The @Accolade S-1 made for an interesting weekend read.

Not just as #coronavirus distraction, but for the window into a health tech solution that *could* be more aligned with the fundamental cost problem for employers and patients with private coverage (ahem...prices).

1/n

Not just as #coronavirus distraction, but for the window into a health tech solution that *could* be more aligned with the fundamental cost problem for employers and patients with private coverage (ahem...prices).

1/n

Prior digital health IPOs have seen firms pitching employers on savings through lower utilization, either via chronic disease mgmt (@Livongo) or convenient services that might reduce ER visits (@Teladoc, perhaps @OneMedical).

But for employers, price is the problem, not volume.

But for employers, price is the problem, not volume.

Accolade, in short, is a fairly high-touch service (tech + lots of call center staff) to help employees navigate the M.C. Escher painting that is American health care (find an affordable etc).

That service could potentially save $$ by nudging employees toward lower-cost options.

That service could potentially save $$ by nudging employees toward lower-cost options.

To the financials! The S-1 doesn’t have much operational data, but the overall picture looks a bit like a turnaround, w/ promising top-line momentum set against steep losses.

Revenue is up >40% YoY, but the company is losing $5M/mth on a GAAP basis, little changed from last year

Revenue is up >40% YoY, but the company is losing $5M/mth on a GAAP basis, little changed from last year

One surprise is how few clients the company signed until the last year. Accolade apparently had only 11 employer clients in early 2017, and then added just 4-5 logos per year until early 2019.

They now say they have jumped to 53 clients, perhaps helped by the @Humana partnership

They now say they have jumped to 53 clients, perhaps helped by the @Humana partnership

Strikingly, 45-50% of Accolade revenue comes from just three clients (Comcast, Lowe’s & United Airlines), w/ 25%-ish from Comcast alone

Note: Reports mention 60% / 35% for the Top 3 / Comcast, but this appears to refer to year-old #s; growth has since diluted concentration a bit

Note: Reports mention 60% / 35% for the Top 3 / Comcast, but this appears to refer to year-old #s; growth has since diluted concentration a bit

As context, Livongo went public w/ ~680 employer clients, but similar trailing revenue to Accolade.

Of course, Livongo engages / monetizes a small slice of a client’s employees (given low-ish chronic disease prevalence in the commercial population), so each client is worth less

Of course, Livongo engages / monetizes a small slice of a client’s employees (given low-ish chronic disease prevalence in the commercial population), so each client is worth less

Other metrics are a mixed bag. Gross margins run 35-40%, and Accolade is spending ~$2.5 – 3M a month on sales and marketing (both about the same as ONEM).

Seems to be decent bookings momentum, but these are expensive clients to acquire and serve.

Seems to be decent bookings momentum, but these are expensive clients to acquire and serve.

