,

37 tweets,

15 min read

Read on Twitter

News broke 3 days ago that the NASS has passed the National Housing Bill 2018. Meaning it's just waiting for presidential assent. A few observers have given their views on the new law. This is a thread to break down the law and explore its implication.

A THREAD

#NHFAct2018

A THREAD

#NHFAct2018

The National Housing Fund (Establishment Act) 2018 is a bill to repeal the NHF Act 1992 (now NHF Act Cap 2004). The bill sponsored by Senator Ahmed Lawan has the primary aim of mobilizing additional funding for the financing of housing projects in Nigeria. #NHF2018

The highlights of the bill are:

- Levy of 2.5% on each bag of cement

- Contribution of 2.5% of monthly income of all employees (Public and Private Sector) and self-employed earning from minimum wage and above at an interest rate of 2% p.a.

#NHF2018

- Levy of 2.5% on each bag of cement

- Contribution of 2.5% of monthly income of all employees (Public and Private Sector) and self-employed earning from minimum wage and above at an interest rate of 2% p.a.

#NHF2018

- Investment of 10% of PBT of every commercial bank, merchant bank, insurance company and PFA in the fund at the rate of 1% above interest rate payable on current accounts by banks.

- The FG will make “adequate financial contribution & grants” to the fund as it deem fit. #NGF2018

- The FG will make “adequate financial contribution & grants” to the fund as it deem fit. #NGF2018

- An employer (public and private) is expected to make the monthly deductions and remit to the fund through the Federal Mortgage Bank of Nigeria (FMBN)

- The CBN shall collect the investment amounts from Commercial and Merchant banks at the end of each year.

#NHF2018

- The CBN shall collect the investment amounts from Commercial and Merchant banks at the end of each year.

#NHF2018

The National Insurance Commission (NAICOM) shall collect for Insurance Companies. While the National Pension Commission (PENCOM) has the responsibility of collecting for PFA’s. FIRS will collect from manufacturers and importers the 2.5% levy on cement. #NHF2018

- There are stringent and punitive sanctions for individuals or body corporate who fails to collect and remit contribution and levies ranging from losing operating licenses to fines up to N100 million for corporates and N10 million for individuals. #NHF2018

- Any contributor who does not have any outstanding loans and has attained 60 years of age or 35 years of service is entitled to a refund of contribution at an interest rate of 2% p.a. within 3 months of application. #NHF2018

Who manages the fund?

- The Federal Mortgage bank of Nigeria (FMBN).

How?

- Through lending to PMB (Primary Mortgage banks)

Who can access the loan?

- Individual Contributors

- Developers

#NHF2018

- The Federal Mortgage bank of Nigeria (FMBN).

How?

- Through lending to PMB (Primary Mortgage banks)

Who can access the loan?

- Individual Contributors

- Developers

#NHF2018

How do contributors access the fund and is it limited to contributions?

- A contributor interested in the NHF loan applies through a PMB, who packages & forwards the application to FMBN. The loan amount is determined by applicant’s affordability & not 2.5% contribution. #NHF2018

- A contributor interested in the NHF loan applies through a PMB, who packages & forwards the application to FMBN. The loan amount is determined by applicant’s affordability & not 2.5% contribution. #NHF2018

Is participation Mandatory?

- Yes it is mandatory for everybody earning any amount from minimum wage and above. Whether you are a public worker, a private worker or even self employed. As long as you are earning any amt from minimum wage, you're mandated to contribute. #NHF2018

- Yes it is mandatory for everybody earning any amount from minimum wage and above. Whether you are a public worker, a private worker or even self employed. As long as you are earning any amt from minimum wage, you're mandated to contribute. #NHF2018

