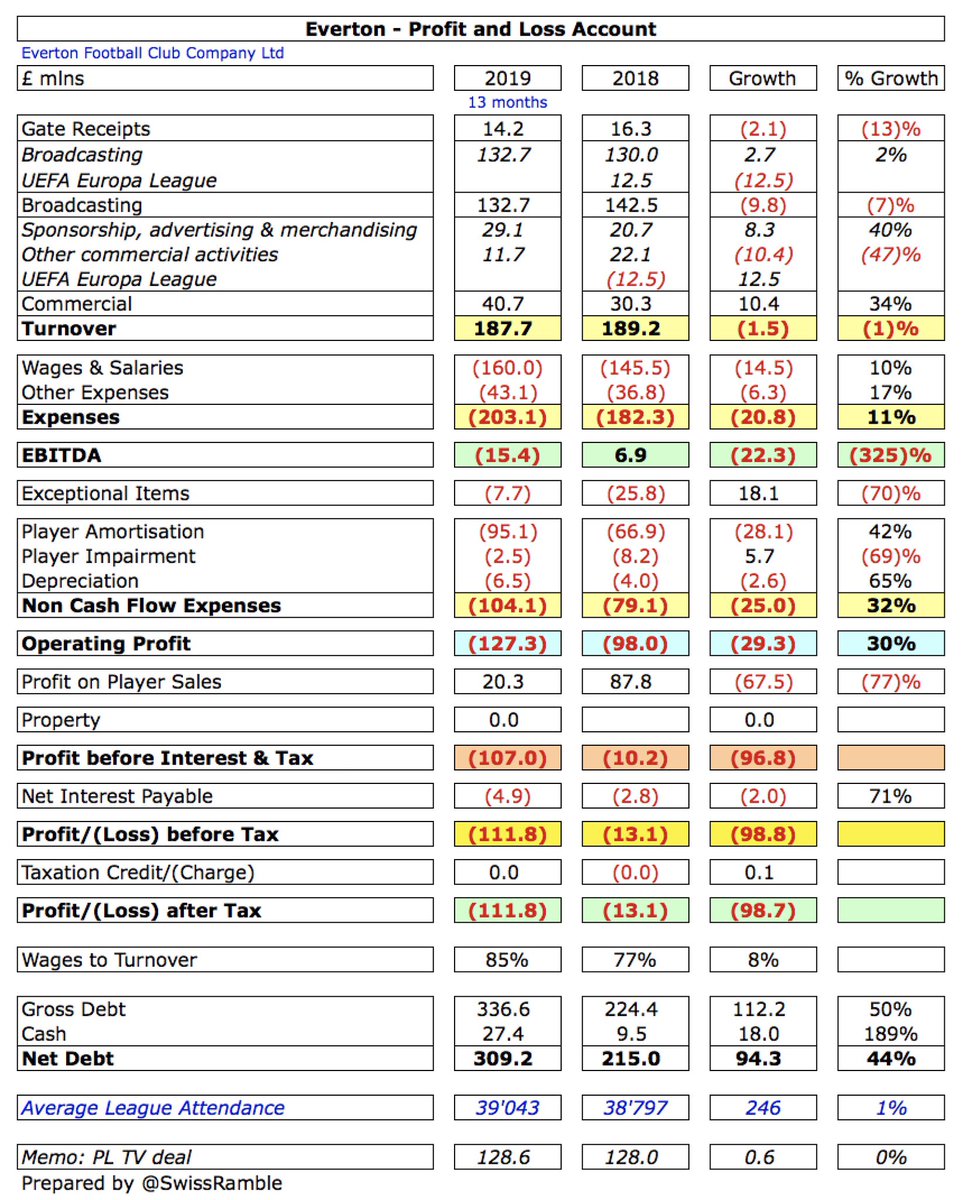

Everton’s 2018/19 financial results covered a season when they finished 8th in the Premier League for the second year in a row. Marco Silva replaced Sam Allardyce as manager in May 2018 #EFC

As a technical point, it’s worth noting that #EFC changed their accounting close date from May 31st to June 30th, so the 2018/19 accounts covered a 13 month period with little impact on turnover, but an additional month of expenses, which adversely impacted the bottom line.

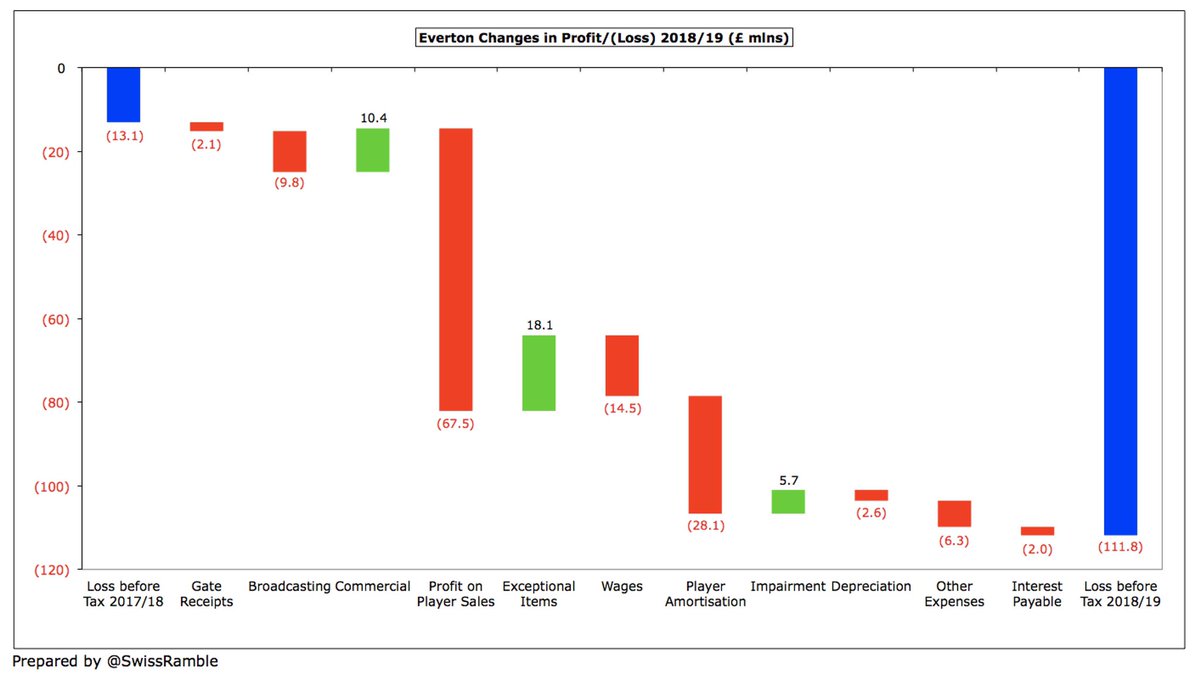

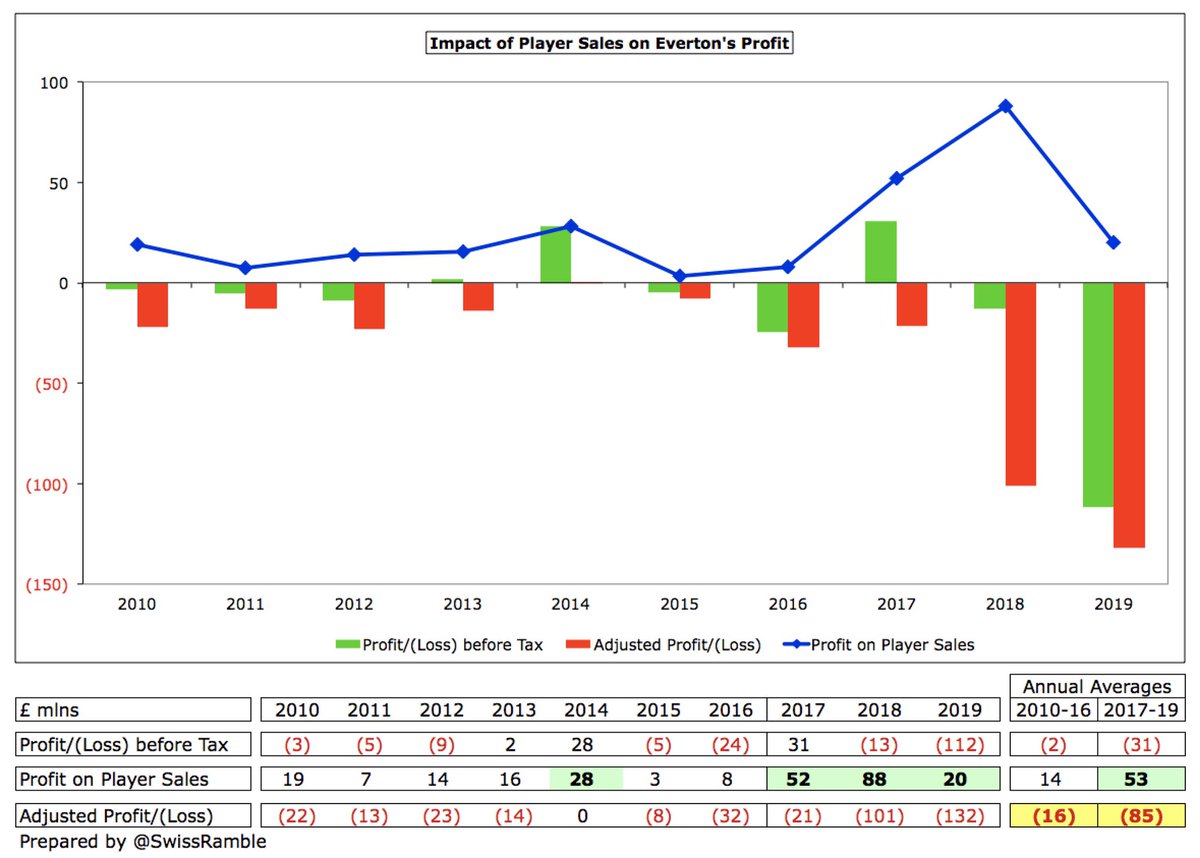

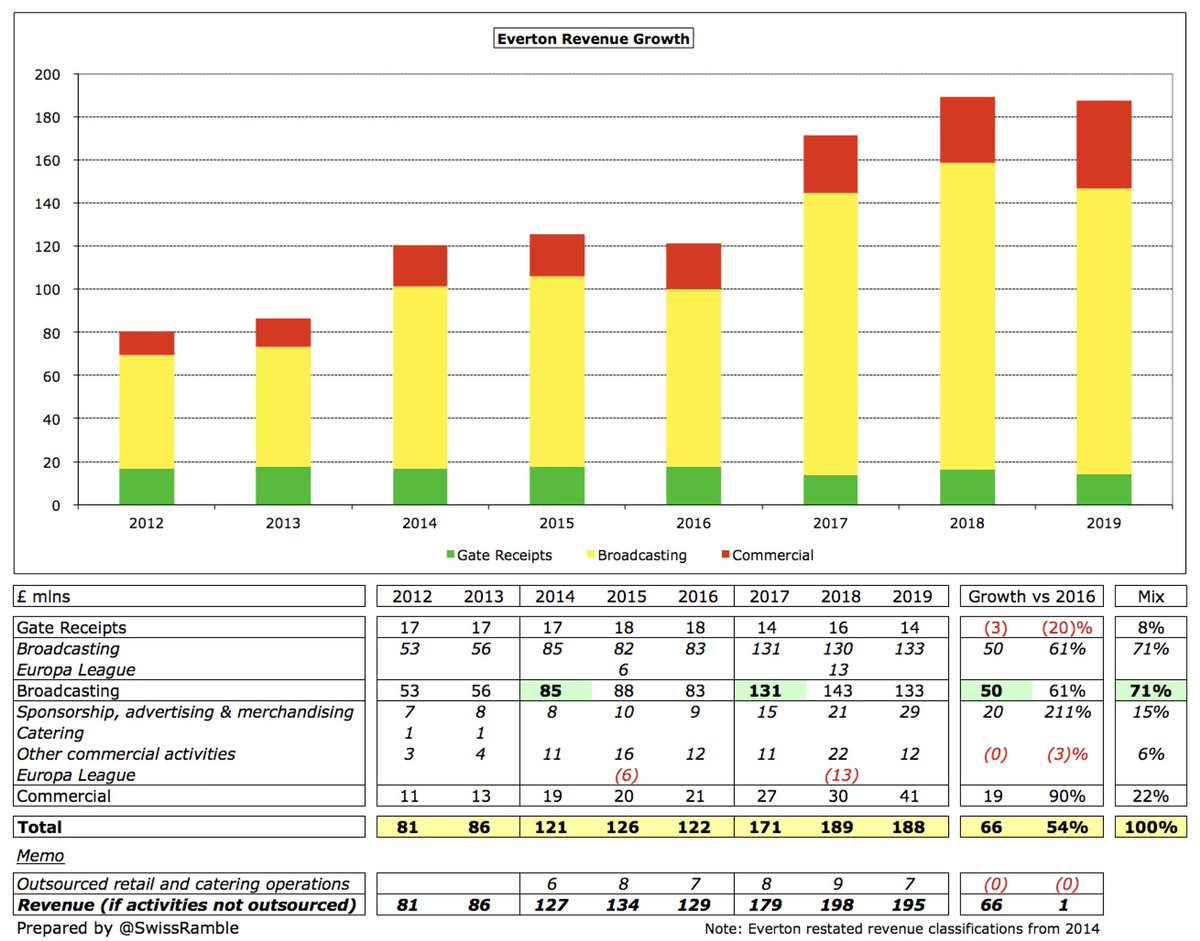

#EFC loss shot up from £13m to a club record £112m, as revenue fell slightly (1%) to £188m, still second highest in club’s history, despite dropping out of the Europa League, and profit on player sales fell £68m to £20m, while player investment meant expenses increased by £46m.

