages were created and pumped rapidly into new MBS, which were still rated AAA or so by the agencies. That means they were supposed to be as safe as US govt Treasurys.

Fund managers and investors bought these MBS in a frenzy, due to the higher returns

Fund managers and investors bought these MBS in a frenzy, due to the higher returns

, in a low interest environment, and the attractive AAA rating.

“ in the mid-1990s $30 billion of mortgages constituted "a big year" for subprime lending, by 2005 there were $625 billion in subprime mortgage loans, $507 billion of which were in mortgage backed securities”

“ in the mid-1990s $30 billion of mortgages constituted "a big year" for subprime lending, by 2005 there were $625 billion in subprime mortgage loans, $507 billion of which were in mortgage backed securities”

Now let’s look at the role of derivatives.

MBS is explained above – CDO (Collateralised Debt Obligations) are similar - but they have one additional feature – the risk of the underlying mortgages was sliced into different levels of risk – from the “safest” (Senior tranche) to

MBS is explained above – CDO (Collateralised Debt Obligations) are similar - but they have one additional feature – the risk of the underlying mortgages was sliced into different levels of risk – from the “safest” (Senior tranche) to

to the middle risk (Mezzanine) to the more risky tranches (Equity, or Junk). For example:

Here, Investor A has the safest investment, and investor H has the riskiest. Another way to slice risk is that the equity investors take the brunt of the first defaults.

Here, Investor A has the safest investment, and investor H has the riskiest. Another way to slice risk is that the equity investors take the brunt of the first defaults.

The Senior investors would only be affected if more than 8% of borrowers defaulted.

It is these risks the rating agencies said were as safe as US Treasurys. They were paid to say this.

It is these risks the rating agencies said were as safe as US Treasurys. They were paid to say this.