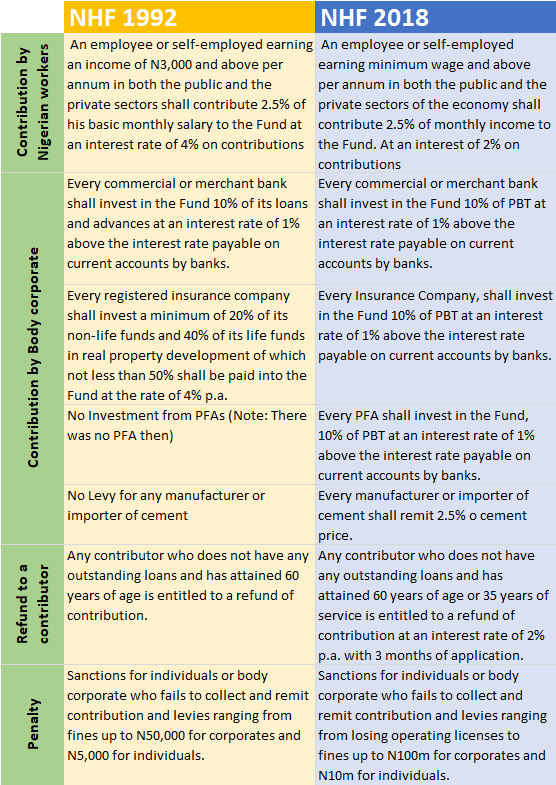

What is the difference between the NHF Act 1992 (2004) and the NHF Bill 2018?

See attached chart.

#NHF2018

See attached chart.

#NHF2018

If the NHF Act has been in existence since 1992 and the provisions of the law was mandatory, how come it was not fully implemented?

There were several reasons why the scheme was not fully implement. I will explore some of them in the next few tweets.

#NHF2018

There were several reasons why the scheme was not fully implement. I will explore some of them in the next few tweets.

#NHF2018

1. Stakeholders did not meet up to their obligations. As at 2013, the CBN had not even paid up its 30% equity stake in FMBN. Banks and insurance companies required to invest in the scheme defaulted. The CBN that was required by law to remit investment couldn't care less. #NHF2018

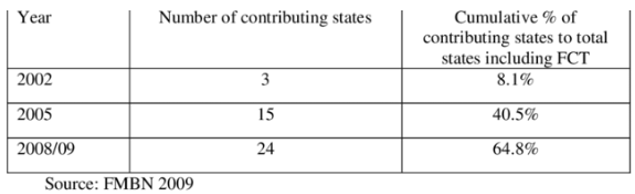

2. Many States didn’t start remitting until many years after the law took effect. And they also defaulted. As at 2009, only 24 States were contributing. It is difficult to enforce a law which the drafters themselves (government) are not even obeying. #NHF2018

3. Many employees through their labour unions simply opted out of the scheme due largely to complaints regarding alleged poor record keeping by the Federal Mortgage Bank of Nigeria (FMBN) and cumbersome bureaucratic bottlenecks to obtain loans. #NHF2018

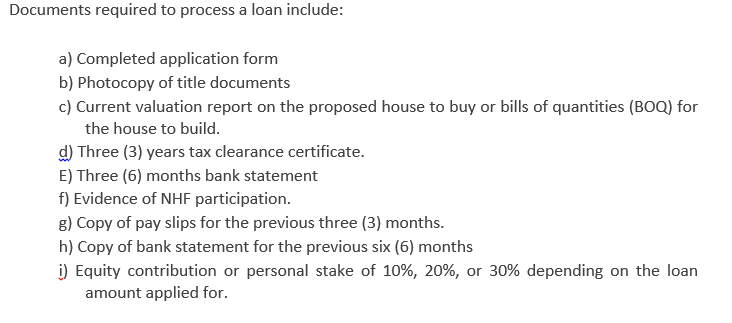

4. The cost of construction and real estate development kept increasing beyond the capacity of workers to afford. The maximum loan amt you can collect on the NHF presently is N15 Million with equity contribution ranging from 10% – 30% depending on the amount applied for. #NHF2018

5. Challenges in enforcement of the law. For instance, the law hasn't been able to figure out how to get the self-employed to contribute. The law expects them to voluntarily contribute. Besides, it's difficult to enforce a law that d enforcers themselves are defaulting. #NHF2018

6. Finance. The pool of funds was insufficient to make any significant impact. Between 1992 – 2009 (a period of 17 years), the fund was only able to mobilize about N70 Billion of which it was able to loan out about N20 Billion mostly to developers. #NHF2018

7. The Land Use Act made the process of perfecting title to landed property burdensome, slow and costly. The NHF doesn't fund purchase of land. It only funds construction and renovation of buildings of which you MUST have title documents proving ownership. #NHF2018

8. Political considerations: The States were more inclined to implement their housing projects than implement the NHF because such projects had greater political capital to them than the NHF which was seen as the arm in which the FG executes its own housing projects. #NHF2018

What has the NHF achieved since inception?

