Please RT

THREAD

How Sukuks (Islamic Bonds) break AAOIFI Rules

In this thread () we talked about Sukuk, now we will see how market practice breaks the required Shariah rules.

THREAD

How Sukuks (Islamic Bonds) break AAOIFI Rules

In this thread () we talked about Sukuk, now we will see how market practice breaks the required Shariah rules.

AAOIFI have very clear rules on Sukuk, and some of the key areas were changed in around 2008, after criticism by Justice Taqi Usmani, perhaps the most prominent Islamic finance scholar in the world.

AAOIFI is the world’s leading (and best) maker of Shariah standards for Islamic

AAOIFI is the world’s leading (and best) maker of Shariah standards for Islamic

banking transactions. Their rules on Sukuk are (generally) very good.

However, the market still insists on breaking these rules.

I will give a brief overview on how this happens, and then why.

First of all lets look at what AAOIFI says.

However, the market still insists on breaking these rules.

I will give a brief overview on how this happens, and then why.

First of all lets look at what AAOIFI says.

They have different rules for Ijara (leasing) Sukuk (they should not, but they do), so we will look at non Ijara Sukuks. This is from Shariah Standard (17) on Investment Sukuk:

Why is this important?

Well, because AAOIFI do not want Sukuk just to be debt priced at interest. So they want to remove some of the key aspects of debt from Sukuk. And one of the key aspects is that, when the loan matures, the borrower has to return the capital to the lender.

Well, because AAOIFI do not want Sukuk just to be debt priced at interest. So they want to remove some of the key aspects of debt from Sukuk. And one of the key aspects is that, when the loan matures, the borrower has to return the capital to the lender.

If we really used Sukuk properly, then the assets would be sold back to the obligor at MARKET PRICE of the assets, and not the nominal value.

If they are always sold at nominal value, then this a massive confirmation that all the parties are just creating debt, and breaking

If they are always sold at nominal value, then this a massive confirmation that all the parties are just creating debt, and breaking

AAOIFI Shariah rules.

Now let us look at some recent market issues of Sukuk. I literally chose 3 random Sukuks from sukuk.com for this, and then opened the prospectus and searched it (I know where to look, fortunately, and these documents are up to 500 pages long)

Now let us look at some recent market issues of Sukuk. I literally chose 3 random Sukuks from sukuk.com for this, and then opened the prospectus and searched it (I know where to look, fortunately, and these documents are up to 500 pages long)

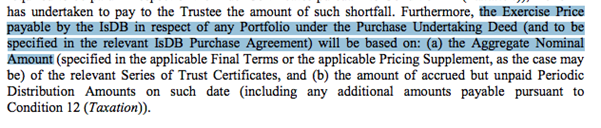

Islamic Development Bank Sukuk (issued March 2018, $1,25bn), Mudarabah structure

From the prospectus:

From the prospectus:

Next: DP World Crescent Sukuk (Hybrid structure, issued May 2016, $1.2bn)

From the prospectus:

From the prospectus:

Also:

Final Example:

Dubai Islamic Bank, Hybrid structure, February 2018, $1bn

Dubai Islamic Bank, Hybrid structure, February 2018, $1bn

I could carry on for days and days, and I do in fact cover dozens of different Sukuk issuances in much more detail in my book on Sukuk, and there are NO EXCEPTIONS.

Every single Sukuk I have ever reviewed always has the redemption price based on face/nominal value of the Sukuk.

Every single Sukuk I have ever reviewed always has the redemption price based on face/nominal value of the Sukuk.

Clearly this breaks AAOIFI rules.

WHY DOES THIS MATTER?

To understand this, we have to understand why AAOIFI made this impermissible. Taqi Usmani highlighted several aspects of Sukuk that rendered them debt instruments

WHY DOES THIS MATTER?

To understand this, we have to understand why AAOIFI made this impermissible. Taqi Usmani highlighted several aspects of Sukuk that rendered them debt instruments

rather than based on (and priced on) real assets. These points included:

1) Sukuk certificates should not be redeemed at face value (like debt) - rather should be linked to the underlying assets

2) any profit shortfalls should not be met by the Sukuk issuer, the investors should

1) Sukuk certificates should not be redeemed at face value (like debt) - rather should be linked to the underlying assets

2) any profit shortfalls should not be met by the Sukuk issuer, the investors should

take risk that the assets may not perform

3) Any excess profit should be kept by the investors, not delivered back to the issuer.

The AAOIFI rules were then changed to enforce these rules. And every single Sukuk issuance in the world breaks these rules.

3) Any excess profit should be kept by the investors, not delivered back to the issuer.

The AAOIFI rules were then changed to enforce these rules. And every single Sukuk issuance in the world breaks these rules.

Here is a question for you: how many Sukuk issuances actually claim to be compliant with AAOIFI rules?

Answer: ZERO.

Now, you know why they do not dare to make this claim - because they would be lying.

Answer: ZERO.

Now, you know why they do not dare to make this claim - because they would be lying.

WHY IS THIS IMPORTANT:

This is absolutely crucial. Because everyone in the market wants Sukuk to be debt instruments - the issuer, the banks, the investors, the arrangers – everyone.

Because debt instruments follow known behaviour –

This is absolutely crucial. Because everyone in the market wants Sukuk to be debt instruments - the issuer, the banks, the investors, the arrangers – everyone.

Because debt instruments follow known behaviour –

– they are priced transparently, and traded easily, and fit into portfolios easily, and so on. In short, because they are designed to fit into markets designed around debt and interest (Riba).

What can we do?

Well, you do what you like - my responsibility is to highlight the double standards that are clear in the modern Islamic banking industry.

Does it matter?

To me, it is important. I like to think my faith has high values that should not be traded for profit.

Well, you do what you like - my responsibility is to highlight the double standards that are clear in the modern Islamic banking industry.

Does it matter?

To me, it is important. I like to think my faith has high values that should not be traded for profit.

I think this is unacceptable.

I know pricing at interest is wrong, but others think it is ok. Even if you think it is ok, you will find that when we force contracts to price at Riba, then we end up breaking Shariah rules in the contracts.

I have shown one instance here, and this

I know pricing at interest is wrong, but others think it is ok. Even if you think it is ok, you will find that when we force contracts to price at Riba, then we end up breaking Shariah rules in the contracts.

I have shown one instance here, and this

this happens many, many times in Islamic contracts.

To me, this action is completely beyond me.

It appears integrity and honesty have been ditched for profit.

But, you should know. Ignorance of what is done in the name of our religion is no longer an excuse for you.

/THREAD

To me, this action is completely beyond me.

It appears integrity and honesty have been ditched for profit.

But, you should know. Ignorance of what is done in the name of our religion is no longer an excuse for you.

/THREAD