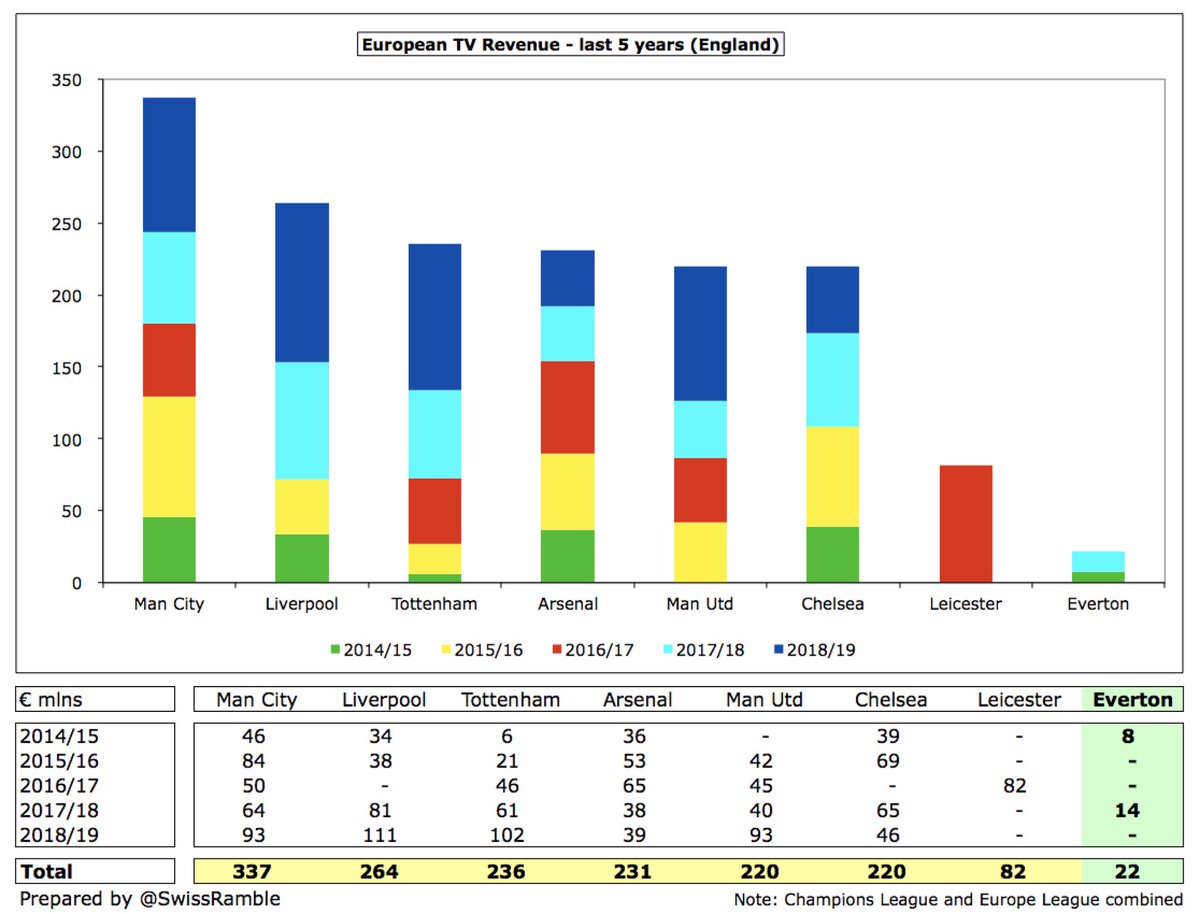

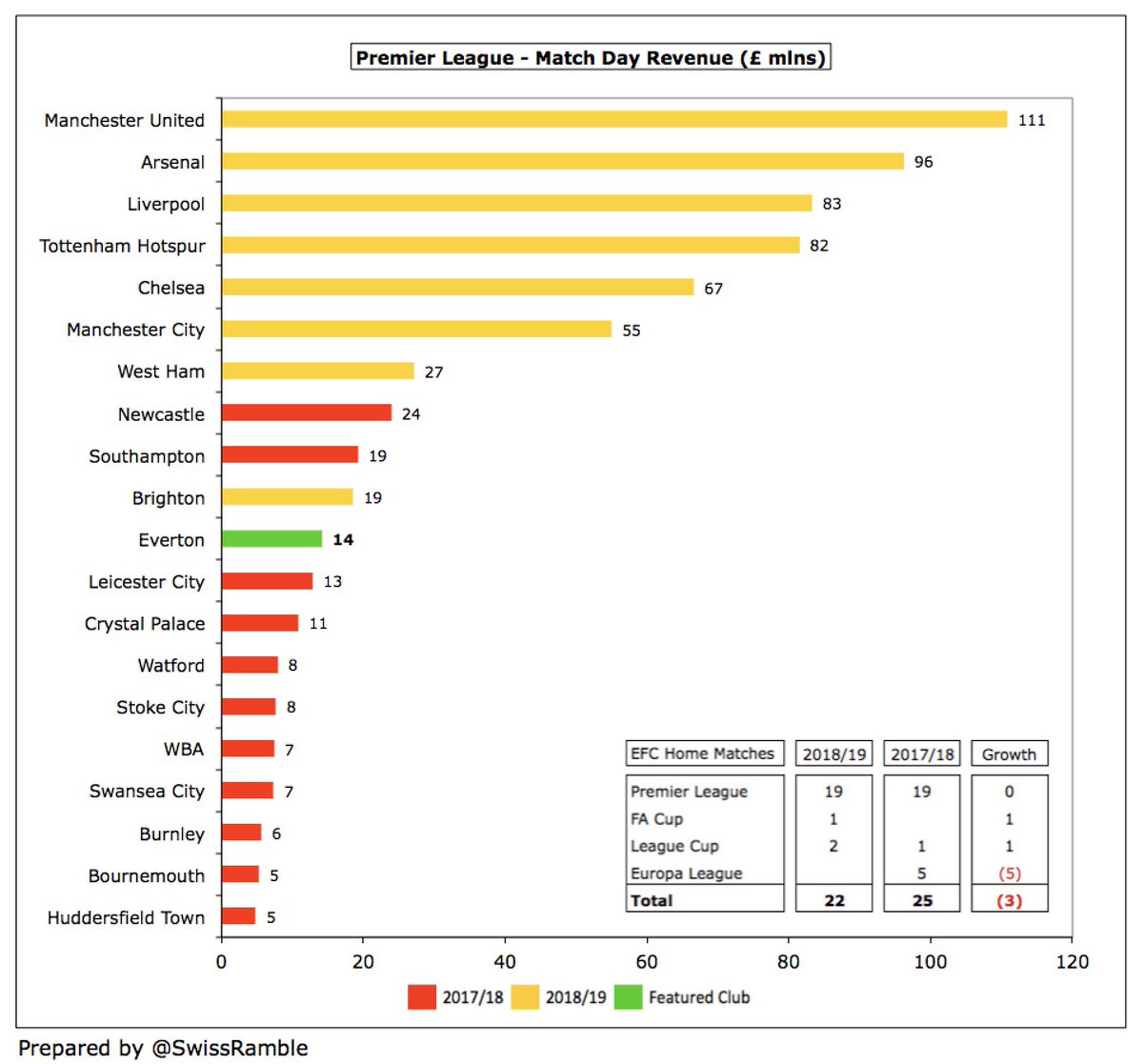

Failure to qualify for the Europa League meant #EFC broadcasting fell by £10m (7%) to £133m, while gate receipts decreased £2m (13%) to £14m for the same reason. This shortfall was largely compensated by a £10m (34%) increase in commercial to £41m.

Note: #EFC include Europa League prize money in Other Commercial, which I have reclassified to Broadcasting in order to be consistent with the way that other clubs report this revenue.

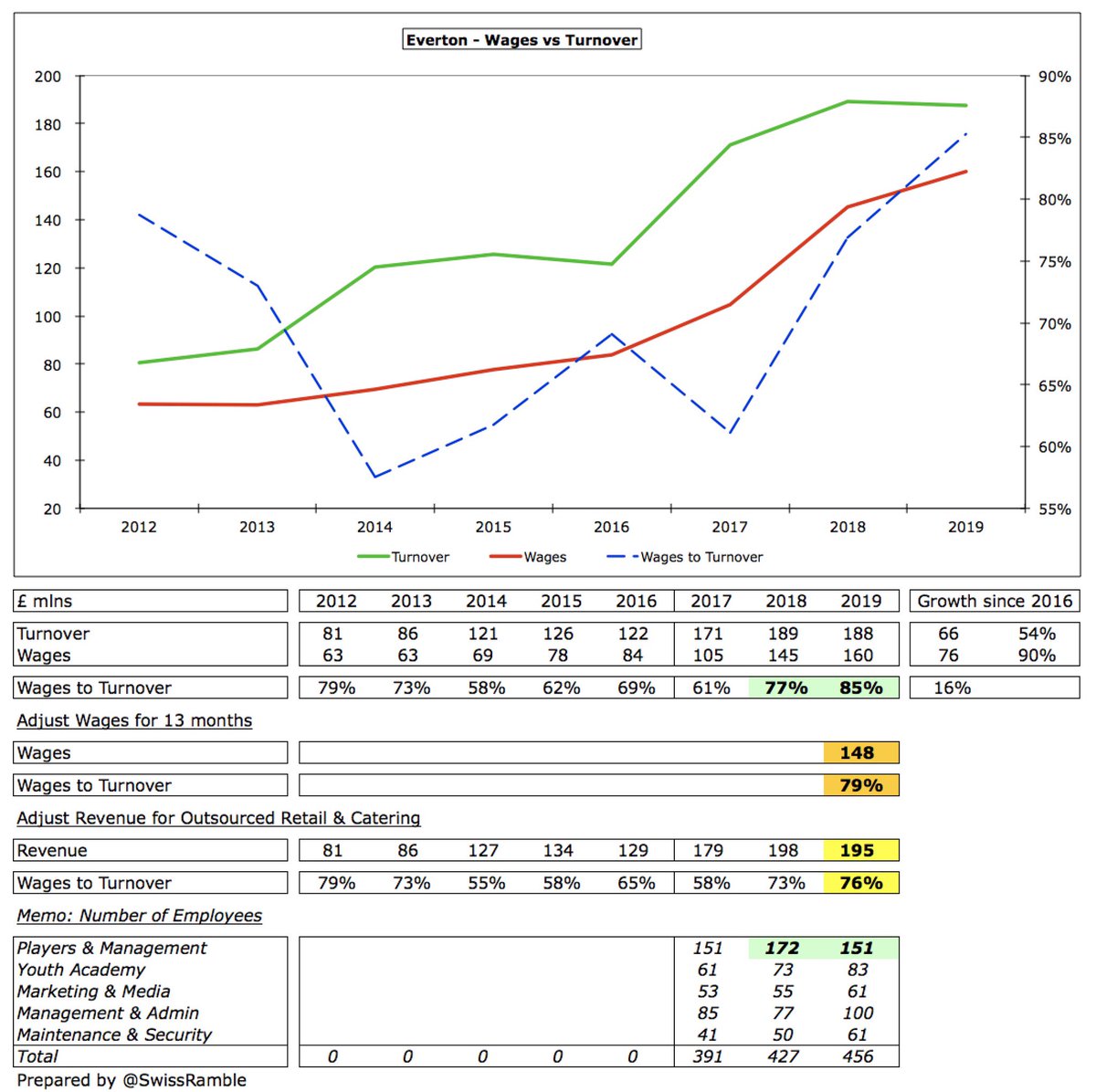

Following further investment in the squad, #EFC wage bill increased £15m (10%) to £160m and player amortisation rose £28m (42%) to £95m, while other expenses were up £6m (17%) to £43m. On the other hand, exceptional items and player impairment were £18m and £6m lower respectively

