On 8/05/2016 Sunday Times exposed that Lloyds were targeting non-sophisticated customers with excessive & undisclosed FX charges. I made multiple whistleblower disclosures on this subject when at LBG & escalated to @fca @APPGbanking @AWhistleblowing thetimes.co.uk/article/reveal…

It's important that IRHP victims and whistleblowers as well as FX Victims read this entire thread. You will understand why at the end.

In the article, reviews & investigations were promised. However, internal @TheFCA documents reveal that Lloyds, the FCA & Andrew Bailey whilst at Bank of England, instead colluded to engage in a hunt for the whistleblower that had spoken to the Times, & failed to investigate LBG

The future Governor of the Bank of England engaged in the unlawful hunt for the identity of a whistleblower. It makes it quite clear why Bailey and the FCA were so lenient on Jes Staley doesn't it. They believed it was me. I was actually busy at the time taking the matter to CoLP

In 2016 @CityPolice said by email to me that the criminal investigation that they were preparing to launch regarding these mark ups was prevented by FCA, who told them they'd taken no action in 2015. This despite FCA claiming Spot FX was unregulated & they had no scope for fraud

LBG Policy actually stated that "In highly competitive markets where clients are sophisticated, highly price sensitive, AV may not be charged. Where AV is charged, for smaller, less sophisticated customers, AV is limited to a set level." (3.3!) (AV = 'Added Value (Mark Ups))

This despite LBG advertising, as you can clearly see here, all FX Spot and Forwards to ALL customers at this time as having 'No Charge'. And let's be clear, a Mark Up is a charge, cost, fee, commission etc. levied against that customer entirely due to the transaction.

For the record, the policy states that LBG sales persons can take 'up to' 1.92% on FX Spot transactions of even £5mio for non sophisticated customers, who are told there is 'no charge'. Thats a £96,000 charge for a transaction they will charge a sophisticated customer £0 for.

And it is a charge, fee, cost, commission etc. entirely as a result of the transaction. This claim by Horta Osorio as to a 'cost to cover' is nonsense. The cost to cover is the same for sophisticated customers as it is for non sophisticated. The transaction costs the same.

Lloyds & other banks will claim that for non-sophisticated customers they have to impart more time or effort, so there's a greater cost. NONSENSE. The only extra time or effort sales persons spent on non sophisticated customers was trying to sell them a product they didn't need

Lloyds & all banks assessed clients for sophistication but not by the formal criteria. Instead they assessed based on what the client knew about the product & the true price of the product. The less a client knew, the more they were fleeced. It's that simple.

Don't take my word for it though, this is the Plea agreement between Barclays and the NYDFS dated May 20th 2015. It's important for any FX and IRHP customer that you read these three pages from this agreement. dfs.ny.gov/docs/about/ea/…

What you read there is blueprint of sales practises deployed by EVERY bank & sales person. It's just that only Barclays had two sales persons stupid enough to have this conversation on an electronic chat. Barclays were fined $2.5bio and forced to plead guilty to criminal conduct.

Why is this important & why is this relevant to the Lloyds policy? Well, on this date, May 20th 2015, it essentially rendered the very practises detailed in Lloyds policy as criminal in the eyes of U.S Regulators & DoJ and for the same reasons.

This date also coincided with the FCA turning on me, going to extraordinary lengths to bury this policy and me along with it, even to the point of lying to my MP and intentionally prejudicing my Employment Tribunal. Why? Because it turns out, the FCA had approved the LBG Policy

This is extract of written witness statement of Matthew Lawrence, Head of SME's at LBG, produced for my Tribunal. In LBG defence of this policy, he confirms that the regulator (the FCA) has seen it & therefore approved it. The FCA had approved practises deemed criminal in the U.S