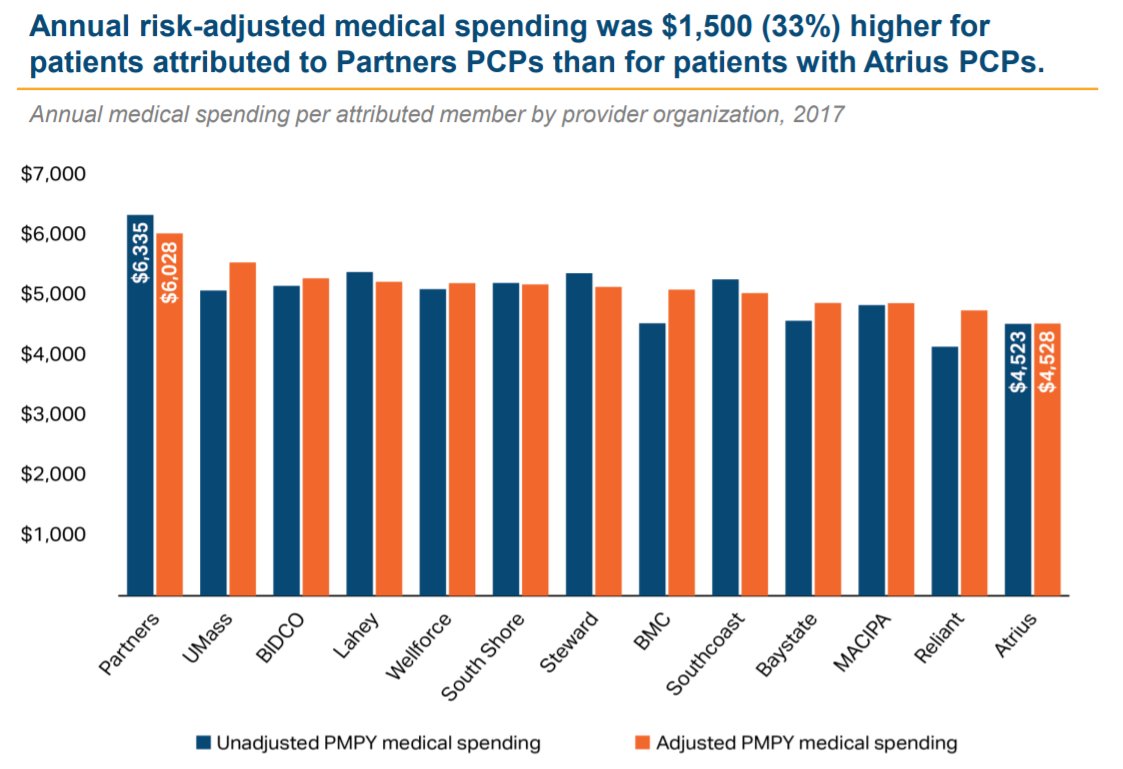

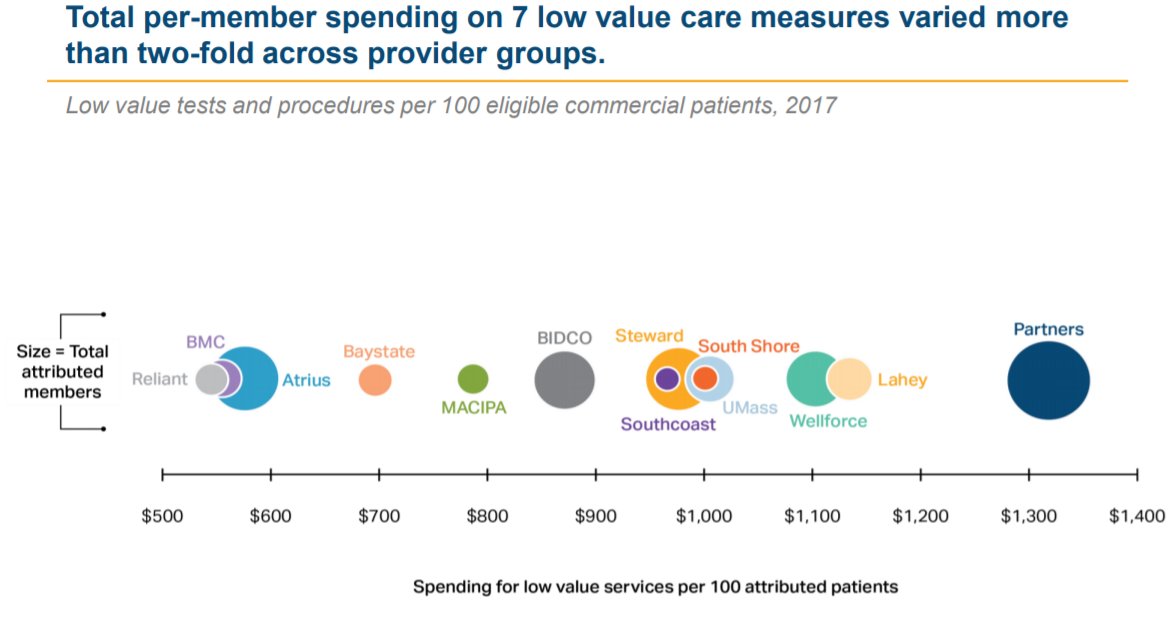

Where Accolade gets interesting (for me, in any case) is the data on hard dollar claim cost savings for employers, which seem to run about 6%, or ~$300 PMPY against a 2016 baseline.

That’s a gross #, which might be ~4% and $200 – 225 after netting out the cost of Accolade itself

That’s a gross #, which might be ~4% and $200 – 225 after netting out the cost of Accolade itself

Caution!! ...on that net number:

S-1 data seem to imply that clients may pay something like $75-90, but this could well be wrong. There are also hints that Comcast – also an investor in the company - may be paying materially more (perhaps as much as $150 PMPY)

S-1 data seem to imply that clients may pay something like $75-90, but this could well be wrong. There are also hints that Comcast – also an investor in the company - may be paying materially more (perhaps as much as $150 PMPY)

In any case, Aon estimates of (gross) employer savings suggest that 50-60% of the cost ↘️comes from outpatient professional claims (cheaper or avoidable specialist care), another 30% from lower drug $$ (prob generic switching) and the remainder from outpatient facility claims.