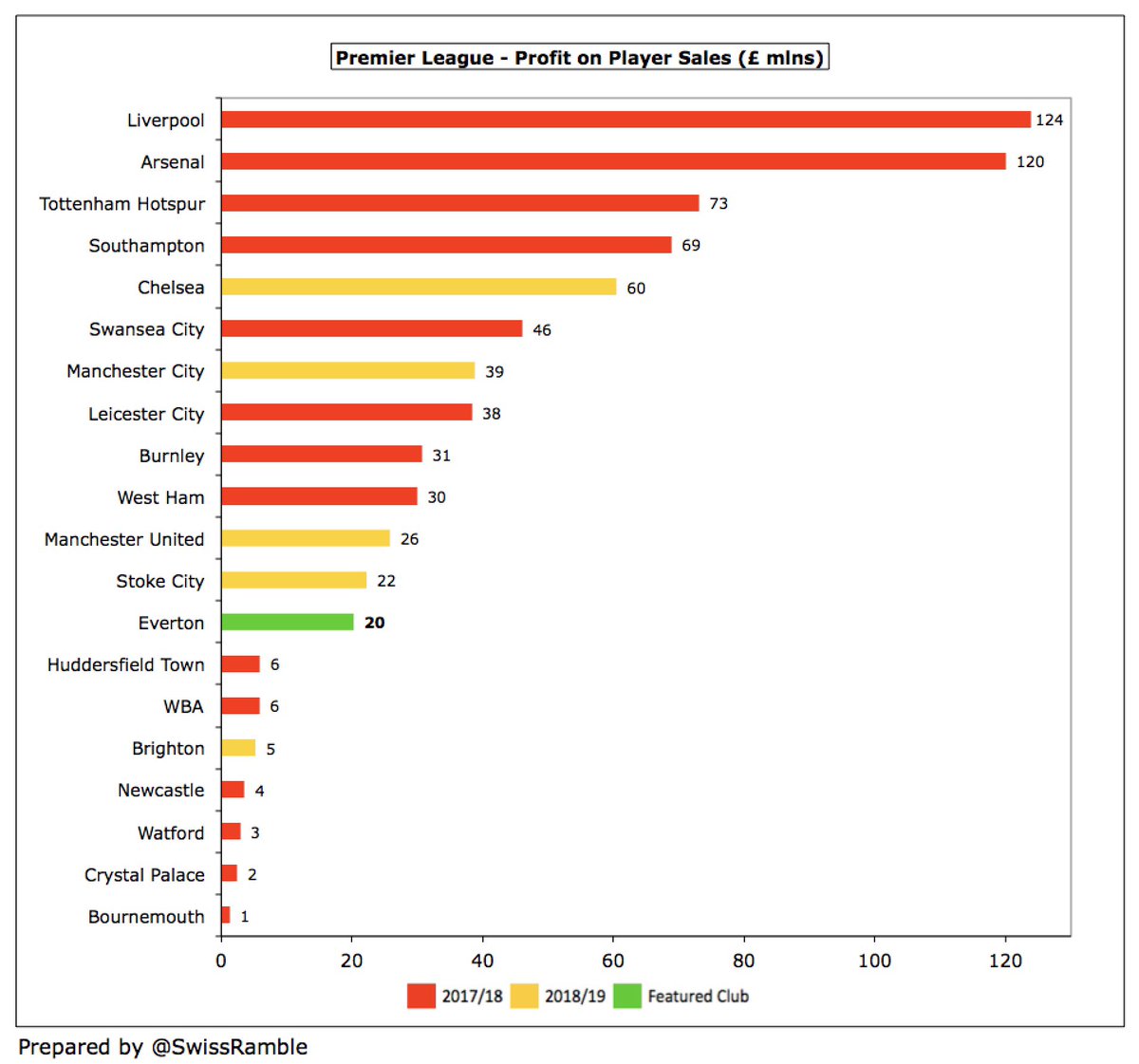

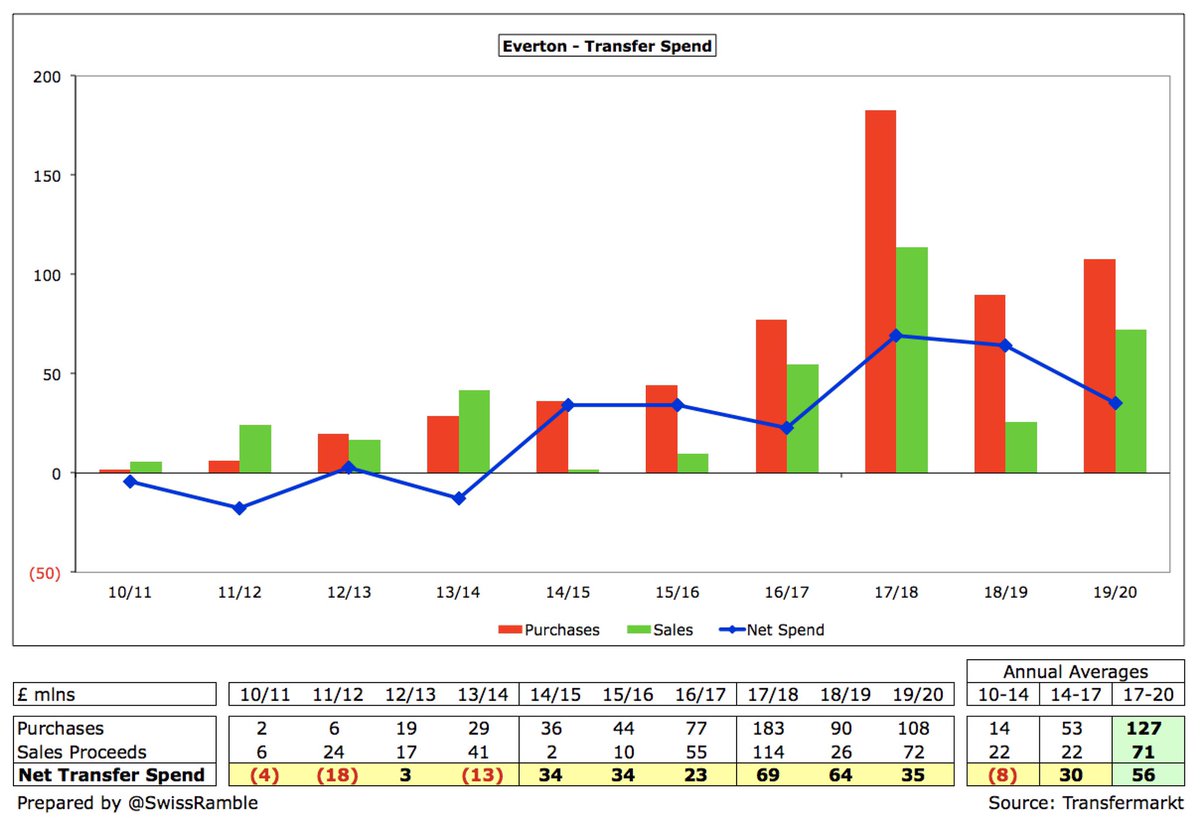

#EFC could have reduced the loss with more player sales, but they looked to retain their key talent. As a result, profit on player sales fell from £88m to £20m, mainly Davy Klaassen to Werder Bremen and Funes Mori to Villarreal. Prior season included Lukaku, Barkley and Deulofeu.

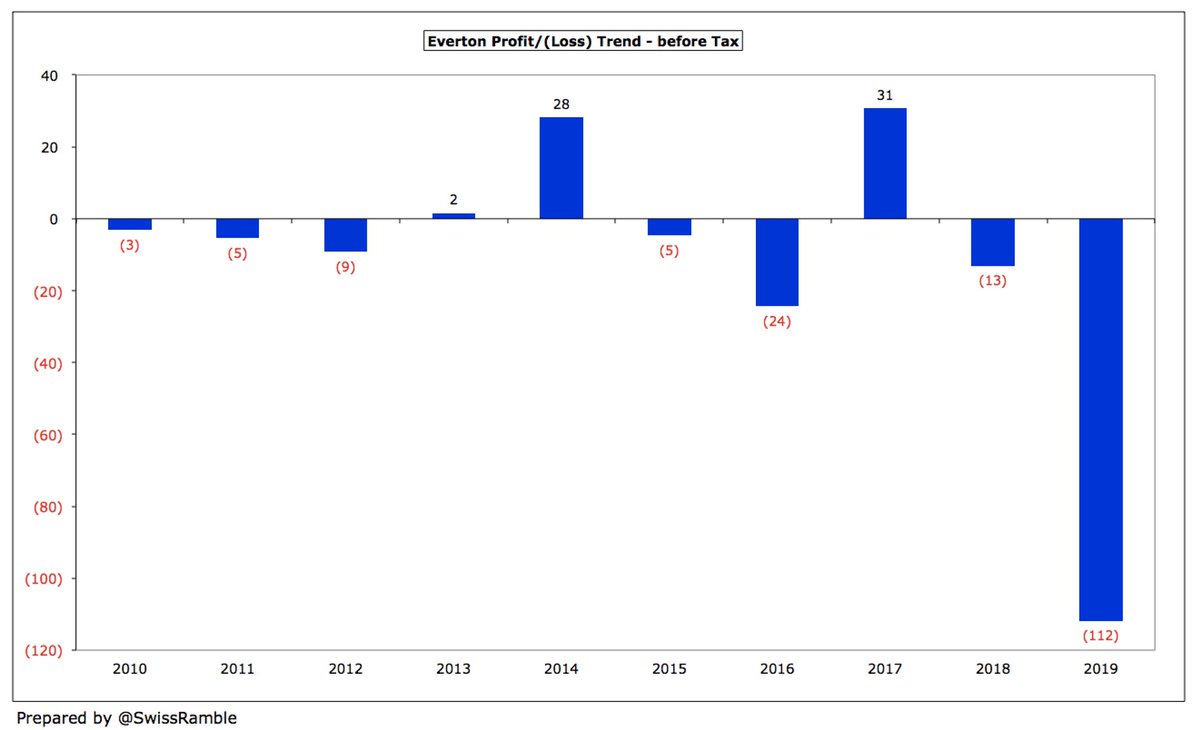

#EFC have reported losses 4 times in last 5 seasons with the sole exception being £31m profit in 2017. Total deficit over this period was £123m, but £112m of this in last season. In 14 years since 2005, club has only been profitable 4 times – and 2008 was just £26k.

