,

15 tweets,

7 min read

Read on Twitter

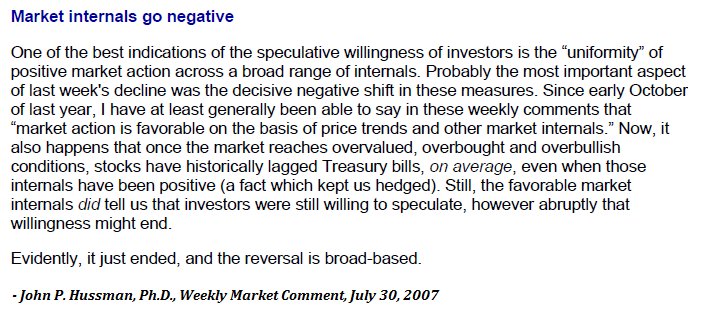

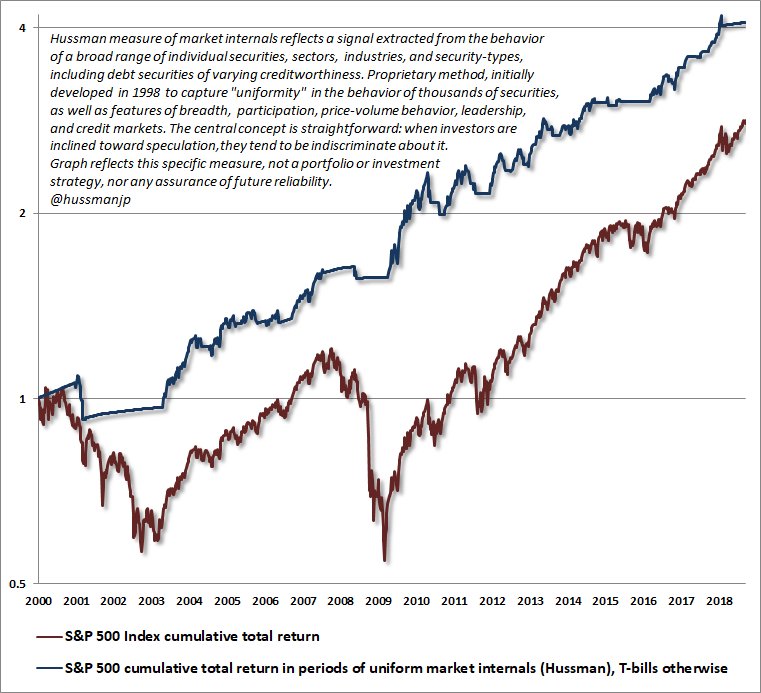

1/ Thread: A quick scrapbook of what I call "full-cycle" investing, *including my error in this cycle. First up, major peaks (2000, 07, 18) have a common feature: extreme valuation finally meets risk-aversion (which I gauge by deterioration in the uniformity of market internals).

2/ By contrast, major lows (1990, 02-03, 08-09) feature a material retreat in valuations, joined by an early improvement in market internals. This doesn't require valuations to reach or break historical norms. I've noted this shift after every bear market plunge in 30+ yrs.

