,

18 tweets,

5 min read

Read on Twitter

Happy Monday - this week is all about China data dump (retail sales, FAI, IP, monetary) & Malaysia CPI & GDP. In the US, we got CPI, retail sales,IP & housing starts. In the Eurozone, German & French CPI final, GDP p & ZEW Survey.

All to confirm what we know - global slowdown👈🏻

All to confirm what we know - global slowdown👈🏻

Where are we? We're here👇🏻:

a) Global manufacturing slowdown ON (US ISM manu less exceptional & more down to earth)

b) China PMI in contraction, PPI feeling deflated, imports & profits declining

c) Asia growth weak

c) China fixes CNY weaker

c) CBs in Asia cut & let FX follow CNY

a) Global manufacturing slowdown ON (US ISM manu less exceptional & more down to earth)

b) China PMI in contraction, PPI feeling deflated, imports & profits declining

c) Asia growth weak

c) China fixes CNY weaker

c) CBs in Asia cut & let FX follow CNY

One short nap & we're back to January 2007 (okay, a bit higher, like 3% higher if you invested 100 so today is 103, not account for FX, CPI, dividend, etc).

Shanghai Composite on Aug 2019 2,794

Index on January 2007 👉🏻👉🏻👉🏻2,716

Shanghai Composite on Aug 2019 2,794

Index on January 2007 👉🏻👉🏻👉🏻2,716

China aggregate financing rose CNY1,010bn lower than the 1625bn expected & less than half of last month's high of 2262bn 😬. So liquidity is pretty tight in China & confirms huge divergence in funding for different types of companies/banks. Access is an issue for those that need.

New loan is 1060bn vs 1663.6bn in June and much less than the 1275bn expected. Risk aversion is is prevalent & so we're in the usual situation of those that need liquidity (smaller, riskier, etc) do not get it & so ACCESS is a challenge.

Starting H2 w/ PPI deflation, weak credit

Starting H2 w/ PPI deflation, weak credit

😯Details are not pretty - loans are down & bonds are up but mostly local government special bonds 👇🏻👇🏻👇🏻

If you look at this, then you can see where the growth will come from in China in H2 (government driven projects/sectors). Meanwhile, the decline of new loans means that private sector weakness persists into H2 2019 & you knew this from the PPI, industrial profits & PMI figures.

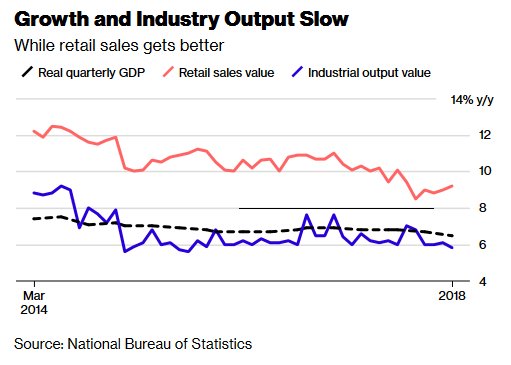

Told you. Not pretty. Huge payback from June as July data sags across the board:

Retail sales down to 7.6%; IP down to 4.8% and FAI down to 5.7%

ALL WORSE THAN EXPECTATIONS & PAST. But you knew that right from weak PMI, deflated PPI & contracting profits.

Retail sales down to 7.6%; IP down to 4.8% and FAI down to 5.7%

ALL WORSE THAN EXPECTATIONS & PAST. But you knew that right from weak PMI, deflated PPI & contracting profits.

Details of retail sales - note that June data was unusually strong & that July is a payback of that so not as bad as it looks. Trend is consumers tightening.

What's down? Autos, Communication appliance, petrol, household electronics, jewelry, clothing.

BASICALLY CONSUMER GOODS

What's down? Autos, Communication appliance, petrol, household electronics, jewelry, clothing.

BASICALLY CONSUMER GOODS

So durables are down & consumer goods are down & the only things that are up are ALCOHOL, BEVERAGES, AND FOOD. In other words, essentials.

Do you know what that means??? Cutting back discretionary & tightening purse strings 🥶.

Do you know what that means??? Cutting back discretionary & tightening purse strings 🥶.