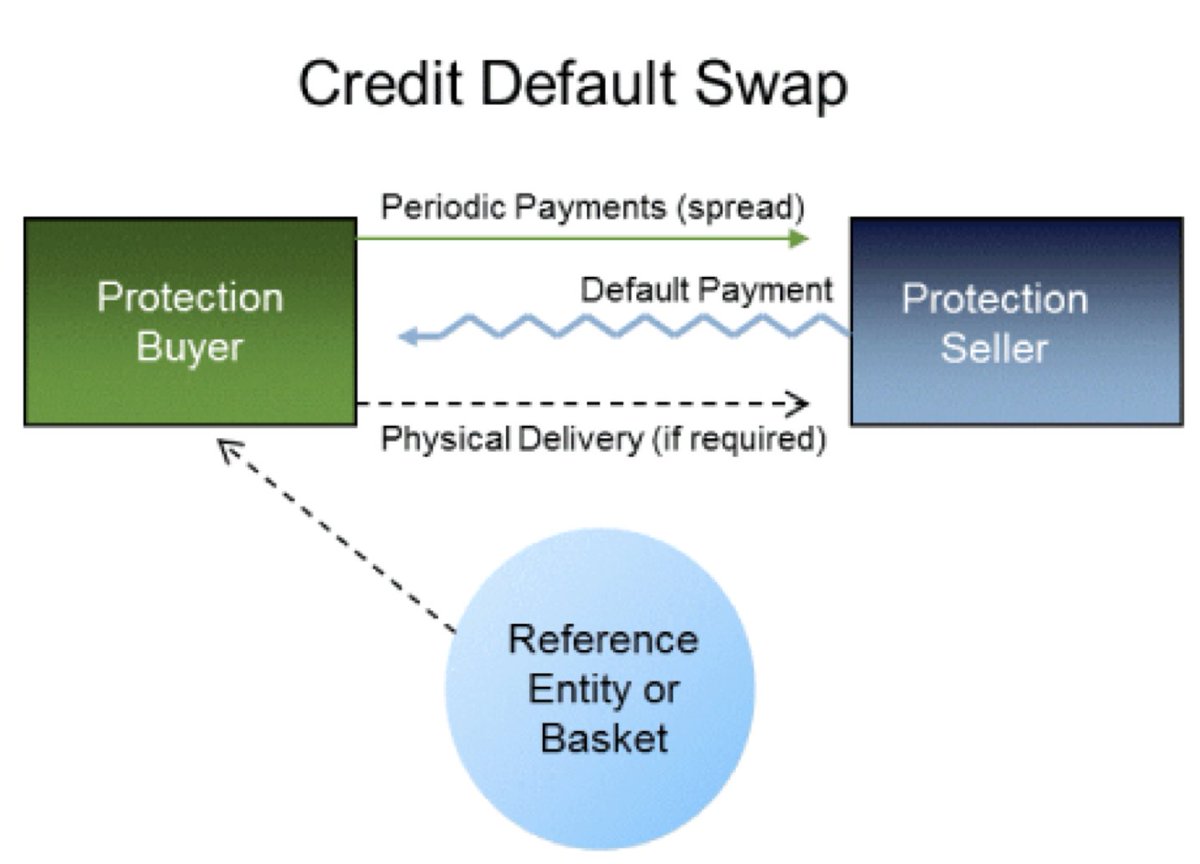

Next, let’s look at Credit Default Swaps (CDS) – some investors wanted further protection in the form of insurance in case the borrowers defaulted. So CDS were created for this – investors pay insurance to the CDS issuer, and if the mortgages default,

the CDS issuer (the insurer) would make good the investor’s losses. In theory.

Insurers were more than happy to rake in insurance premiums as they thought these borrowers just would not default – they saw this as free and easy money, and issued CDS at a startling rate.

Insurers were more than happy to rake in insurance premiums as they thought these borrowers just would not default – they saw this as free and easy money, and issued CDS at a startling rate.

AIG (a big insurer) took in over $3bn annually from this, about 17.5% of their total revenue.

CDS are not regulated, meaning there are no exact figures for how many were created. One estimate states the volume of the CDS market is 3x global GDP.

CDS are not regulated, meaning there are no exact figures for how many were created. One estimate states the volume of the CDS market is 3x global GDP.

. By the end of 2007, over $62 trillion were outstanding. That is many more times larger than the actual debt that was being insured!

It is amazing that with a single debt, you can create multiple CDS to insure it – all because the issuer of the CDS thought it was

It is amazing that with a single debt, you can create multiple CDS to insure it – all because the issuer of the CDS thought it was

easy and free money.

How can this cycle of CDO creation exceed the value of debt they insure? By re-iterating the process – using CDO’s (rather than the original debt) as the underlying asset for new CDO’s

How can this cycle of CDO creation exceed the value of debt they insure? By re-iterating the process – using CDO’s (rather than the original debt) as the underlying asset for new CDO’s

Now, back to the story…

We have a lot of new subprime borrowers. Before, if they fell behind in payments, they could refinance, as home values were increasing.

We have a lot of new subprime borrowers. Before, if they fell behind in payments, they could refinance, as home values were increasing.

It is hardly surprising house prices were rising, because banks were pumping out cheap debt to poor credit borrowers, and that debt fuelled unsustainable price growth.

However, when property values began to decline from 2006, re-financing became more difficult. Also, the impact

However, when property values began to decline from 2006, re-financing became more difficult. Also, the impact

of Adjustable Rate Mortgages kicked in. Remember how quickly the lenders pushed out mortgages? One way was to reduce initial interest rates, but these rates then stepped up after a few years. When this happened, the subprime borrowers struggled to meet much higher repayments.

They could not refinance as property values were falling – negative equity.

They began to default.

Look at the types of mortgages that resulted in default: we can see that subprime adjustable rate were the massive driver:

They began to default.

Look at the types of mortgages that resulted in default: we can see that subprime adjustable rate were the massive driver:

Now we have a waterfall effect – these defaults meant the owners of MBS and CDO’s began to feel the effect of defaults.

Their securities dropped in value, and quickly - but not immediately.

Their securities dropped in value, and quickly - but not immediately.

What happened first, when banks and funds realised their value was falling, they decided to offload them to new investors who did not know their price was falling. They still had a good credit rating, in theory.

These banks and fund managers were selling bad securities to

These banks and fund managers were selling bad securities to

buyers who did not do their homework.

Ok, so the defaults happened, investors took BIG losses. Many, of course, had insurance in the form of CDS, so they now went to the insurers such as AIG, and asked for their compensation.