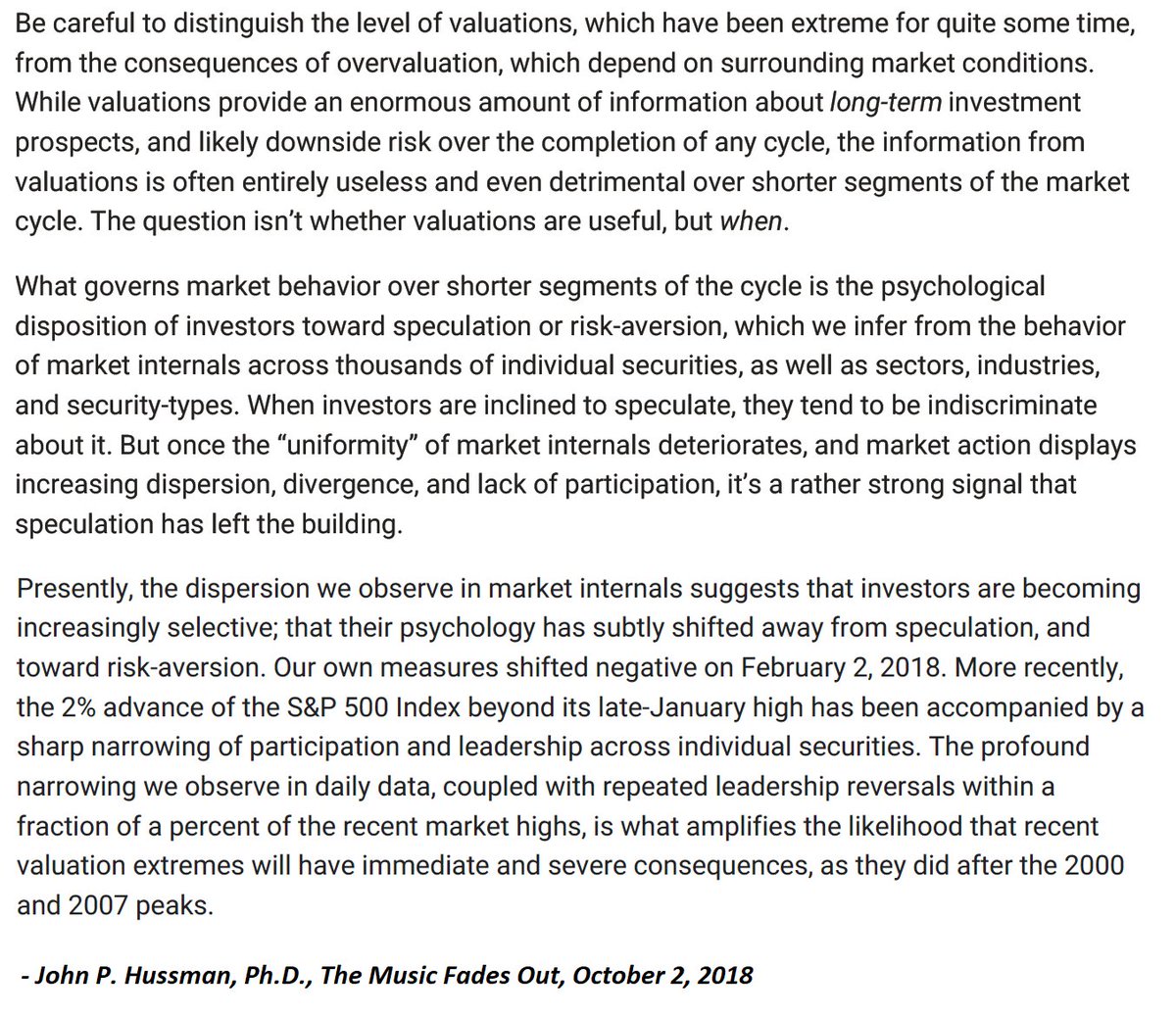

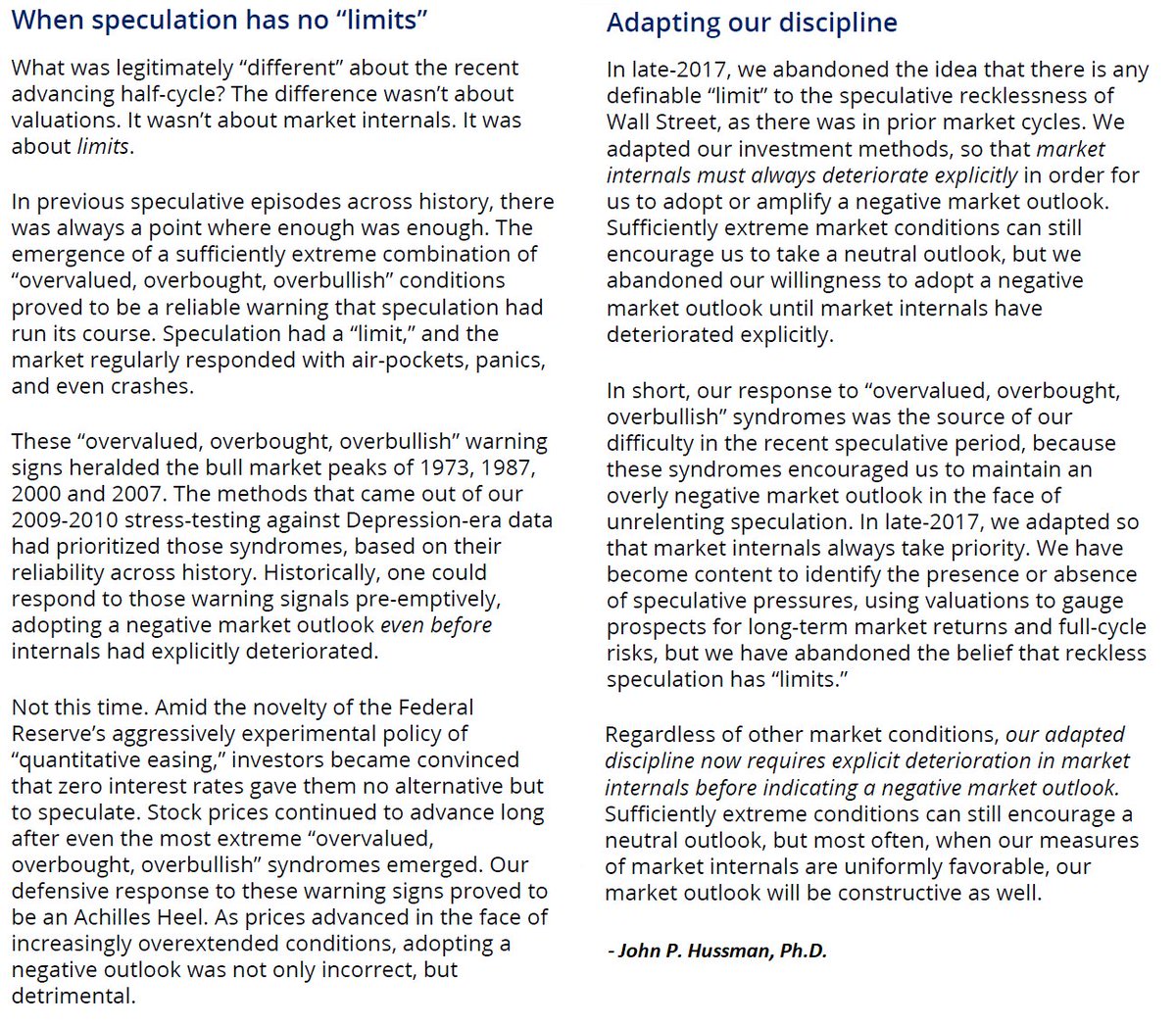

3/ Now my error in the recent half-cycle. My response to historically reliable "overvalued, overbought, overbullish" syndromes was an Achilles Heel in the face of ZIRP. The error was to believe the speculative recklessness of Wall Street had a "limit," as it had in other cycles.

4/ Understand the lesson. Both valuations and market internals navigated this cycle beautifully. The lesson was that ZIRP caused investors to lose their minds, so one could not take a preemptive bearish outlook until internals deteriorated (signaling increasing risk-aversion).