According to FMBN MD Ahmed Dangiwa, since inception (27 years ago), the NHF has disbursed a total of N193.4 Billion loans to a total of about 23,000 beneficiaries and refunds to about 230,000 retirees. #NHF2018

sunnewsonline.com/fmbn-disburses…

According to FMBN MD Ahmed Dangiwa, since inception (27 years ago), the NHF has disbursed a total of N193.4 Billion loans to a total of about 23,000 beneficiaries and refunds to about 230,000 retirees. #NHF2018

sunnewsonline.com/fmbn-disburses…

While a significant part of the fund has been accessed by developers resulting in thousands of housing units constructed, it must be noted however that the fund has been most active in recent years due to increased collaborations with Labour, States and the OPS. #NHF2018

Now let's consider the challenges with the new NHF 2018 just passed.

@PwC Nigeria posted 10 reasons why the bill in its present form is a bad idea. I will like to highlight 7 of them for specific reference. #NHF2018

pwcnigeria.typepad.com/tax_matters_ni…

@PwC Nigeria posted 10 reasons why the bill in its present form is a bad idea. I will like to highlight 7 of them for specific reference. #NHF2018

pwcnigeria.typepad.com/tax_matters_ni…

- The contribution is regressive as it taxes the poor more than the rich. For instance, minimum wage earners will pay about 250% of their personal income tax (PAYE) to the NHF monthly. #NHF2018

- Making all employers liable to deduct and remit the contributions monthly (without a threshold) will worsen the ease of doing business and Nigeria's paying taxes ranking. #NHF2018

- Cost of borrowing will increase as banks are required to invest a minimum of 10% of their profits at 1% above current deposit rates. #NHF2018

- Increasing the tax burden without addressing other fundamental issues like land regulation, REITS framework etc is not consistent with the 2017 National Tax Policy

- Imposition of the 2.5% levy on cement is a tax on property dev which will make housing less affordable

#NHF2018

- Imposition of the 2.5% levy on cement is a tax on property dev which will make housing less affordable

#NHF2018

- The requirement for PFAs to invest pension funds in the scheme means less returns for pension contributors which will erode value for pensioners. #NHF2018

- The return of 2% per annum for contributors withdrawing after attaining 60 years of age or 35 years of service is far below inflation rate and grossly insufficient to compensate for time value of money. #NHF2018

My Thoughts:

This bill is clearly an attempt by the NASS to mobilize more funding for the NHF which in 27 years has not been able to mobilize much in terms of finance. So clearly that is understood. However, the challenges of housing, goes beyond just funding. #NHF2018

This bill is clearly an attempt by the NASS to mobilize more funding for the NHF which in 27 years has not been able to mobilize much in terms of finance. So clearly that is understood. However, the challenges of housing, goes beyond just funding. #NHF2018

There are systemic challenges around property rights for example that needs to be resolved. If this is not fixed, contributors cannot access loans and the funds will just be another big government effort to trap people’s money until they retire or worse die. #NHF2018

Secondly, I am of the opinion that emphasis should be more about strengthening existing laws to ensure that banks and insurance companies comply with the law as it currently is than enacting another law that will largely be defaulted. #NHF2018

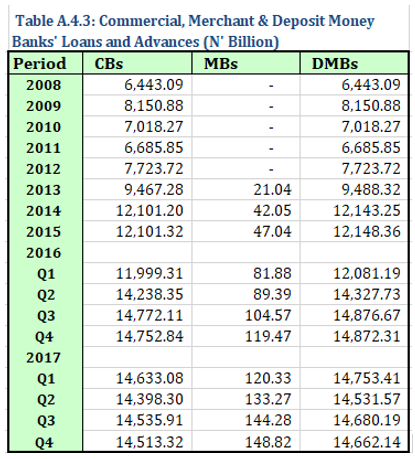

For instance, the CBN, & NAICOM statistics indicated that between 2008 and 2017, total loans and advances by deposit money banks and non-life and life funds from insurance companies amounted to over N100 trillion. Imagine the impact collecting 10% of that amt wld have? #NHF2018

At 10% investment of their loan advances and insurance with the NHF, about N10 trillion shd have been invested in the fund by the banks and insurance companies over the period. Can we strive to achieve this first before increasing the burden of contribution on workers? #NHF2018

It's telling that the fund has refunded more people in its lifetime than it has granted loans to contributors. Without an integrated solution, plan and strategy in place, (which must also include increased funding), we would just be increasingly the burden on workers. #NHF2018

In trying to solve one problem (the lack of adequate funding), we should not create additional problems for the Nigeria worker and corporate entities. This bill should not be signed in its present form. The President should send it back to the NASS for review. #NHF2018