Ok, so the defaults happened, investors took BIG losses. Many, of course, had insurance in the form of CDS, so they now went to the insurers such as AIG, and asked for their compensation.

AIG had little or no reserves set aside for this – they just did not imagine these defaults could happen.

AIG had to pay out around $25bn. The government had to step in to bail out AIG.

The drive for short term profit now came home to roost.

Not only did investors

AIG had to pay out around $25bn. The government had to step in to bail out AIG.

The drive for short term profit now came home to roost.

Not only did investors

and insurance companies lose money – now we began to see how the financial markets are highly connected and correlated, in a way that nobody (ie regulators) had not foreseen.

On 9 August 2007, BNP Paribas froze 3 funds

On 9 August 2007, BNP Paribas froze 3 funds

saying they had no way to value the CDO assets in them. This was the first major bank to acknowledge this.

Banks began to record losses from

1) defaults on mortgages they lent out

2) Losses on MBS they invested into

3) High bank levels of debt, leverage

Banks began to record losses from

1) defaults on mortgages they lent out

2) Losses on MBS they invested into

3) High bank levels of debt, leverage

Let’s look at what leverage is:

So what level of leverage is OK, and what level is risky?

We can see non financial corporates have had leverage levels of between 1x and 3.5x

Too much leverage is risky, because if revenue falls, you struggle to service your debt and you can quickly become insolvent –

We can see non financial corporates have had leverage levels of between 1x and 3.5x

Too much leverage is risky, because if revenue falls, you struggle to service your debt and you can quickly become insolvent –

insolvent – even if your business is still profitable!

Let’s look at leverage levels of banks at this time:

Yes, US banks had leverage levels of 35x before the crisis.

For each real asset worth $1 they owned, they gave out over $35 in loans. Think about that for a second

Let’s look at leverage levels of banks at this time:

Yes, US banks had leverage levels of 35x before the crisis.

For each real asset worth $1 they owned, they gave out over $35 in loans. Think about that for a second

Ok, so banks wrote off a lot of losses. What next?

Now, banks started to fail, Why?

Before the crash Lehmans bought 5 mortgage lenders, and of course, the aim was to pump out a lot of mortgages quickly, then to bundle them into MBS, and repeat. Easy money.

Now, banks started to fail, Why?

Before the crash Lehmans bought 5 mortgage lenders, and of course, the aim was to pump out a lot of mortgages quickly, then to bundle them into MBS, and repeat. Easy money.

Now, in Sep 2008, they wrote off almost $6bn on mortgage assets – the bank made overall losses. Their stock price plummeted from almost $70 to just over $10. The market knew this bank is almost dead, so they stopped providing short term liquidity in the interbank market.

This is the lifeblood of any bank – the ability to borrow short term funds on this market. When this dried up, Lehmanns could no longer survive.

The US Govt declined to bail them out – Lehmans folded.

Let’s not feel too sorry for the banks

The US Govt declined to bail them out – Lehmans folded.

Let’s not feel too sorry for the banks

– remember the homeowners, who took out the loans to buy homes to live in, the lower credit borrowers who would otherwise struggle to buy a home?

Well, they lost their homes.

Look at the spike on foreclosures in 2008.

Well, they lost their homes.

Look at the spike on foreclosures in 2008.

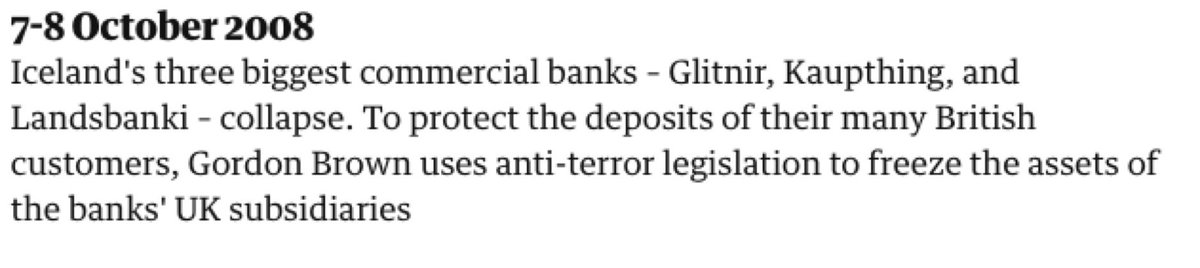

After Lehmans, Washington Mutual and Wachovia followed suit.