5/ So what now? Well, first, I continue to believe that the recent half-cycle was one of the three most speculative episodes in U.S. financial history. A 15% decline off the extreme is not going to make that all better ...

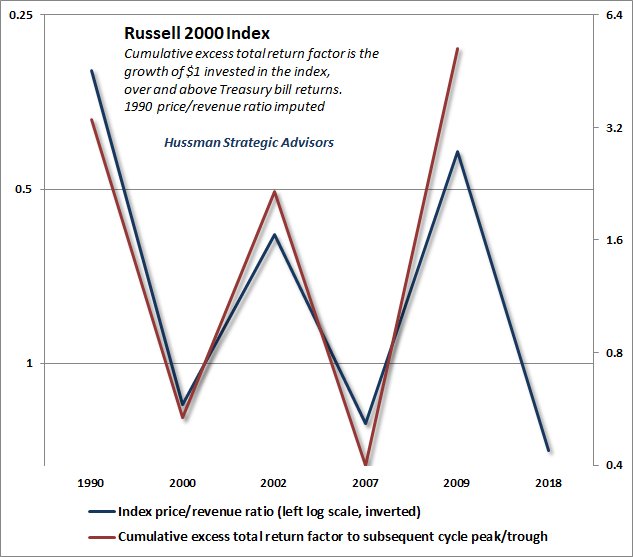

6/ From a valuation standpoint, given the extremes we observed in this cycle, a rather run-of-the-mill cycle completion would likely involve an overall loss of about -60% in the S&P 500, without even breaking norms that were breached in every cycle except the 2000-2002 collapse.

7/ Again however, a return to historical valuation norms isn't a requirement. Yes, I think we'll probably approach or break 1000 on the S&P 500 over the completion of this cycle, but the key, if you go back earlier in this thread, is to be mindful of speculation vs risk-aversion.

