,

14 tweets,

4 min read

Read on Twitter

After having criticized the IMF for its lax "surveillance" of surplus countries, I want to join @adam_tooze in commending the IMF for its latest report on Germany - and to join the IMF in calling for Germany to implement policies to "restore" household purchasing power

(1/x)

(1/x)

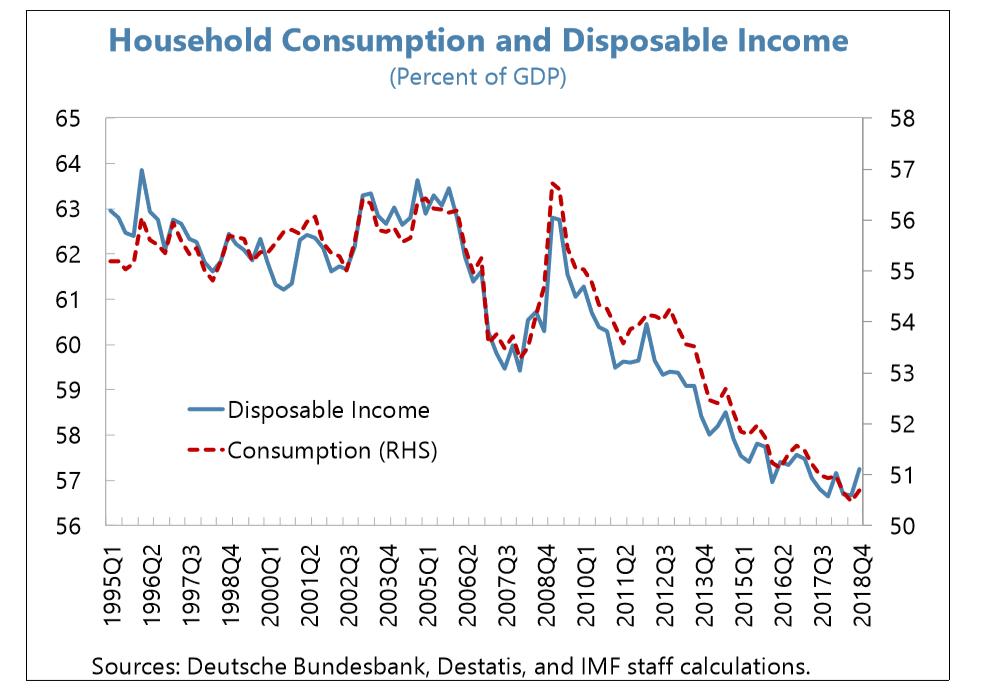

this is a key point "Bringing household disposable income to GDP ratio back to its 2005 level (63 percent) through wage growth alone would require nominal wage growth to exceed annual nominal GDP growth by around 1.5 percentage points each year for over a decade. "