In the UK, lender Northern Rock did the same:

From the Guardian,

In the UK, lender Northern Rock did the same:

From the Guardian,

January 2008, the largest single-year drop in US home sales in 25 years.

February 2008, UK govt nationalises Northern Rock

March 2008, Bear Stearns “bought out” by JP Morgan

Sep 2008 US govt bails out Fannie Mae and Freddie Mac – two huge firms that had guaranteed

February 2008, UK govt nationalises Northern Rock

March 2008, Bear Stearns “bought out” by JP Morgan

Sep 2008 US govt bails out Fannie Mae and Freddie Mac – two huge firms that had guaranteed

guaranteed subprime mortgages.

Sep 2008, UK’s largest lender, HBOS, rescued by Lloyds TSB after a huge drop in share price.

Sep 2008, 2 more American banks collapse – Washington Mutual and Wachovia.

Now, govts were being dragged in, not just banks and homeowners:

Sep 2008, UK’s largest lender, HBOS, rescued by Lloyds TSB after a huge drop in share price.

Sep 2008, 2 more American banks collapse – Washington Mutual and Wachovia.

Now, govts were being dragged in, not just banks and homeowners:

Banks had to restrict lending, and this slowed down the economy, and unemployment increased.

The Guardian presents the timelime below:

The Guardian presents the timelime below:

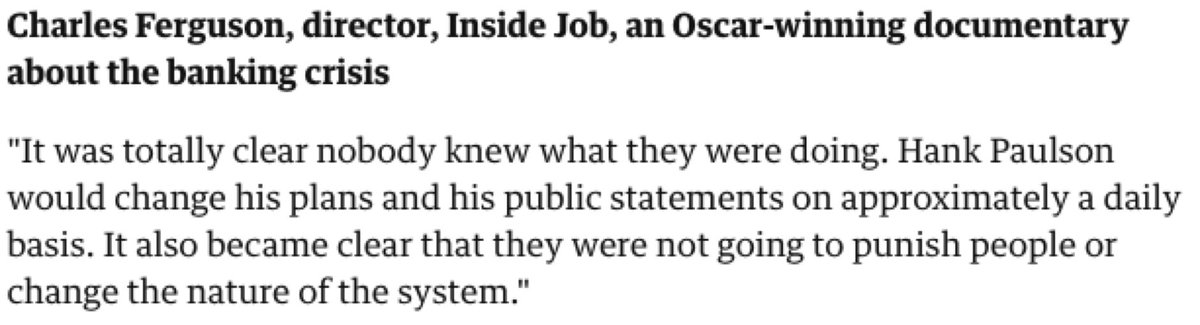

Anti-terror legislation is even used:

The whole British banking sector was at risk of collapse:

And, of course, people lost their jobs:

The blame game was in full flow:

Greece:

Greece is bailed out:

And things just got worse and worse…

So what can we learn from all this?

Impact of debt creation and derivatives

Debt is not without consequence.

Even though low levels of debt, can support the growth of businesses - we all know that, when there is money to be made by

So what can we learn from all this?

Impact of debt creation and derivatives

Debt is not without consequence.

Even though low levels of debt, can support the growth of businesses - we all know that, when there is money to be made by

creating debt, it will never end there. Human nature dictates, where private enterprises (banks) lend more money to make more profit, we will continue to issue debt.

When it reaches unsustainable levels, we all suffer.

When it reaches unsustainable levels, we all suffer.

Pursuit of short term profit, conflict of interest of credit rating agencies

The lending banks were happy to push out new debt because they could rapidly package into MBS and do the same all over again. It was easy money, and nobody paid any attention to the risk of delivering

The lending banks were happy to push out new debt because they could rapidly package into MBS and do the same all over again. It was easy money, and nobody paid any attention to the risk of delivering

delivering high levels of debt to low credit borrowers, backed by property that was falling in value.

Also, the creative investment bankers were happy to package this debt into securities and make short term profit. As long as they sold the risk to investors, it was no longer

Also, the creative investment bankers were happy to package this debt into securities and make short term profit. As long as they sold the risk to investors, it was no longer

their problem.