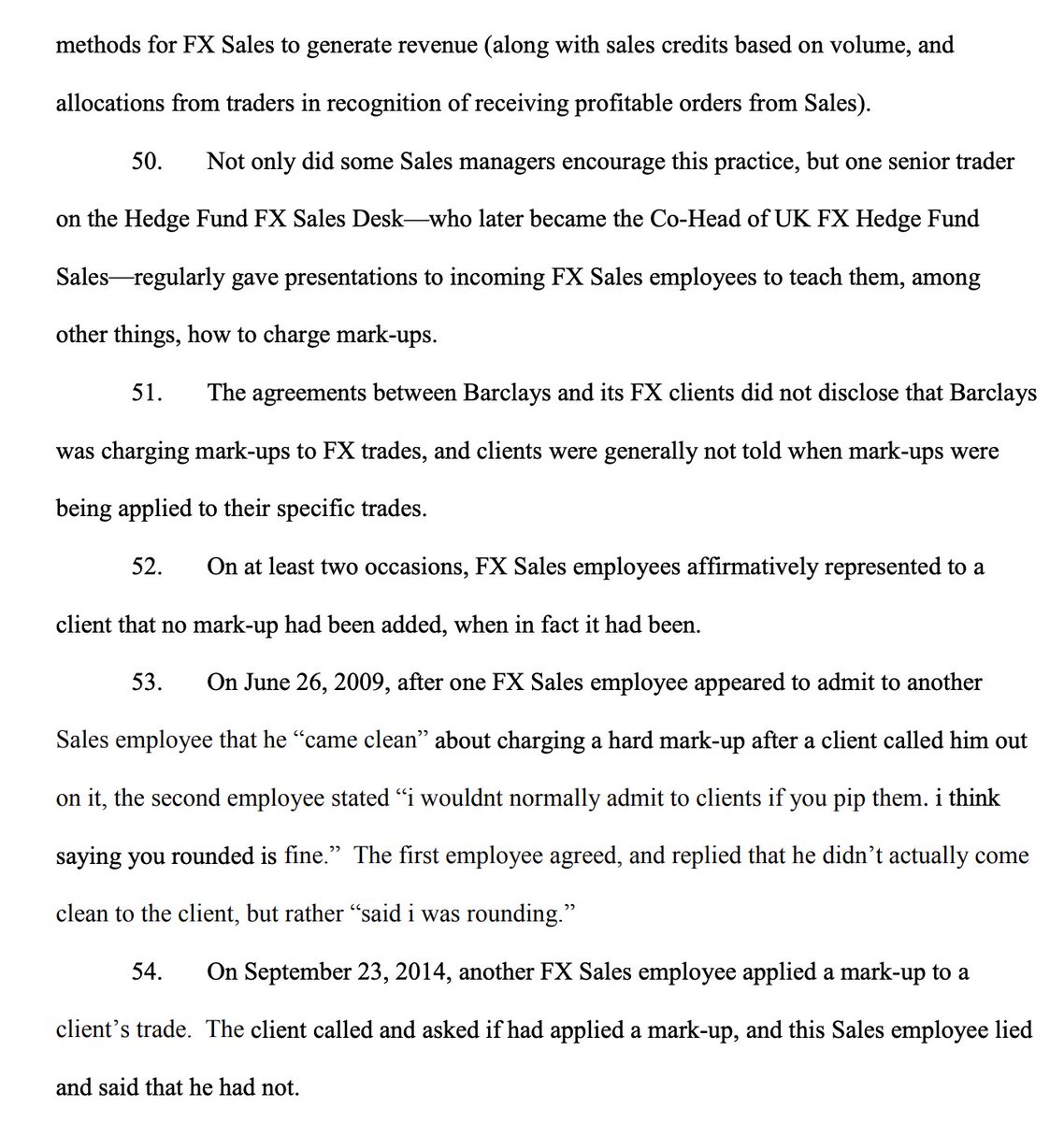

IMPORTANT: The LBG policy applies to sale of IRHP's also. So, according to wording of this policy, if you paid so much as one penny in AV (Mark Up), LBG are saying that you were non-sophisticated. You were therefore mis-sold, even if they tried to classify you as sophisticated