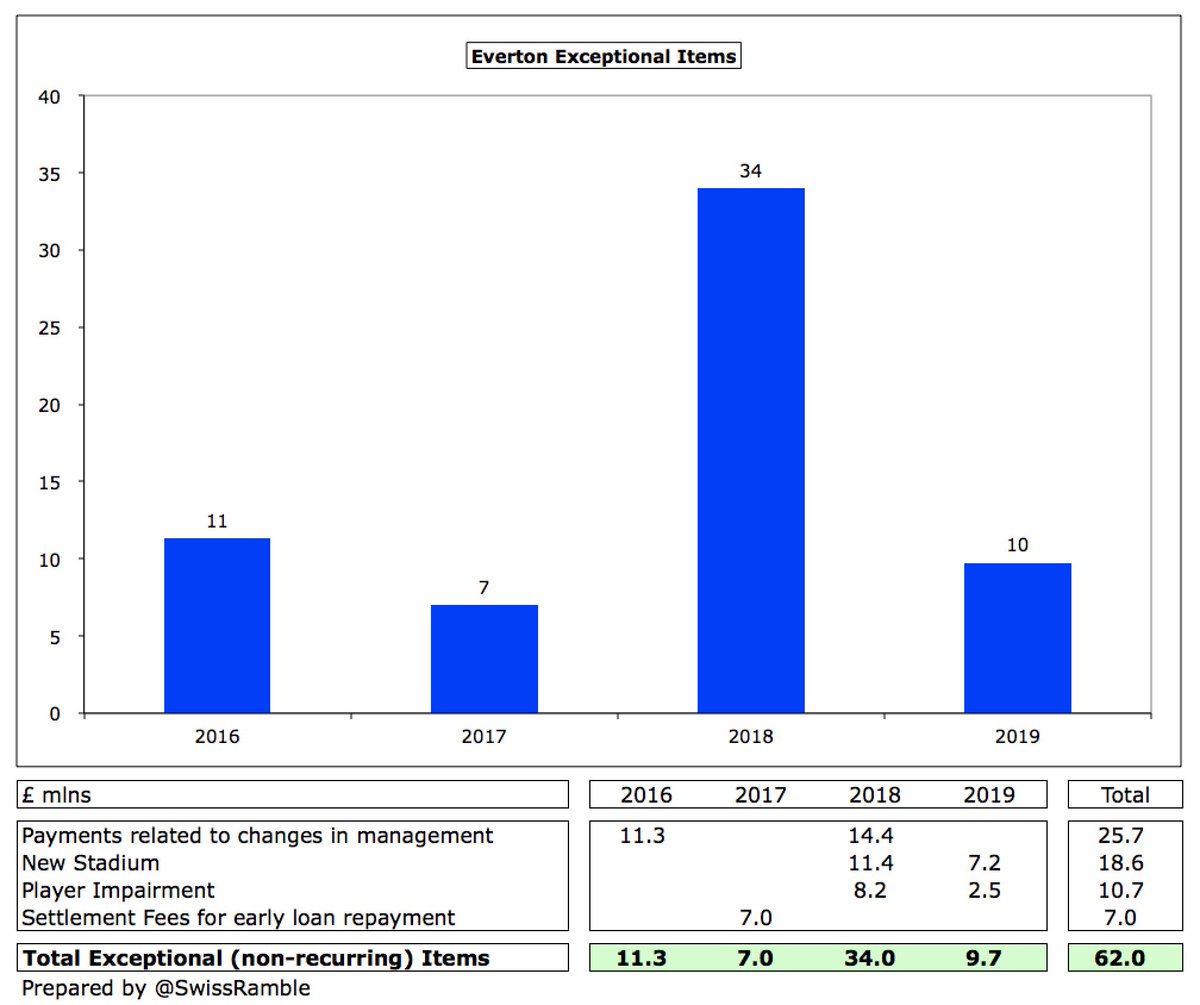

#EFC figures hit by £62m exceptional costs in last 4 seasons, including £26m payments for management changes (Martinez, Koeman & Allardyce). Silva compensation still to book in 2019/20. Also £19m new stadium costs, which can be capitalised once planning permission granted.

On the other hand, #EFC have increasingly relied on profit from player sales, which has averaged £53m a season over the last 3 years, compared to just £14m in preceding 7 years. Should also be fairly high in 2019/20, due to sales of Gueye, Lookman, Vlasic and Onyekuru.

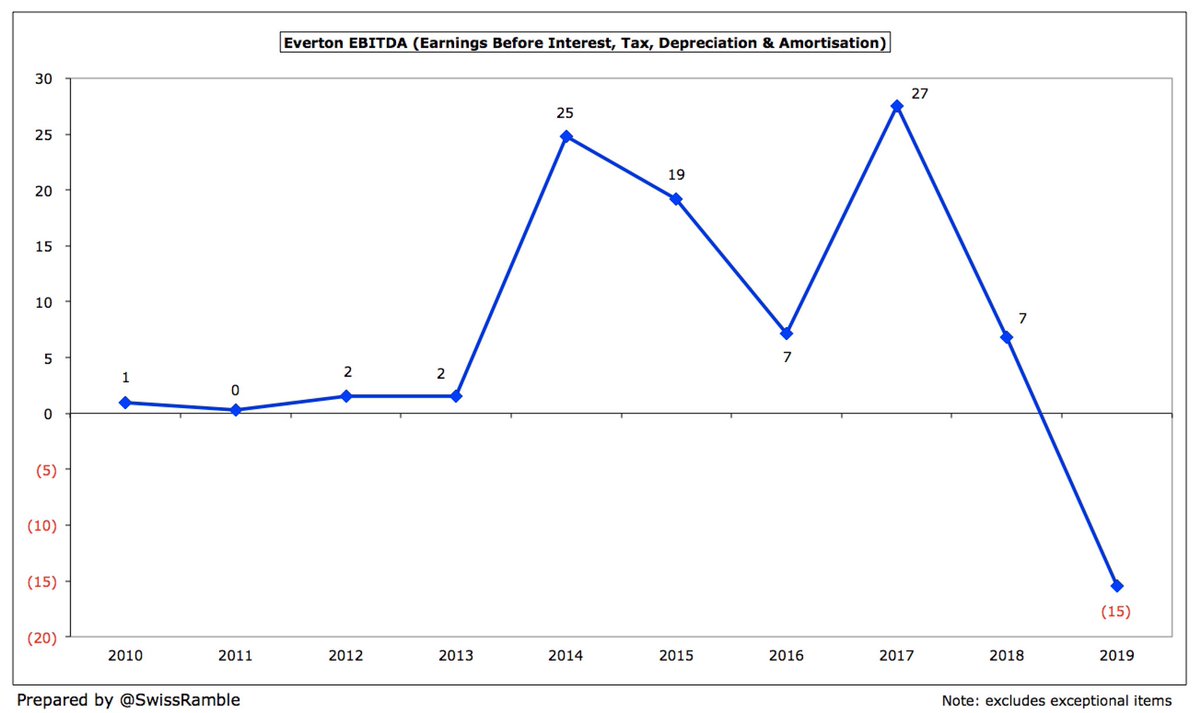

#EFC EBITDA (Earnings Before Interest, Tax, Depreciation & Amortisation), considered as a proxy for cash operating profit, as it excludes player sales and exceptional items, fell from £7m to £(15)m, down from £27m just two years ago.

#EFC £188m revenue is 54% (£66m) higher than £122m reported just 3 years ago. Vast majority of the growth (£50m) is due to higher Premier League TV deal, though commercial is also up £19m. Note: if outsourced catering/retail were included, revenue would be £7m higher at £195m.

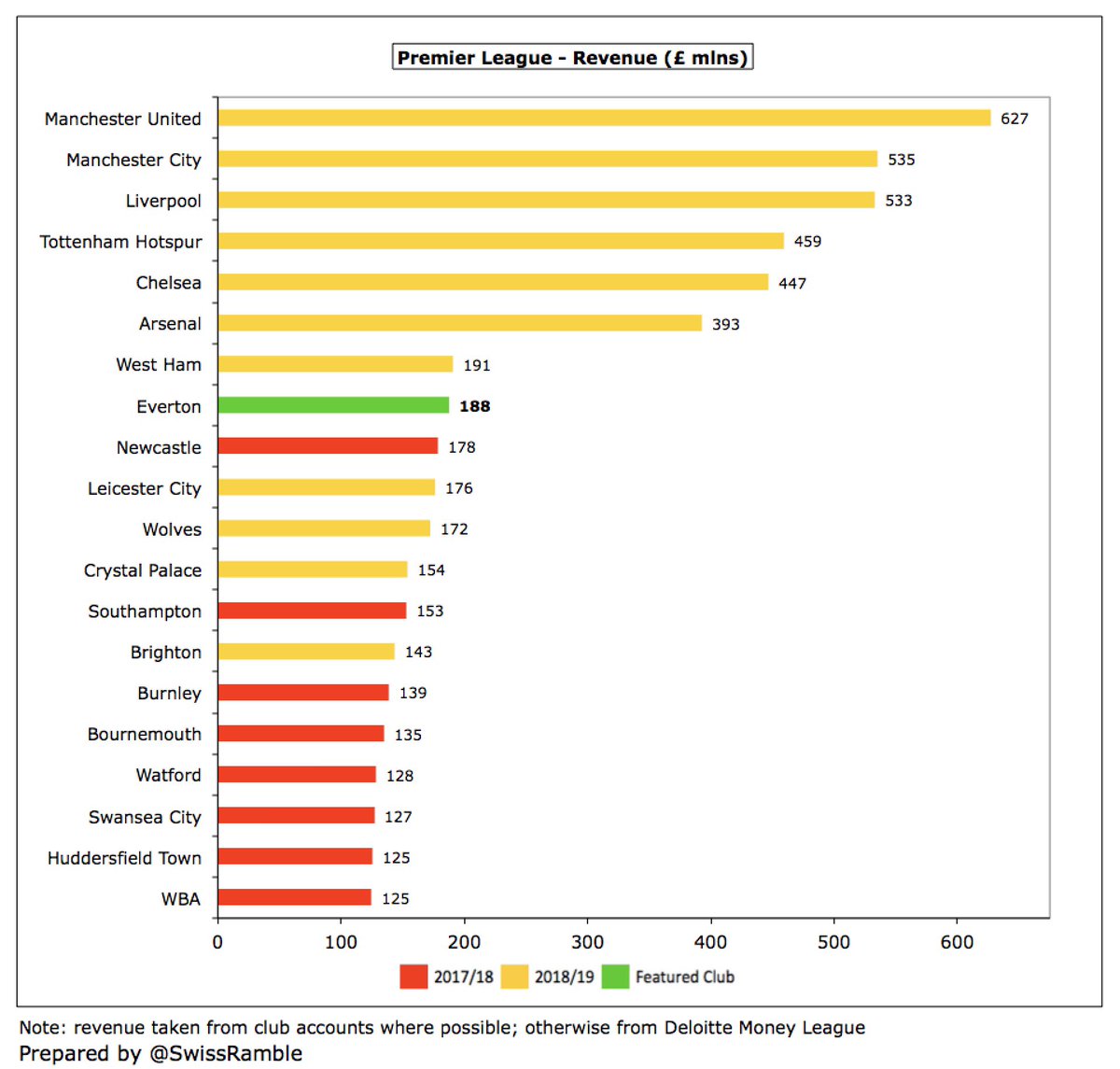

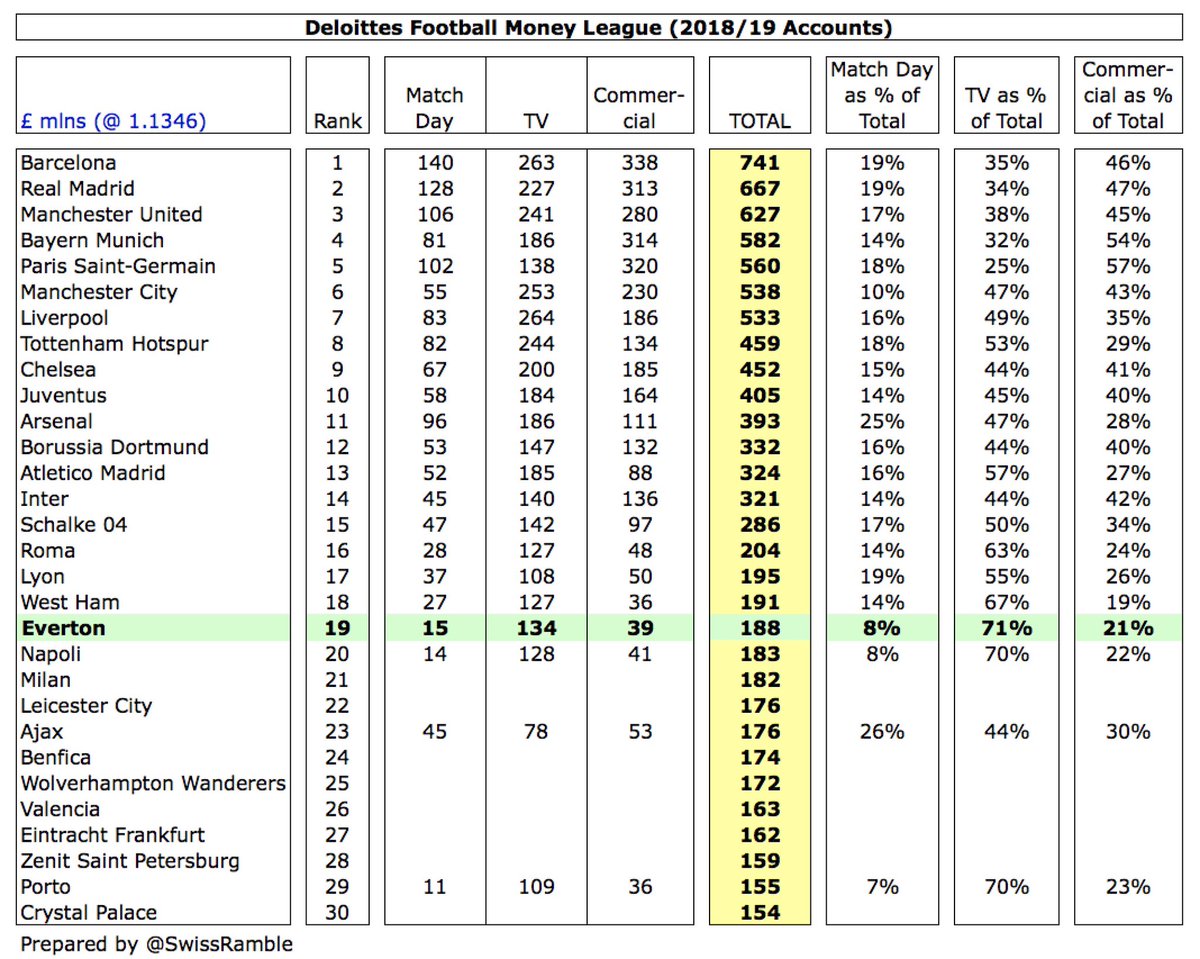

More positively, #EFC had the 19th highest revenue in the world per the Deloitte Money League, though they did drop two places and were one of only two clubs in the top 20 not to generate any revenue growth in 2018/19.