Ratings agencies were happy to give unrealistic ratings, maybe because they were being paid to do so. They still have a clear conflict of interest in the markets now.

Not understanding everything is connected

We learnt, the hard way, that foreclosures can

Ratings agencies were happy to give unrealistic ratings, maybe because they were being paid to do so. They still have a clear conflict of interest in the markets now.

Not understanding everything is connected

We learnt, the hard way, that foreclosures can

result in bank failures, unemployment, and recession. The causes were financial, but the impacts are very real, for real people.

Can it be repeated?

Well, the key causes were:

Can it be repeated?

Well, the key causes were:

1) Desire to make money by pumping out debt

2) Mechanism to repackage debt into derivatives

3) Proliferation of non-regulated derivatives in order to make profit

4) Regulators really having no clue of the impact of the complexity of financial markets

2) Mechanism to repackage debt into derivatives

3) Proliferation of non-regulated derivatives in order to make profit

4) Regulators really having no clue of the impact of the complexity of financial markets

Do you think any of these key factors have been eliminated now?

Connection with Islamic banking

The key causes were:

1) debt – debt (at interest is forbidden) – so in theory we cannot get into this mess but the reality is Islamic banks love debt and interest.

Connection with Islamic banking

The key causes were:

1) debt – debt (at interest is forbidden) – so in theory we cannot get into this mess but the reality is Islamic banks love debt and interest.

Up to 99% of their activities are priced at interest.

2) Derivatives – really they should not exist in any form. Where some derivatives can deliver benefit is in hedging and reducing risk - to deliver this we must focus more on better forms of insurance and protection

2) Derivatives – really they should not exist in any form. Where some derivatives can deliver benefit is in hedging and reducing risk - to deliver this we must focus more on better forms of insurance and protection

3) Profit before everything – In theory we should be earning profit as long as it not breaking a larger obligation. These can include no harm to people or the community, the environment, and so on.

In theory, we “could” say that adherence to Islamic principles would has avoided

In theory, we “could” say that adherence to Islamic principles would has avoided

the direct contributors of this crisis.

However, in reality, Islamic finance, as practiced, is dominated by debt (99% of everything Islamic banks do is priced at interest – this means this is debt (at interest)).

Also, we definitely execute derivatives in many areas –

However, in reality, Islamic finance, as practiced, is dominated by debt (99% of everything Islamic banks do is priced at interest – this means this is debt (at interest)).

Also, we definitely execute derivatives in many areas –

this includes Sukuk (every single Sukuk in existence has derivatives built into it), and investments too. And profit rate swaps to hedge profit risk which is interest rate risk

And we have failed to develop proper insurance and protection products – instead we deliver

And we have failed to develop proper insurance and protection products – instead we deliver

Takaful as a poor mimic to conventional insurance

And profit before everything – we do all the above in the name of profit. So, clearly we are failing here too

I firmly believe the theory of our system is incredibly powerful – yet we consistently fail to put any of this into

And profit before everything – we do all the above in the name of profit. So, clearly we are failing here too

I firmly believe the theory of our system is incredibly powerful – yet we consistently fail to put any of this into

practice.

We love debt, we love interest, we use derivatives in every sector, and so the only reason we avoided being hurt (that much) in the crash is because the economies where Islamic banking operates were not developed enough (in terms of financial products and

We love debt, we love interest, we use derivatives in every sector, and so the only reason we avoided being hurt (that much) in the crash is because the economies where Islamic banking operates were not developed enough (in terms of financial products and

proliferation of debt) to be dragged into it.

Give us a decade or more, and we will be getting there.

If you believe we escaped because of Islamic banking, you must educate yourself.

Just because we like to believe something does not mean it is true.

Give us a decade or more, and we will be getting there.

If you believe we escaped because of Islamic banking, you must educate yourself.

Just because we like to believe something does not mean it is true.

In fact, this delusion of ours has only served to give extra impetus to an industry that has wholly lost its way, and is disconnected to the real intention and power of our faith.

END THREAD (if you got this far!)

END THREAD (if you got this far!)

unroll @threadreaderapp

unroll please @threadreaderapp