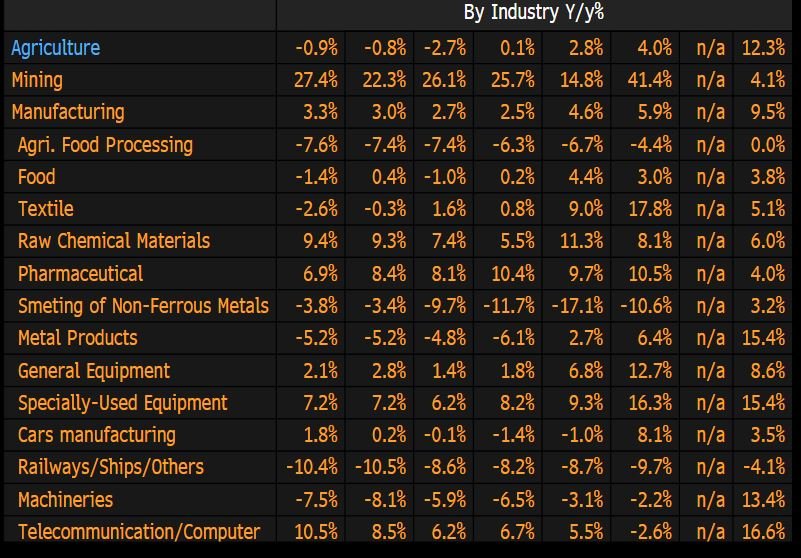

IP tells the same story as retail sales. What's down? EVERYTHING EXCEPT: Food, pharma, railways, and power & heat.

Notice that this means that essential production okay & also those part of the infra push okay but NOT EVERYTHING ELSE 🥶

Notice that this means that essential production okay & also those part of the infra push okay but NOT EVERYTHING ELSE 🥶

Okay, let's look at investment because that tells you about risk appetite for the future (actually you know it's low because LENDING DATA WAS BAD IN JULY). FAI:

a) State is up but private is down (knew this from lending data as local govies up but LENDING DOWN)

a) State is up but private is down (knew this from lending data as local govies up but LENDING DOWN)

Fixed asset investment by sector. What do you see?

a) Agri down & agri processing also down

b) Manufacturing a mixed bag but mostly weak 👇🏻

Look at the contraction. Look at what's holding up investment. U knew this -> all related to infra OK but real activity & tradeable bad.

a) Agri down & agri processing also down

b) Manufacturing a mixed bag but mostly weak 👇🏻

Look at the contraction. Look at what's holding up investment. U knew this -> all related to infra OK but real activity & tradeable bad.

Ready? Now that u have digested the data that I warned u would happen. The next thing to think about is: How does this impact EM Asia, rest of the world & MOST IMPORTANTLY HOW THE PBOC & MOF WILL RESPOND.

Newton's 3rd Law: For every action, there is an equal and opposite reaction

Newton's 3rd Law: For every action, there is an equal and opposite reaction

NBS after the data dump, which underwhelmed, said:

a) High pork prices mainly due to swine fever

b) China's overall inflation is likely to be stable.

Notice what they emphasize & de-emphasize. That tells u what is coming & what they consider a hurdle to easing & not 😉.

a) High pork prices mainly due to swine fever

b) China's overall inflation is likely to be stable.

Notice what they emphasize & de-emphasize. That tells u what is coming & what they consider a hurdle to easing & not 😉.

Watch these clips on our view on Asia 3 wks ago - all still true today. Btw, do u know what this means? Yes u do. I've primed u - more EASING from Asian central banks. What's in the way of that? A hawkish Fed, not CPI. The diff b/n now & 2018 is the Fed.

Sorry, I forgot to include these quotes by NBS, which are important:

a) Downward pressure on China's economy rising 📉

b) Faces severe external pressure

c) Rising jobless due to graduate season📉

d) Higher pork prices due to swine

e) CPI is likely to be stable ✅.

Implications?😉

a) Downward pressure on China's economy rising 📉

b) Faces severe external pressure

c) Rising jobless due to graduate season📉

d) Higher pork prices due to swine

e) CPI is likely to be stable ✅.

Implications?😉

Note that NBS is EMPHASIZING that the downward pressure to the econ & stability of CPI. Reasoning of why the economy is downward & why jobless rate higher not key.

Let's put this equation together

Growth down 📉 + CPI stable ✅ =Policy response❓

What to do❓🥁🥁🥁 Dun dun dun

Let's put this equation together

Growth down 📉 + CPI stable ✅ =Policy response❓

What to do❓🥁🥁🥁 Dun dun dun