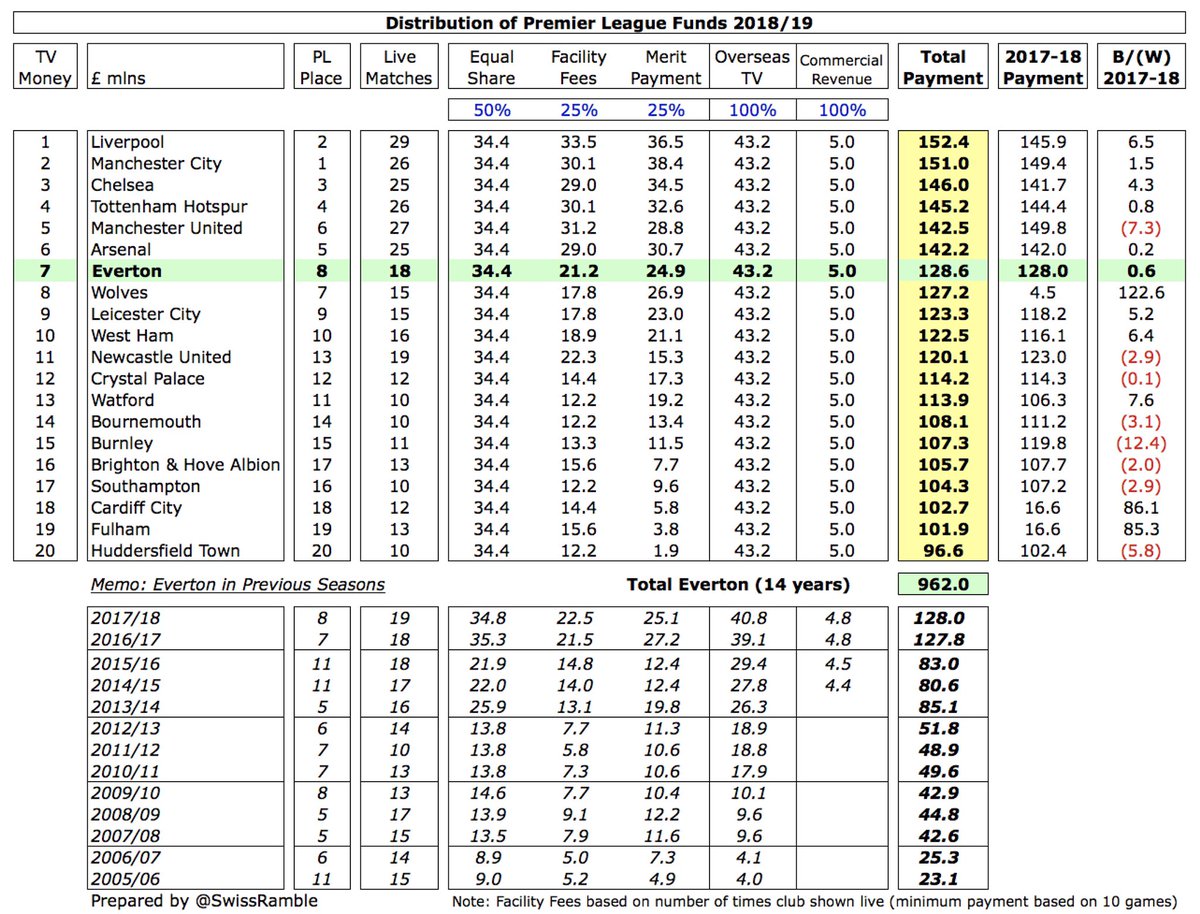

#EFC £129m Premier League TV money was slightly more than the previous season, as lower facility fees £1m (team broadcast live 18 times vs. 19) were offset by higher overseas distribution £2m. Club has received £962m from the Premier League in the last 14 years.

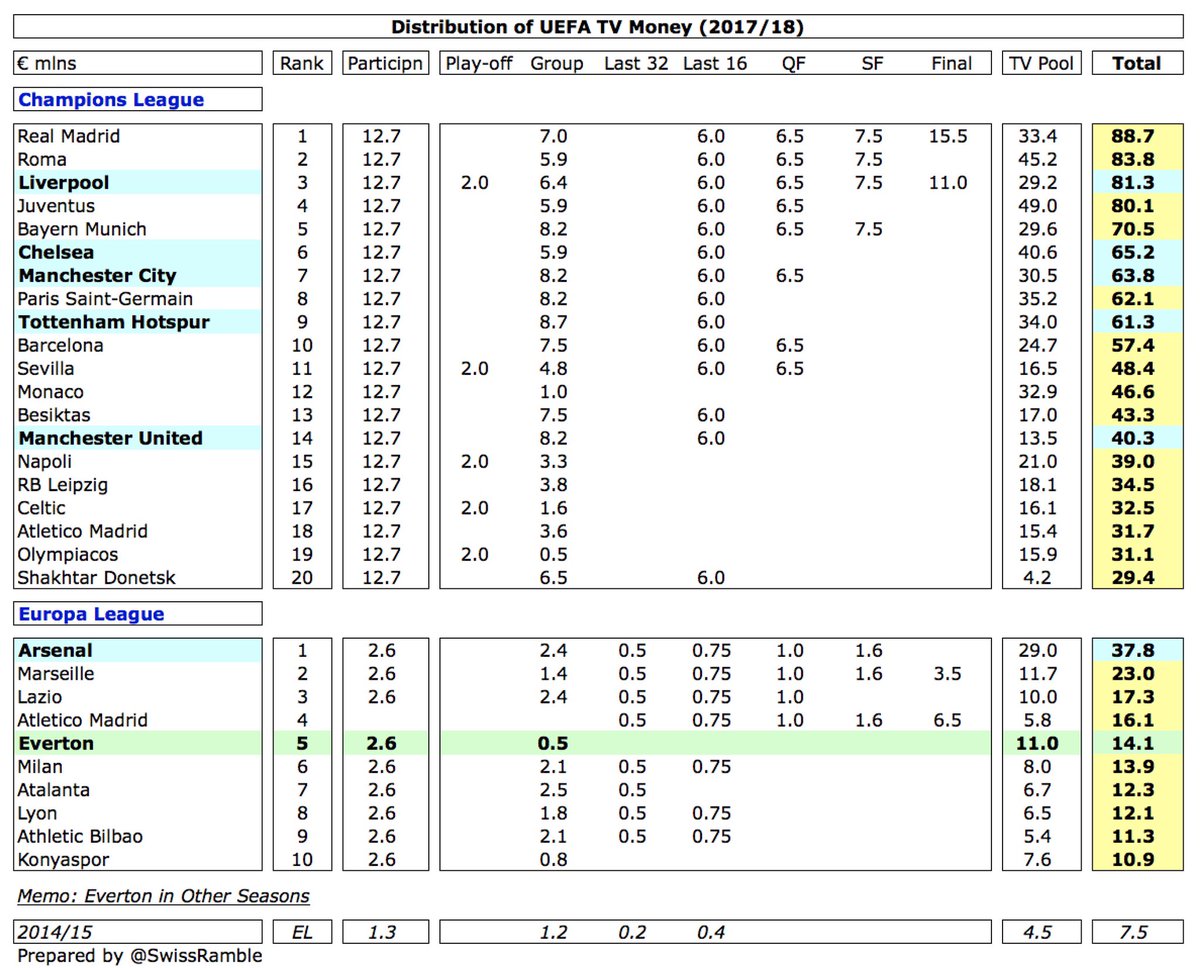

#EFC 2018/19 revenue suffered a €14m reduction after failing to qualify for the Europa League, which CFO Sasha Ryazantsev said, “demonstrated why regular European football is so important for us financially”.

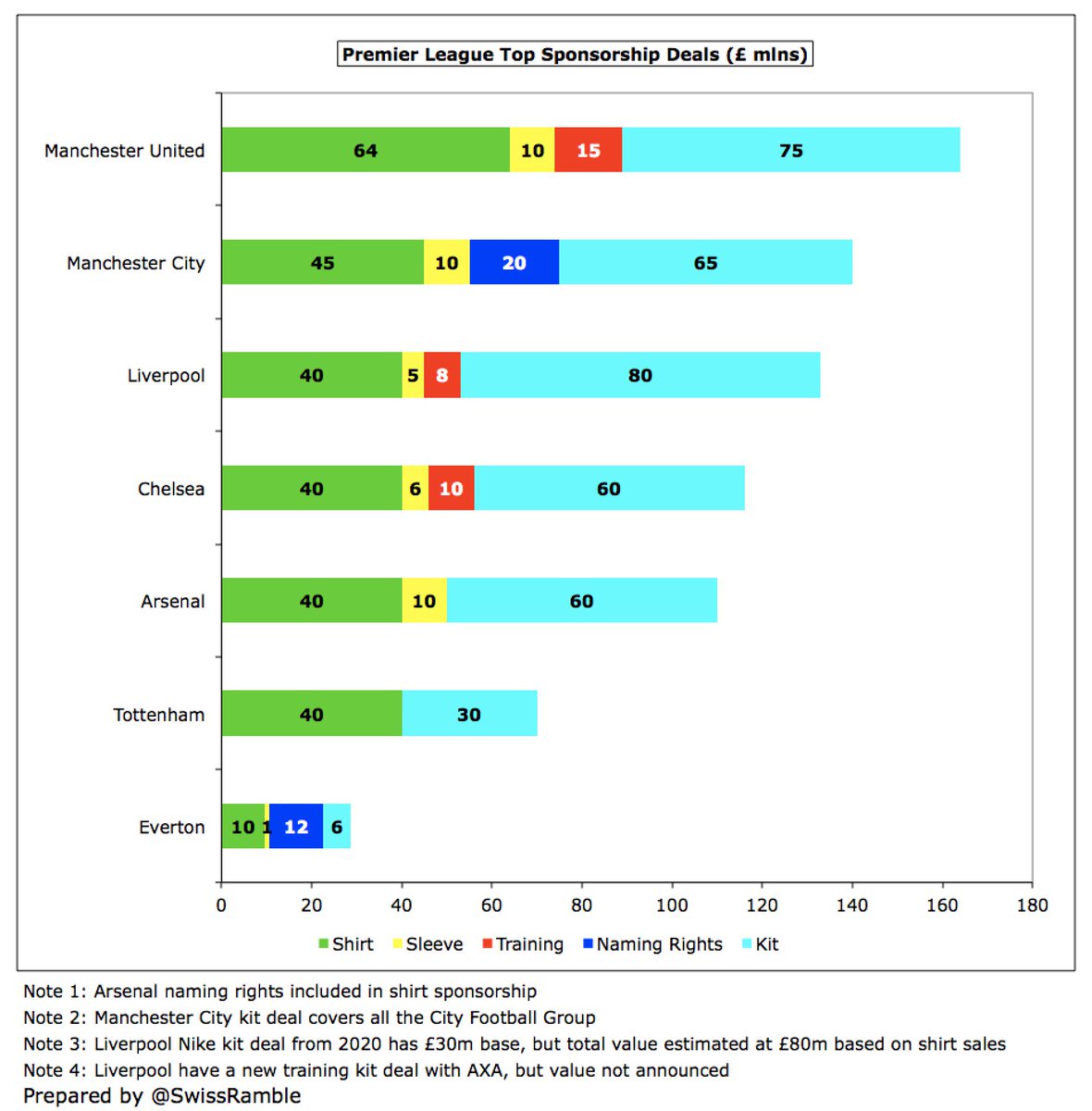

In 2018/19 #EFC training ground naming rights deal with USM Holdings (where majority owner Farhad Moshiri is a shareholder) doubled from £6m to £12m. Deals with SportPesa (shirt), Umbro (kit) and Angry Birds (sleeve) are reportedly worth £9.6m, £6m and £1m a year respectively.