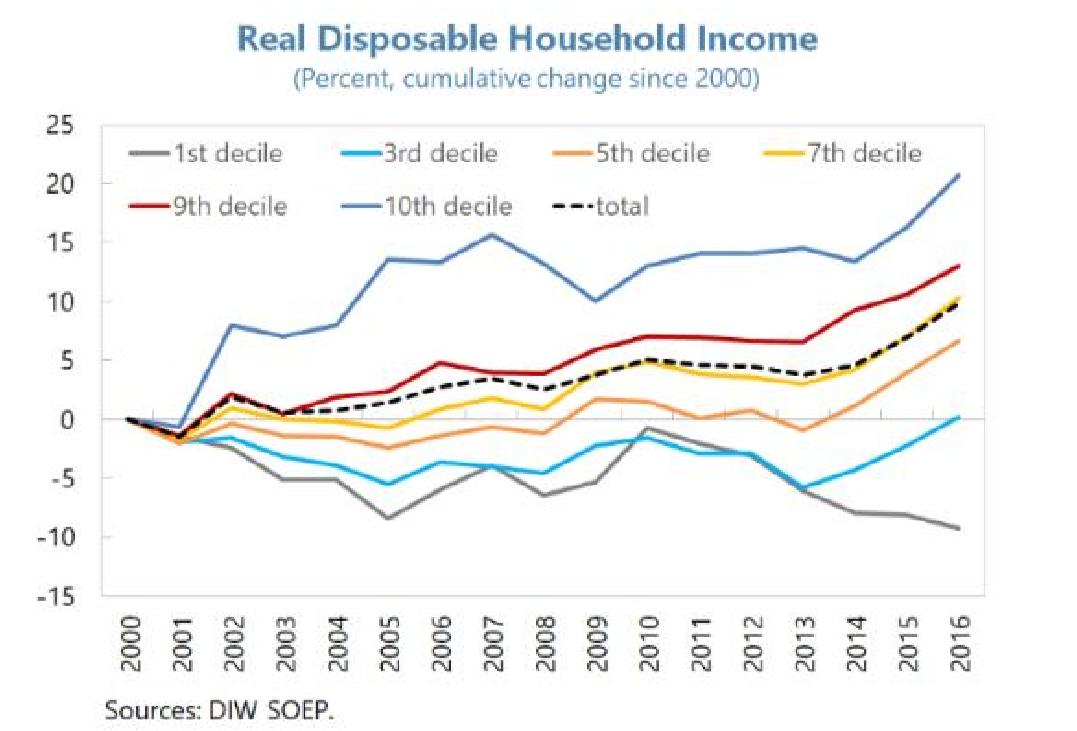

There is a lot to admire about the German model (its focus on manufacturing has helped limit regional in equalities for example). But it hasn't done all that great a job in delivering broad income growth. As in other Western countries, prosperity hasn't been widely shared.

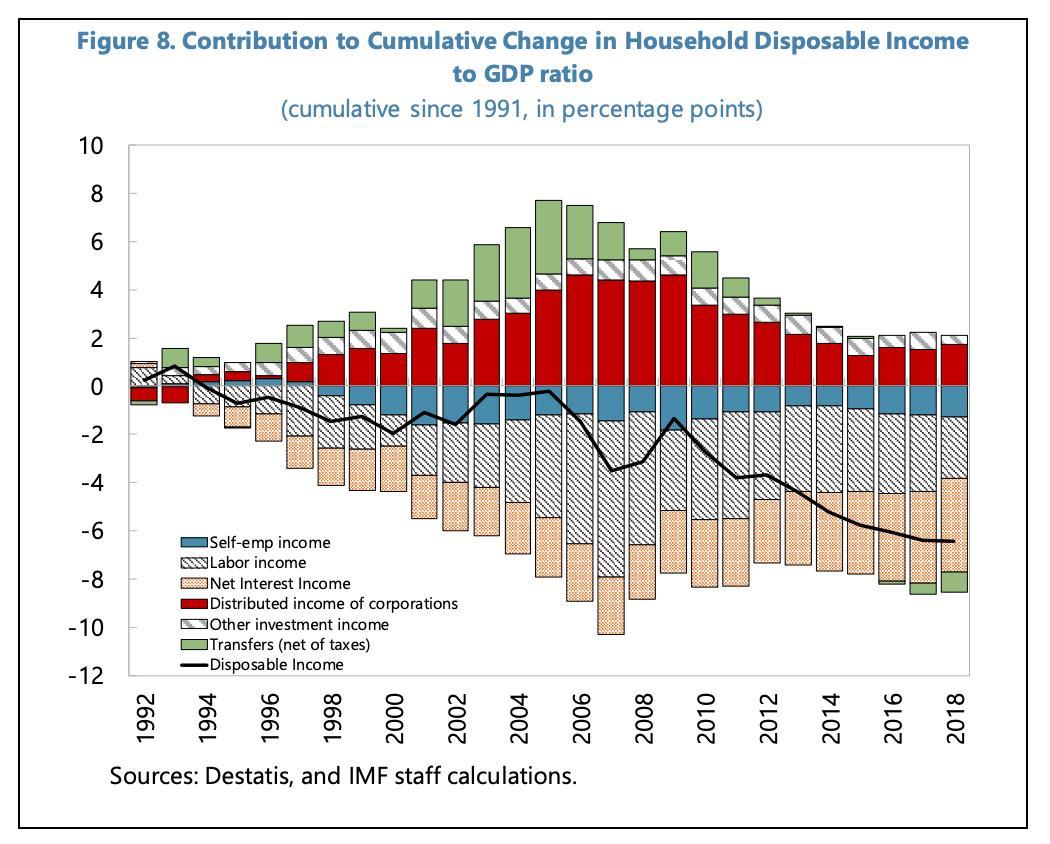

As the IMF notes, the tax system puts a large burden on lower middle income tax payers (and falling transfers have contributed to the fall in household income to GDP (see the green bar in the first chart)