8/ So from a birds-eye view, what matters is the combination of valuations and market internals, which tell us where we are in the overall cycle. Within that, shorter-term technical factors may be useful. For example, Sep 20, 2018, had more warnings than any point since 3/24/00.

9/ Likewise, the completion of any given market cycle typically involves periods of extreme compression that are relieved by explosive clearing rallies that I've often called "fast, furious, and prone-to-failure" much like the one we anticipated last week. These aren't "bottoms."

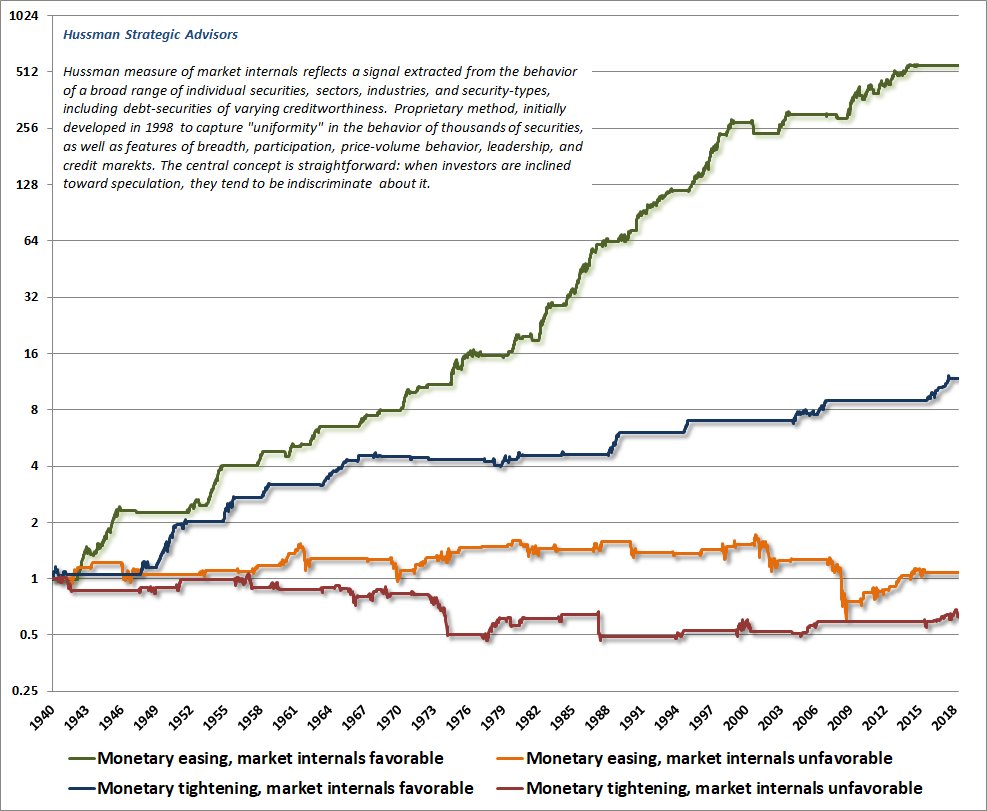

10/ The other thing we're going to get ... eventually ... is Fed easing. Aside from the likelihood of an obligatory knee-jerk advance, this will most likely be a bad thing. Early easings are almost always responses to abrupt economic deterioration.

11/ So remember that easy money is very effective in *amplifying the speculative inclinations of investors, but it's still important to gauge that by the uniformity of market internals. In a risk-averse environment, easy money doesn't help, because liquidity is a desirable asset.

12/ Oh, and it bears repeating that not all valuation measures are created equal. Before you listen to anyone waving this measure or that around, ask whether the measure is well-correlated with actual subsequent market returns. If not, run.

13/ I know people get very upset when I talk about a likely -60% loss in the S&P 500 over the completion of this cycle. It seems preposterous. The problem is that the market loss over the completion of any cycle is related to the level of overvaluation it reached at the peak.

14/ ... and it's those extremes that result in seemingly preposterous loss projections. Again, I'm very open about the error of responding to "overvalued, overbought, overbullish" syndromes before internals broke (see 3/), but don't imagine that makes risks any smaller here.

15/ To sum up, good valuation measures provide strong information on long-term (10-12 yr) returns and full-cycle risks. Intermediate segments of the cycle are best gauged by internal uniformity (speculative/risk-averse psychology), and technicals sometimes inform short horizons.