Please RT

THREAD

Goldsmiths, paper money and banking

I want to talk about how paper money was first created, and how this has an impact on Islamic banking

THREAD

Goldsmiths, paper money and banking

I want to talk about how paper money was first created, and how this has an impact on Islamic banking

The development of money has gone through four major stages

1)Commodity money

This is where something of intrinsic value was used as money. Salt in the Mediterranean region, Silk in China, and of course, gold and silver. In early Islam, gold and silver were used,

1)Commodity money

This is where something of intrinsic value was used as money. Salt in the Mediterranean region, Silk in China, and of course, gold and silver. In early Islam, gold and silver were used,

as well as items such as armour, dates, wheat and so on. These items had to be durable, easily divisible – and ideally light in weight and easy to transport. This money was used as early as 10th century BC

2)Representative Money

Is paper currency that can be exchanged

2)Representative Money

Is paper currency that can be exchanged

exchanged for goods of value often gold or sliver. Some states in the US issued paper backed by tobacco in the 18th century. China is often credited with creating the first paper money as early as the 11th century. Here will will focus on this transformation and the role played

by Goldsmiths in London in the 17th century

3)Fiat money

This has no intrinsic value and can NOT be redeemed for any real assets or commodity. Modern paper currency is an example of fiat money, Look at what it says on a modern UK bank note:

3)Fiat money

This has no intrinsic value and can NOT be redeemed for any real assets or commodity. Modern paper currency is an example of fiat money, Look at what it says on a modern UK bank note:

“I promise to pay the bearer on demand the sum of Ten pounds”.

The Bank of England admit this is a meaningless promise – we can not present this note and expect in exchange £10 worth of anything.

Fiat money works on the basis of trust.

The Bank of England admit this is a meaningless promise – we can not present this note and expect in exchange £10 worth of anything.

Fiat money works on the basis of trust.

It is worth £10 simply because we believe that. And as long as we want to pay for something, and the seller also believes that, then the transaction can occur.

From the BoE website:

From the BoE website:

4)Electronic money

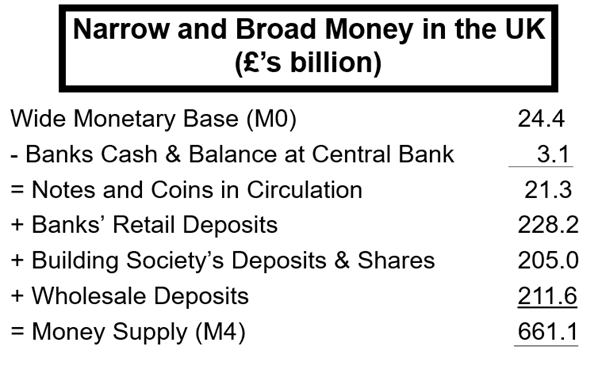

This is modern money for most of us. Electronic money that sits in our bank accounts, that we use to pay for things via cards, and online payments. In the UK, only 3% of the wide money supply is physical notes and coins, the rest is electronic money

This is modern money for most of us. Electronic money that sits in our bank accounts, that we use to pay for things via cards, and online payments. In the UK, only 3% of the wide money supply is physical notes and coins, the rest is electronic money

(and up to 80% or more of electronic money is debt created – out of thin air – by banks)

Physical money / total money = 21.3 / 661.1 = 3.2%

Ok, now let us look at the process of moving from commodity money (gold) to paper money occurred in the UK.

Physical money / total money = 21.3 / 661.1 = 3.2%

Ok, now let us look at the process of moving from commodity money (gold) to paper money occurred in the UK.

In the 17th century, a lot of wealth was stored as gold. And of course, currency was made from gold, and silver. However, one problem is the safe storage of currency and wealth. So, what happened was that wealth holders would often deliver the gold to others who could

keep the gold safe.

These were often goldsmiths who would already hold positions of trust in the community, and have secure methods of storage and protection of gold. Of course, the goldsmith would charge for these safekeeping services.

These were often goldsmiths who would already hold positions of trust in the community, and have secure methods of storage and protection of gold. Of course, the goldsmith would charge for these safekeeping services.

