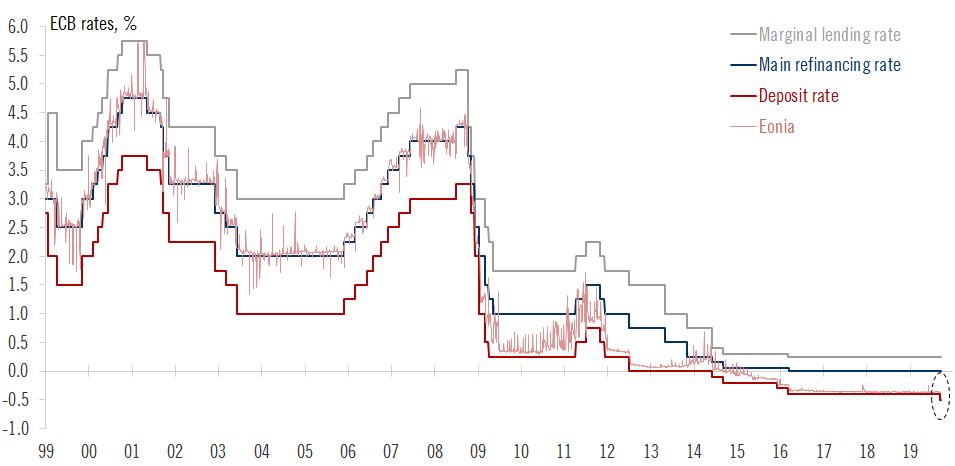

The new limits of ECB policies – our latest, looking to the future on this special day. (1/n)

perspectives.group.pictet/sites/perspect…

perspectives.group.pictet/sites/perspect…

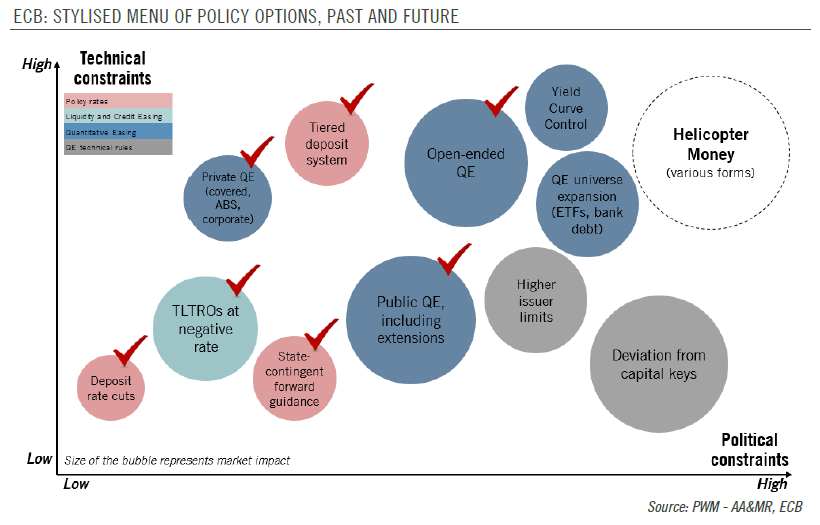

It’s a silly question that we are asking. There are no limits, within the mandate of course. Problem is: (1) the side-effects of existing measures are increasing, and (2) the political appetite for policy innovation is shrinking. (2/n)

