JUST OUT

One step closer to an international agreement on new rules to tax multinationals in a digital world!

The OECD has just published the first building blocks of these rules👉bit.ly/2IBPXyp

A lot still needs to be negotiated.

My take? A thread!

#TaxTwitter

One step closer to an international agreement on new rules to tax multinationals in a digital world!

The OECD has just published the first building blocks of these rules👉bit.ly/2IBPXyp

A lot still needs to be negotiated.

My take? A thread!

#TaxTwitter

Some might say there is little progress and not a lot has been decided. I believe it is quite the contrary. It is impressive to see how quickly the OECD and 134 countries have moved from three options to one unified proposal. This is unseen in international tax history!

Where is pillar 2 (the worldwide minimum tax)? True this document only deals with pillar 1 on taxing rights in a digital world. It is expected for the OECD to publish soon a document on pillar 2. France & Germany still defend there can't be pillar 1 without pillar 2.

In pillar 1 we see that the unified approach has been largely influenced by the earlier marketing intangibles proposal (United States), and the distributional approach (put forward by Johnson & Johnson). There are some unitary taxation elements pushed by countries like India.

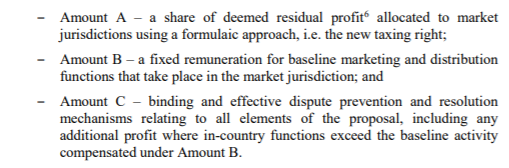

The unified approach has three steps (A, B and C). Step A being the major breakthrough. All companies with a certain turnover in a country even without physical presence might have to allocate a part of their profits to that country.

BUT BUT BUT

BUT BUT BUT

Step A has some worrying elements:

- narrow scope

- likely only a very small share of profits will be allocated to market jurisdictions

- artificial and complex divide between routine/non-routine profits

- segmentation to be expected (per activity, business line or sector)

- narrow scope

- likely only a very small share of profits will be allocated to market jurisdictions

- artificial and complex divide between routine/non-routine profits

- segmentation to be expected (per activity, business line or sector)

- factors of apportionment of profits have not been decided yet but will focus mostly on sales. Employment will have to be taken into account if we want developing countries to benefit else only the rich and big will.

A lot to be decided still, perhaps technical but all crucial.

A lot to be decided still, perhaps technical but all crucial.

Although OECD claims this to be simple I feel we are adding new complexities and grey zones to the international tax rules. We are just adding an extra layer to the existing transfer pricing lasagna. The big winners of this reform are all transfer pricing units of the big four!

Make no mistake the arm's length principle is still here and will still apply to most profits. It is not the big revolution that some were expecting. On the other hand the international taboo on discussing formulary apportionment is dead.

What is next?

(1) G20 Finance Ministers meeting on 17 October

(2) The public consultation on 21 and 22 November

(3) Economic Impact assessments by OECD

(4) Update on pillar 2

(5) January plenary meeting of all 134 countries

...

(6) Final agreement by end 2020

(1) G20 Finance Ministers meeting on 17 October

(2) The public consultation on 21 and 22 November

(3) Economic Impact assessments by OECD

(4) Update on pillar 2

(5) January plenary meeting of all 134 countries

...

(6) Final agreement by end 2020

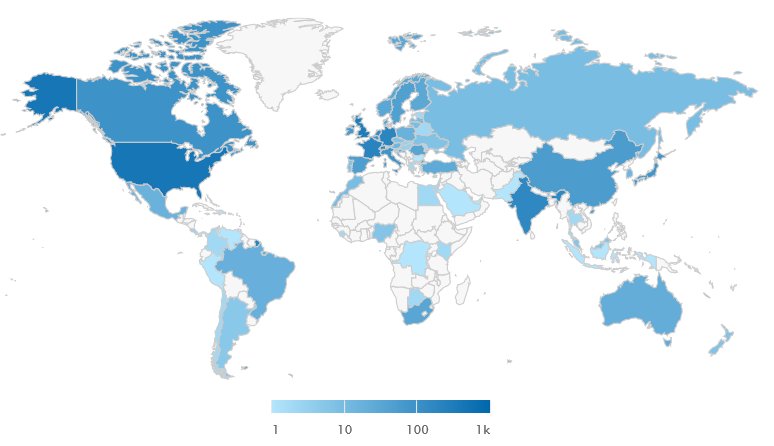

For me the most interesting visual of the day! Where was the #OECDtaxtalks watched most 👇

India, US, France and Germany colour dark blue. No surprise.

India, US, France and Germany colour dark blue. No surprise.