So, if a customer then needed to pay for something, they could go to the goldsmith, and just remove some of the gold that is being held in their name, and spend it as desired.

Now, in order to reflect ownership, the goldsmith would issue a receipt to the customer, when the gold

Now, in order to reflect ownership, the goldsmith would issue a receipt to the customer, when the gold

gold is deposited.

Now, let us imagine, that the customer can not be bothered with actually going to the goldsmith, giving the receipt, taking the gold and giving it to a client for a purchase transaction. That leaves the client in the same position

Now, let us imagine, that the customer can not be bothered with actually going to the goldsmith, giving the receipt, taking the gold and giving it to a client for a purchase transaction. That leaves the client in the same position

position – with an amount of gold, and now he would need to go over to his goldsmith, deposit the gold, obtain a receipt.

So, instead, the goldsmith tells his customer, that he can use the receipt to give it to someone else, and the goldsmith would honour the claim as long

So, instead, the goldsmith tells his customer, that he can use the receipt to give it to someone else, and the goldsmith would honour the claim as long

as that receipt was presented in good form.

So, now the customer can use the receipt to pay for items:

So, this is becoming more efficient already.

Next step: if the customer has deposited gold worth £100, and has a single receipt for this, this is easy to use the receipt to

So, now the customer can use the receipt to pay for items:

So, this is becoming more efficient already.

Next step: if the customer has deposited gold worth £100, and has a single receipt for this, this is easy to use the receipt to

to buy items worth £100. But what if the item was worth only £10?

No problem, says the goldsmith, I will give you a number of receipts of smaller value:

No problem, says the goldsmith, I will give you a number of receipts of smaller value:

Now the customer can use a single receipt to pay for an item worth £10, same process as before:

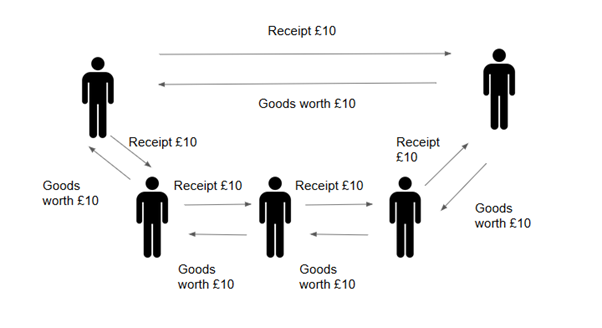

Next step – the seller, having no need for physical gold, finds it easier to actually just use that £10 receipt to pay for something else, and that new recipient can use the same receipt to pay for something else, and so on. Until one recipient actually decides he wants the gold

and presents the receipt to the goldsmith:

Next step, as TRUST in the receipt grows in the community, people find that this receipt is actually easier and more convenient to use for payment, than actually redeeming it for gold.

So, the goldsmith discovered, that some of his

Next step, as TRUST in the receipt grows in the community, people find that this receipt is actually easier and more convenient to use for payment, than actually redeeming it for gold.

So, the goldsmith discovered, that some of his

receipts, he never saw them again! They were continuously circulated in the economy.

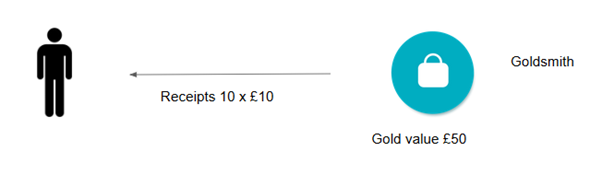

Next, the goldsmith does some calculations. He discovers, for example, that of all the receipts he issues on a deposit of £100 of gold (10 receipts at £10 each),

Next, the goldsmith does some calculations. He discovers, for example, that of all the receipts he issues on a deposit of £100 of gold (10 receipts at £10 each),

only 5 of these (worth £50) are presented to him, and he has to deliver gold against them.

Next, the cunning goldsmith realises he can use this to his advantage.

Next, the cunning goldsmith realises he can use this to his advantage.