(4/x)

(4/x)

It isn't as bad as the US (with its favorable treatment of offshore income which turned firms into savings vehicles), but Germany's tax system also encouraged retained earnings

(5/x)

(5/x)

"High corporate savings, therefore, partly reflect savings of wealthy German households accumulated within firms due to preferential tax treatment"

(distributed profits are taxed at a higher rate I think)

looking forward to the forthcoming IMF paper on this

(6/x)

(distributed profits are taxed at a higher rate I think)

looking forward to the forthcoming IMF paper on this

(6/x)

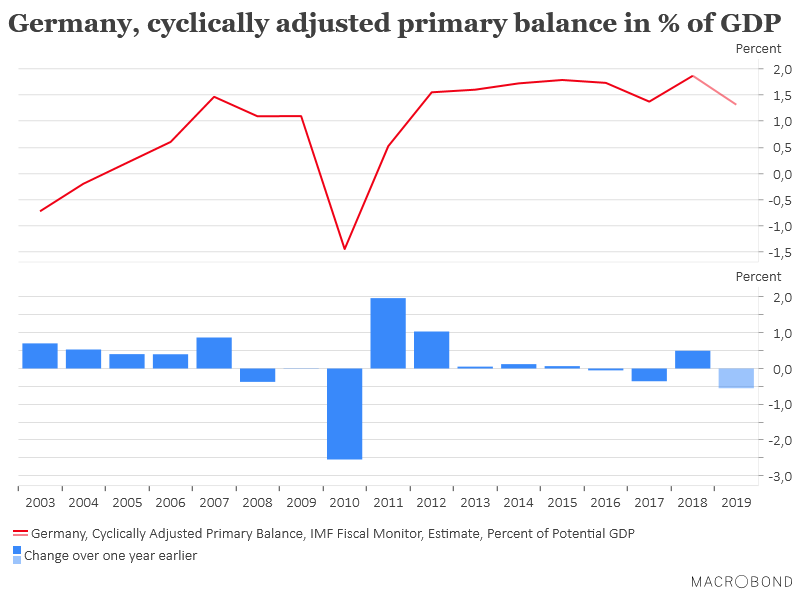

The IMF wants Germany to run a structural fiscal deficit of 0.5 pp of GDP, which seems to translate into a headline fiscal balance of around zero right now -

Directionally, that's the right advice but it is still fairly timid

(7/x)

Directionally, that's the right advice but it is still fairly timid

(7/x)

a flat general government balance and rising GDP means that government debt would still fall relative to GDP (and relative to global reserve demand).

The IMF's advice wouldn't solve the problem the FT recently highlighted

(8/x)

ft.com/content/eeadb2…

The IMF's advice wouldn't solve the problem the FT recently highlighted

(8/x)

ft.com/content/eeadb2…

There is one technical feature of Germany's model that I think warrants more scrutiny. on its current trajectory (1% of GDP fiscal surpluses forever -- net public debt falls by 15 pp, but net external assets rise by 20 pp of GDP (to 2024)

(2018 = third column in table)

(9/x)

(2018 = third column in table)

(9/x)

The 35 pp of GDP swing in Germany's net international investment position has all come from the swing in portfolio assets (reserve asset issues usually provide portfolio assets to the world, as the US does ... )

(table is 2010 to 2018)

(10/x)

(table is 2010 to 2018)

(10/x)

e.g. the current account surplus isn't just financing German direct investment abroad -- German institutions are in aggregate taking increasing risks abroad (lifers, pension funds, savings banks, etc) rather than financing investment at home

(11/x)

(11/x)

would love to see more analysis of where the risk lies. have a better sense of what kind of risks Japanese institutions have been taking over the last 5 years than the kind of risk German institutions now run ...

(12/x)

(12/x)

The IMF has sometimes treated an external surplus as a sign of a well-run economy, one that isn't posing any risks to the world. The IMF didn't make that mistake with Germany this year.

(13/x)

imf.org/en/Publication…

(13/x)

imf.org/en/Publication…

Now I will await an equally hard hitting and in depth analysis of the sources of the excessive external surpluses of the Netherlands and Singapore (and a few others)!

(14/14)

(14/14)