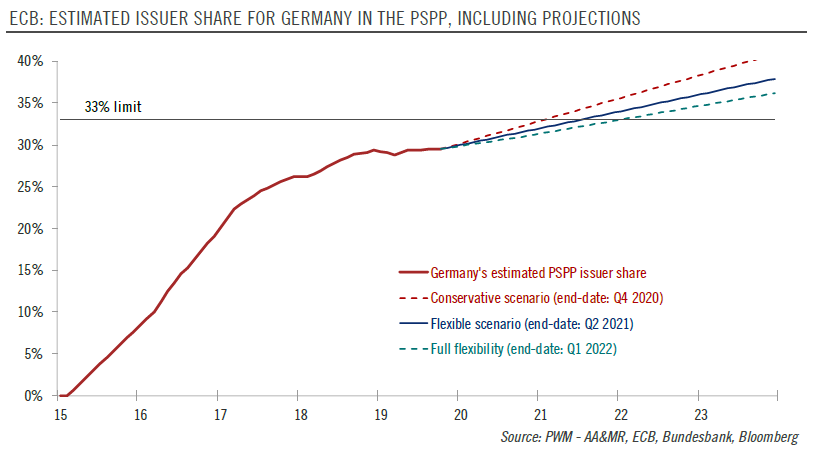

The elephant in the room is open-ended QE. Assuming a slow recovery in core inflation, we expect ECB QE to continue for two years, and issuer limits to be raised by the end of 2020 to free up enough buying space. (3/n)

Our estimates put Germany’s issuer share at 30%. The ECB/Buba could buy more time by reducing the share of central government debt relative to everything else (corporate, agencies, munis) but there’s a limit to how far this can be stretched. (4/n)

In a ‘full flexibility’ scenario, asset purchases could run for 18-24 months under the 33% limits (vs. 12 months under conservative assumptions).

But, QE can only be truly open-ended if there are no limits on a forward-looking basis, e.g. if purchases need to be increased. (5/n)

But, QE can only be truly open-ended if there are no limits on a forward-looking basis, e.g. if purchases need to be increased. (5/n)

Draghi made two interesting comments about limits last week: (1) net debt issuance is important (political cover for Lagarde to raise limits?); (2) the stock of bonds is the relevant metrics for capital keys (Germany overpurchased by €6-22bn, could buy another 3 months). (6/n)

Tiering: it’s coming (30 October)!

- reduces the cost of negative rates from €8.7bn to €5.0bn (though it will increase in 2020)

- creates €35bn in arbitrage opportunities for Italian banks

- no signs of major disruption in repo, so far (7/n)

- reduces the cost of negative rates from €8.7bn to €5.0bn (though it will increase in 2020)

- creates €35bn in arbitrage opportunities for Italian banks

- no signs of major disruption in repo, so far (7/n)

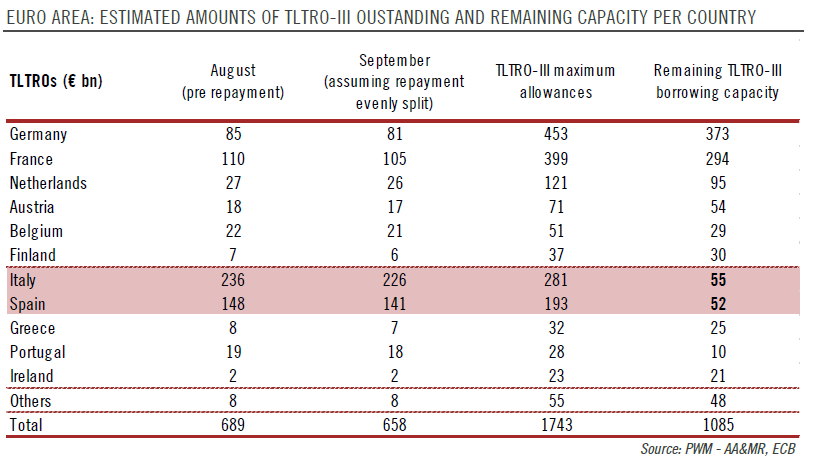

TLTRO-III: expect a large take-up in December and beyond, with demand being driven by favourable cost of funding, TLTRO-II rollover, and tiering arbitrage. (8/n)

In the end, the recalibration of existing tools is more complicated than in the past, but not insurmountable. New tools could be introduced. In the transition to a new Executive Board, the main obstacle to further ECB easing will be of political nature. (/end)

Addendum on (German) issuer limits. Lots of moving parts, always happy to discuss.