#EFC have also announced an “innovative” deal whereby USM will pay £30m for an option to buy naming rights for the new stadium at a pre-agreed price and term. Note: this is not for the naming rights, but just an option for first refusal. Premier League will scrutinise the deal.

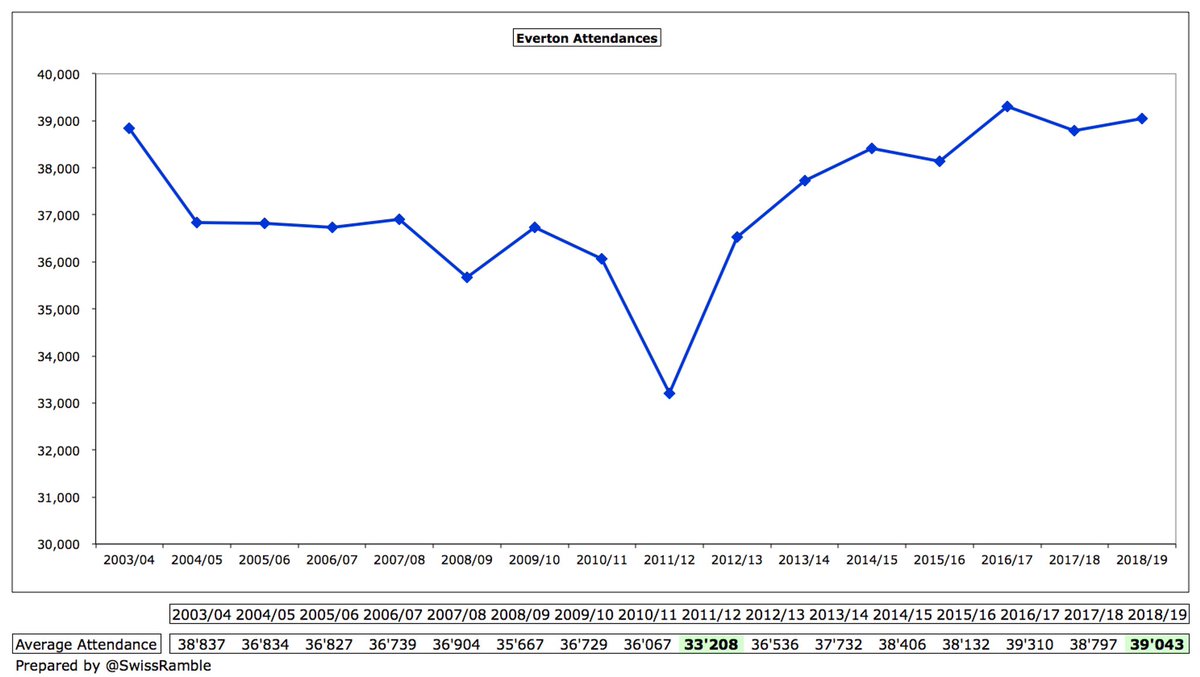

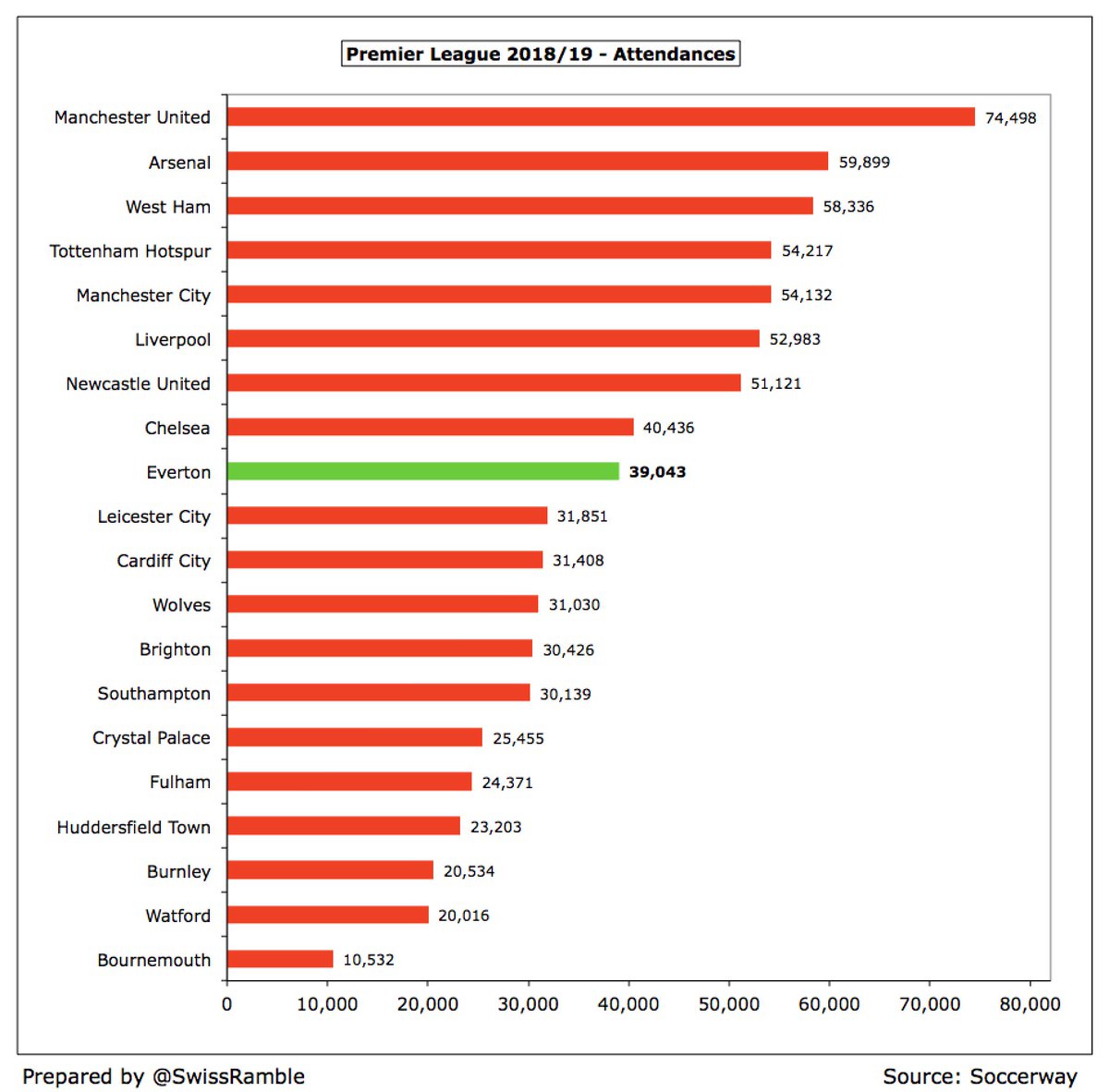

#EFC average attendance rose slightly from 38,797 to 39,043, representing a sellout of all home tickets at Goodison Park. This was still 5,800 (18%) higher than the recent low of 33,208 in 2011/12. Some of cheapest ticket prices in Premier League – frozen for 5 consecutive years.

#EFC average attendance of around 39,000 was the 9th highest in the Premier League, only surpassed by the Big Six plus West Ham (Olympic Stadium) and Newcastle United. Season tickets have reached the cap with more than 10,000 on the waiting list.

#EFC have recently submitted the planning application for a new 52,000 capacity stadium at Bramley Moore Dock. CFO Ryazantsev underlined its importance: The stadium is paramount for our long-term success as a football club.” Cost estimated at £500m.