This all certainly fits with a thesis that, while employers may struggle to negotiate lower prices, there are material savings to be had simply by steering patients to better-value sites of service, or, data-permitting, to specialists less likely to kick off an expensive cascade.

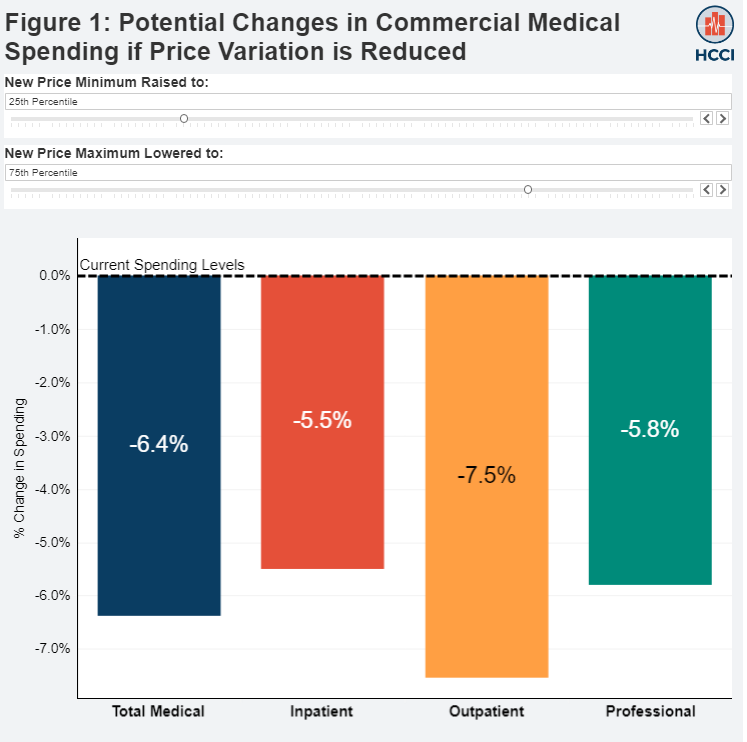

@HealthCostInst data, for example, shows a similar magnitude of savings if employees were able to avoid just the highest-priced providers - i.e. those above the 75th percentile of the price distribution for a particular service in a given market.

Also notable that Accolade’s 6% claim cost savings (gross) is much higher than the 3.5% that One Medical mentions in their S-1 (w/o much supporting analysis).

And, in the ONEM case, their own high prices (and referrals) offset the savings, so net employer savings seem unlikely.

And, in the ONEM case, their own high prices (and referrals) offset the savings, so net employer savings seem unlikely.

Livongo, in turn, does have credible data showing an $88 monthly cost savings *per participating diabetic.*

Significant, but if diabetes prevalence runs at ~5% for commercial lives, it probably equates to $50 – 60 PMPY (gross) across the employee base.

tandfonline.com/doi/full/10.10…

Significant, but if diabetes prevalence runs at ~5% for commercial lives, it probably equates to $50 – 60 PMPY (gross) across the employee base.

tandfonline.com/doi/full/10.10…

Net/net, Accolade seems to pair promising impact w/ rocky financials, which prompts three questions for me:

1) Why have insurers been so slow to build a similar navigation layer? After all, health plans have infamously low customer satisfaction/NPS, and this might help.

1) Why have insurers been so slow to build a similar navigation layer? After all, health plans have infamously low customer satisfaction/NPS, and this might help.

2) Since there is reason to think this approach can cut costs, what is the opportunity to build the same sort of steerage and nudges into primary care workflows, instead of adding a labor-intensive "navigation service" or an arguably duplicative "engagement" layer?

3) If primary care groups (or an MSO) can build this competency, could it be a lucrative place to take risk?

Capturing half of the $300 PMPY savings here could probably boost PCP revenue per attributed commercial member by 30 - 50%.

/n

Capturing half of the $300 PMPY savings here could probably boost PCP revenue per attributed commercial member by 30 - 50%.

/n

I should clarify: Loss rate refers to the period through Nov 2019. Accolade's FY closes at the end of Feb, and there is a clear "plan year" pattern, w/ ARR leveling up in Jan (presumably as new clients go live). So the Q they closed last week could materially shift the burn rate