What if, the next time someone deposits just £50 gold with him, he can still issue 10 receipts at £10 because only 5 will ever be presented to him in the future.

Very smart!

Very smart!

So, he issues receipts worth £50 to the depositor, and gives new receipts, also worth £50, but with NO GOLD backing them, to new customers:

Now, of these 5 new receipts of £10, they are used in the economy, as we know. So, when someone does in fact present a receipt to the goldsmith, he still has to honour it. But he knows only half of these will come to present the receipt.

In addition, the person to whom the goldsmith made a loan of £10, has to repay the loan to the goldsmith. This can be via presenting a receipt, or perhaps gold.

If we notice there NO PROFIT for the goldsmith here. We also notice, that the gold smith has added £50 of “money” to the existing gold money supply. This can have inflationary impacts, of course.

So, the goldsmith now thinks about how to make money from this creation of £50 of

So, the goldsmith now thinks about how to make money from this creation of £50 of

non-gold-backed paper.

The answer is simple – for each new loan of £10 he gives in new paper, he asks for £11 to be repaid, either in gold or paper, or ideally, in £10 paper and £1 of gold.

The answer is simple – for each new loan of £10 he gives in new paper, he asks for £11 to be repaid, either in gold or paper, or ideally, in £10 paper and £1 of gold.

Of course this is a simplistic view, but it gets across the essence of the process used by goldsmiths, to enable the transformation from commodity money to representative money, through to fiat money.

We can see, as long as this process of creation of fiat money is in private

We can see, as long as this process of creation of fiat money is in private

private hands, there no incentive to issue new money UNLESS the lender makes a profit. This profit is achieved by charging interest.

It is feasible for a government to create such money to actually pay for real services, and not aim to make money at interest. However, the

It is feasible for a government to create such money to actually pay for real services, and not aim to make money at interest. However, the

governments have long since given the power to create money to private enterprises.

If you think the Bank of England was created by the UK government, think again!

It was nationalised relatively recently, in 1946:

If you think the Bank of England was created by the UK government, think again!

It was nationalised relatively recently, in 1946:

Ok, this is all very interesting, now how does this impact Islamic banking?

Firstly. We notice that fiat money has no underlying assets backing it.

Commodity money of course, is made from assets of value (gold, silver etc) and representative money represents ownership of such

Firstly. We notice that fiat money has no underlying assets backing it.

Commodity money of course, is made from assets of value (gold, silver etc) and representative money represents ownership of such

real assets.

But fiat money, has no assets backing it. Modern currency is fiat money, and electronic money.

And we can see that fiat money, when created by private enterprises, MUST charge interest on its creation, and its creation is via lending.

But fiat money, has no assets backing it. Modern currency is fiat money, and electronic money.

And we can see that fiat money, when created by private enterprises, MUST charge interest on its creation, and its creation is via lending.

This process is continued today. In the UK, private banks continue to create new money in the form of credit/loan creation. The Bank of England estimates 80% of the money supply in the UK comprises bank credit/debt.

This is quite astonishing if you think about it.

This is quite astonishing if you think about it.

Now, the idea of fiat money is quite difficult to assess in Shariah law. One view is that as long as the currency is held as legal tender, then it is permissible. Another view is that such money is impermissible as there are no real assets backing it.

This has several implications – banks really exist to create debt and charge interest. They are not financial intermediaries of capital – that myth has been busted some years back.

So, when we have Islamic banks, we see they operate in EXACTLY the same model.

So, when we have Islamic banks, we see they operate in EXACTLY the same model.

They exist simply to create debt, and charge interest.

That is why 98-99% of everything they do is priced at interest / Riba.

So, this has quite an astonishing impact on the Islamic banking system.

That is why 98-99% of everything they do is priced at interest / Riba.

So, this has quite an astonishing impact on the Islamic banking system.

What is the answer?

Read my thread about asking “what is the answer?” and “how to fix Islamic banking?”.

Thank you for reading

/THREAD

Read my thread about asking “what is the answer?” and “how to fix Islamic banking?”.

Thank you for reading

/THREAD