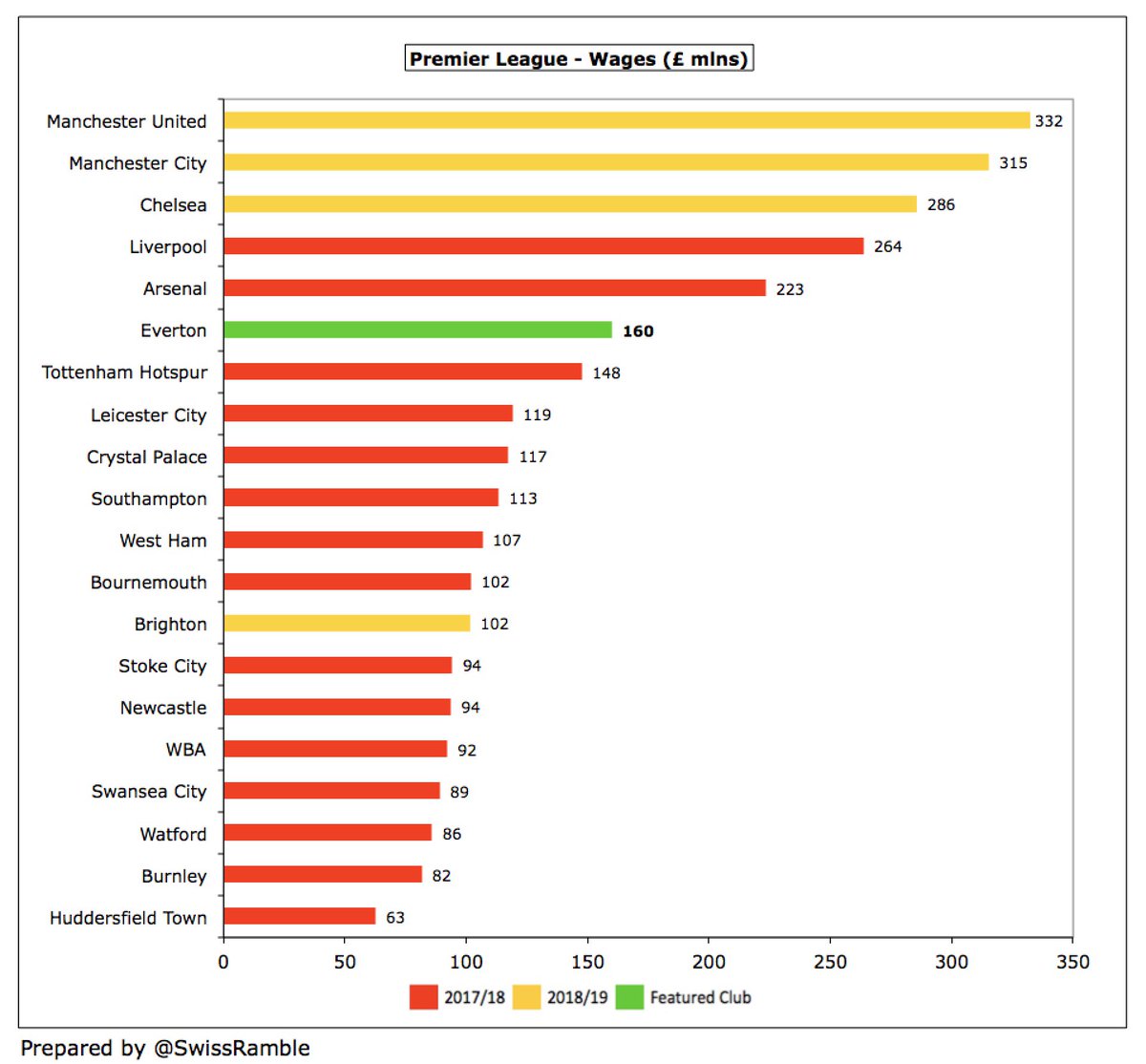

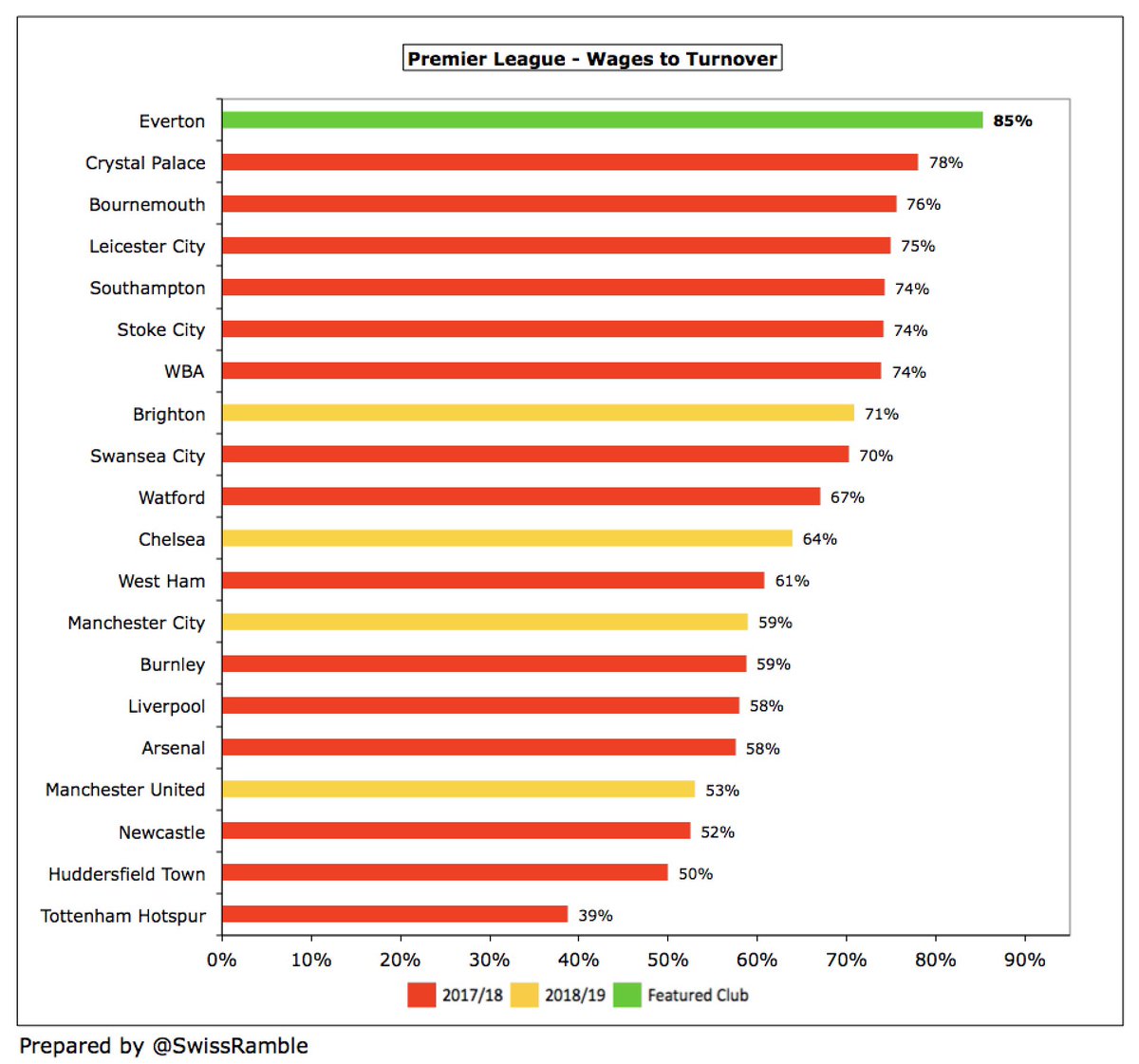

#EFC wage bill rose almost £15m (10%) to £160m, due to significant investment in the squad, despite number of players and management falling from 172 to 151, with wages to turnover ratio worsening from 77% to 85%. Wages are up by incredible £76m (90%) from £84m in last 3 years.

Following increase, #EFC wages to turnover ratio of 85% is the highest (worst) in the Premier League, though “artificially inflated” by additional month in 13 month reporting period. Adjusting for this factor plus outsourced catering & retail revenue, ratio would reduce to 76%.

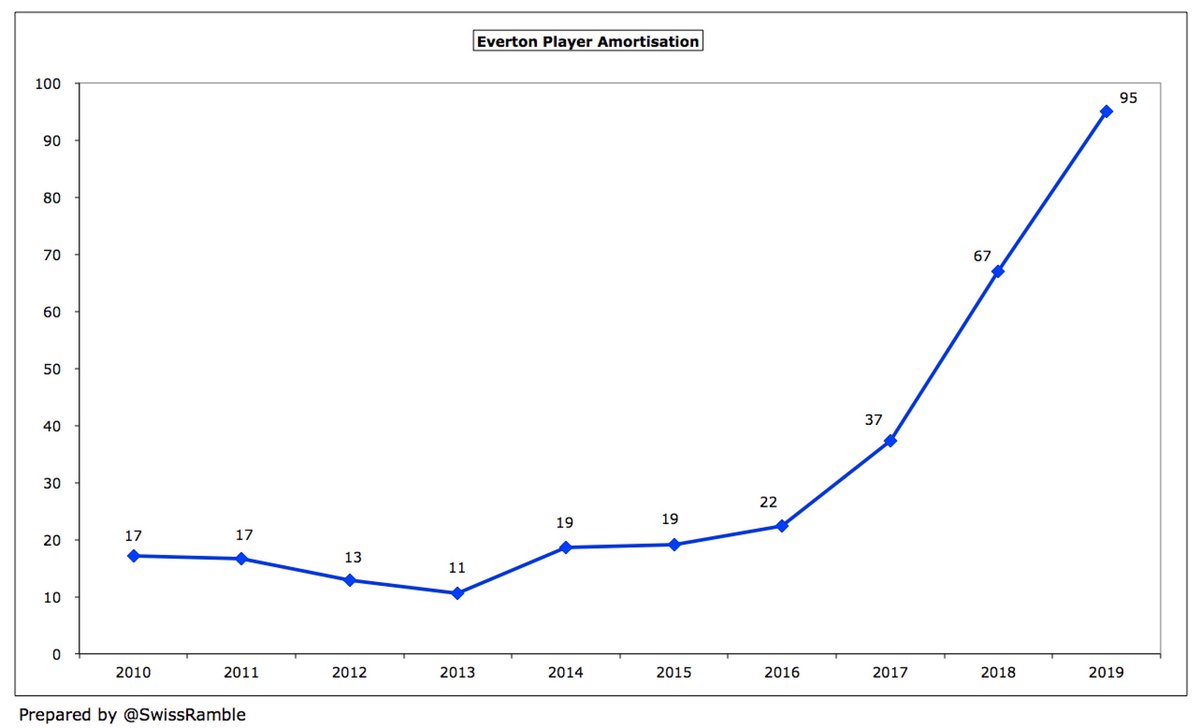

#EFC player amortisation, the annual charge to expense transfer fees over the length of a player’s contract, shot up £28m (42%) from £67m to £95m. More than quadrupled in 3 years, though £8m due to additional month from change in year-end. Player impairment down £6m to £3m.

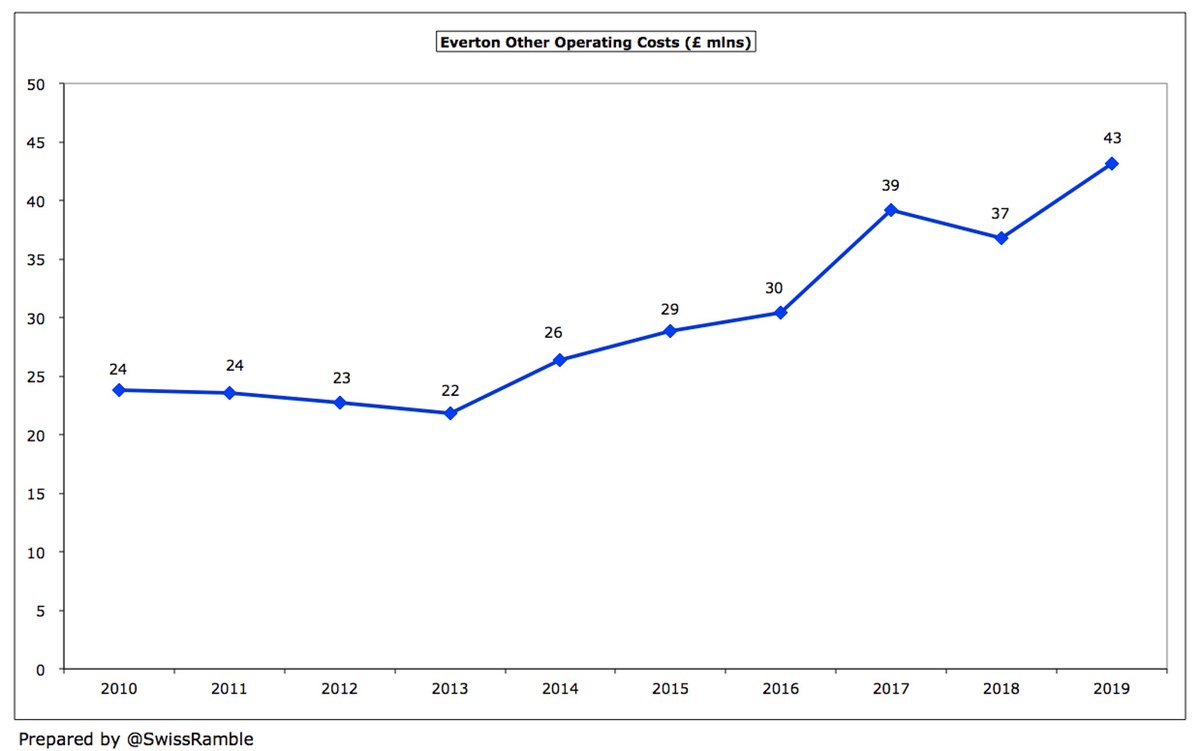

#EFC other operating costs rose £6m (17%) from £37m to £43m, driven by additional month from the change in year-end plus no repeat of previous year’s rebates received for players injured on international duty. These have basically doubled since 2013.

Since Moshiri’s arrival, #EFC have been far more active in the transfer market. In the last 3 seasons they averaged £127m gross spend, more than double the £53m average in the preceding 3 seasons. Over the same period, net spend has increased from £30m to £56m.

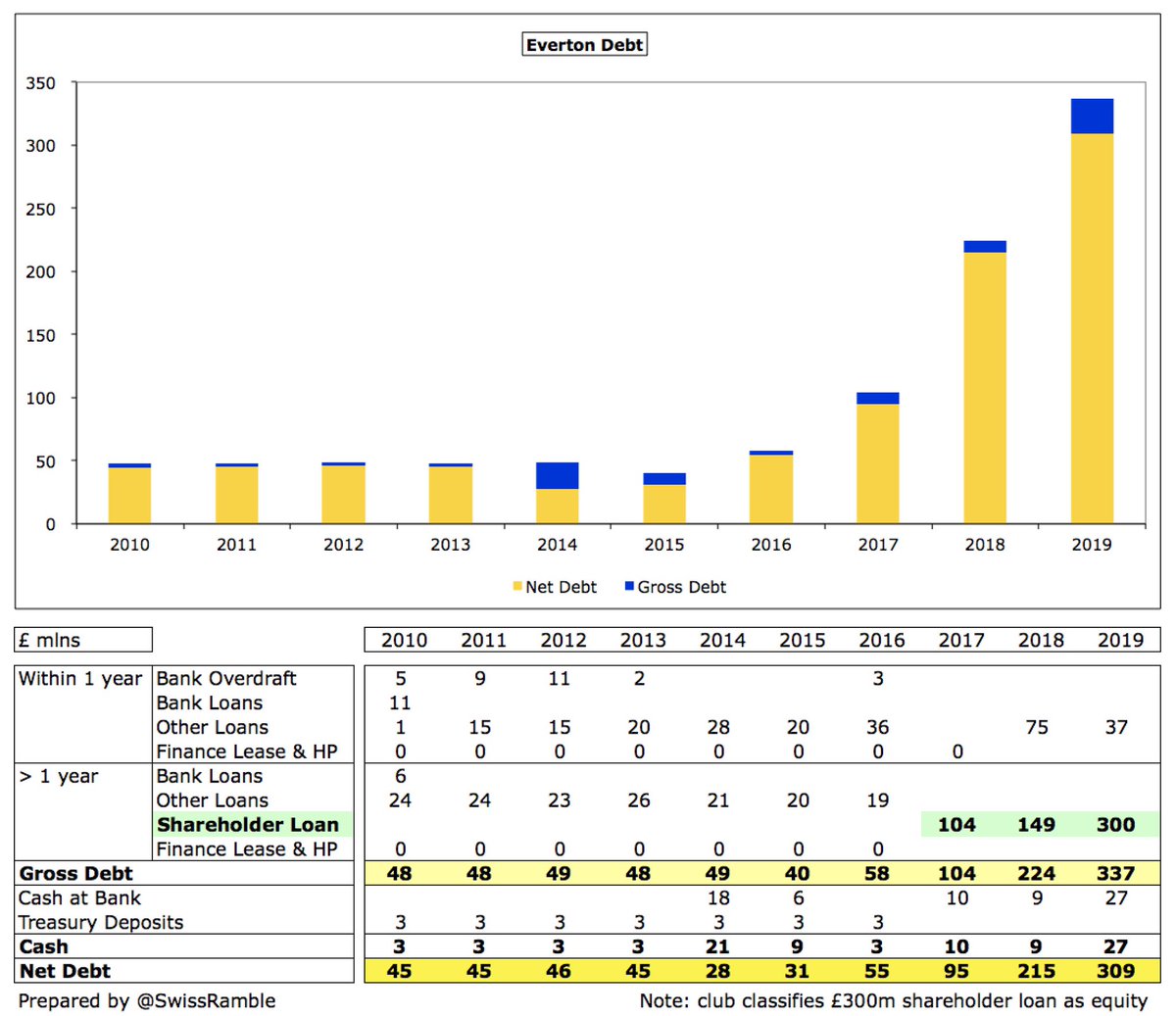

Per #EFC gross debt was cut from £75m to £37m, repayable in July 2019 and July 2020 at an interest rate of 3.5%. Everton classify the £300m interest-free loan provided by owner Moshiri as equity, as no agreed repayment date, but other clubs treat such friendly loans as debt.

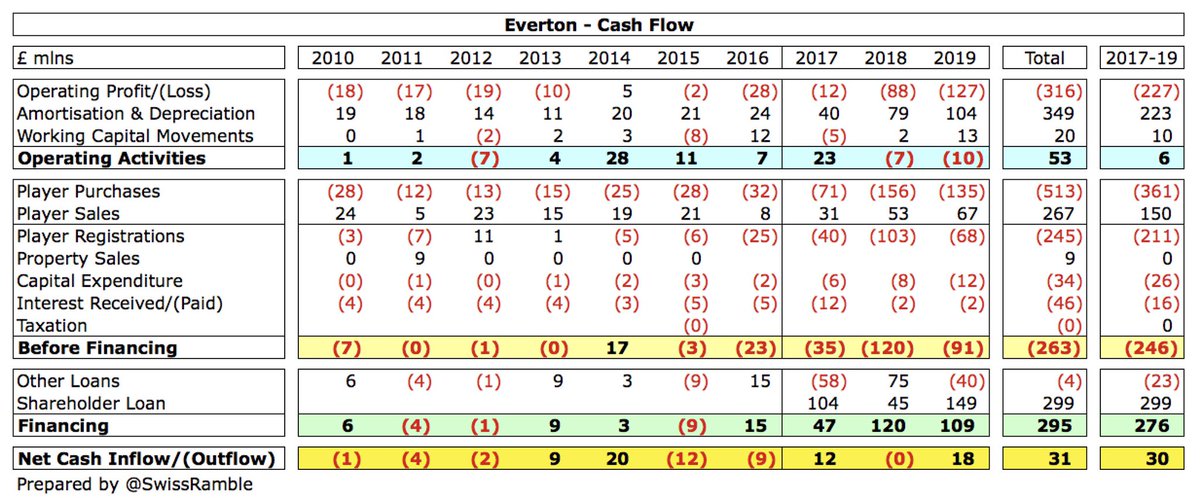

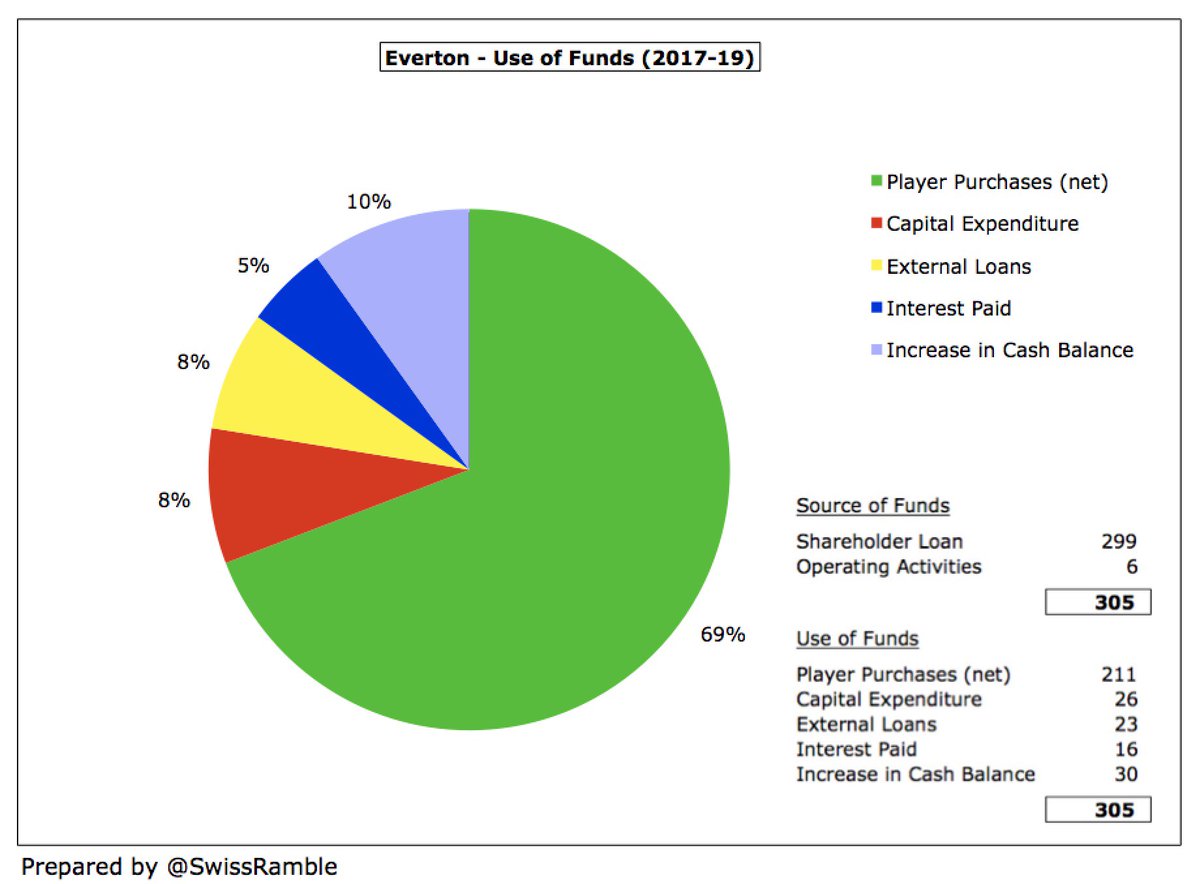

In 2018/19 #EFC had £10m negative cash from operations before spending £68m (net) on players, £40m repaying external debt, £12m on stadium and training ground and £2m interest, leading to a £131m cash deficit. This was funded by a £149m additional loan from Moshiri.

In the last 3 years #EFC available cash of £305m was almost entirely provided by loans from Moshiri. The vast majority of this (£211m) has been used to improve the squad, while £26m went on capex, £23m external loans and £16m interest payments.

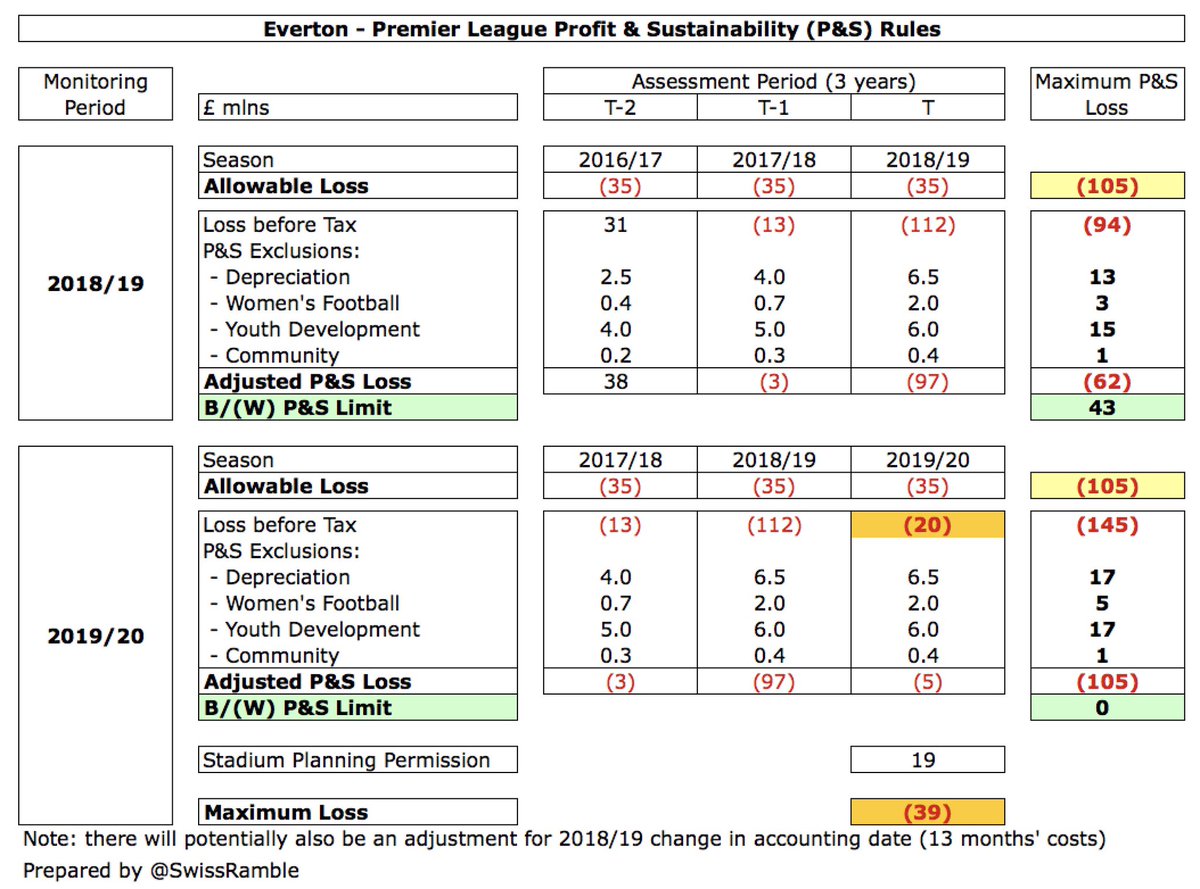

#EFC hefty loss has raised concern over the Premier League’s Profitability and Sustainability rules. These allow £105m loss over 3 years, so club is currently fine, as reported losses are only £94m, even before deductions for depreciation, women’s football, youth & community.

However, this season #EFC will lose £31m profit from 2016/17, so it is more challenging. My estimate is that club can only afford £20m loss in 2019/20, though they would be able to capitalize £19m stadium costs if planning permission is given before end-June, meaning £39m loss.

#EFC might also be able to make an adjustment in their Profitability and Sustainability submission to reduce their 2018/19 expenses for the impact of the additional month arising from change in year-end. Otherwise, they will need to make more player sales.

Since these accounts were finalised, the owner has added a £50m loan, which means he has provided £350m of funding (on top of the price he paid for his shares). Little wonder that chief executive Barrett-Baxendale said, “Mr. Moshiri’s investment has been vital and impactful.”

The #EFC CEO justified the noteworthy loss, “We want to challenge at the very top of the game, but in the modern Premier League-era it is extremely difficult to permanently break the virtuous cycle enjoyed by the richest teams in our league without this period of investment.”