There have been lots of cynical takes after our analysis showing a 4% increase in China’s CO2 emissions on the first quarter - a lot of people who ‘always knew’ that fall in China’s coal use and CO2 emissions was just a blip. -THREAD unearthed.greenpeace.org/2018/05/30/chi…

Let’s look at the trends and drivers of coal use and CO2 in China over the past decade to understand what is a blip and what isn’t.

China’s economy is exceptionally reliant on capital spending and smokestack industries. This is a key factor in China’s extremely high CO2/GDP ratio - CO2 per capita exceeds EU with 1/4 of the GDP per capita.

Accordingly China’s CO2 emissions are overwhelmingly driven by a few heavy industry sectors - metals, cement, chemicals industries use 2/3 of all coal. Demand for these products is almost entirely driven by domestic construction boom.

The distorted economic structure and need to rebalance were recognized by premier Wen already in 2007. Before there was time for recognition to turn into action, the global financial crisis saw China’s exports tank and the government respond with a ginormous stimulus program.

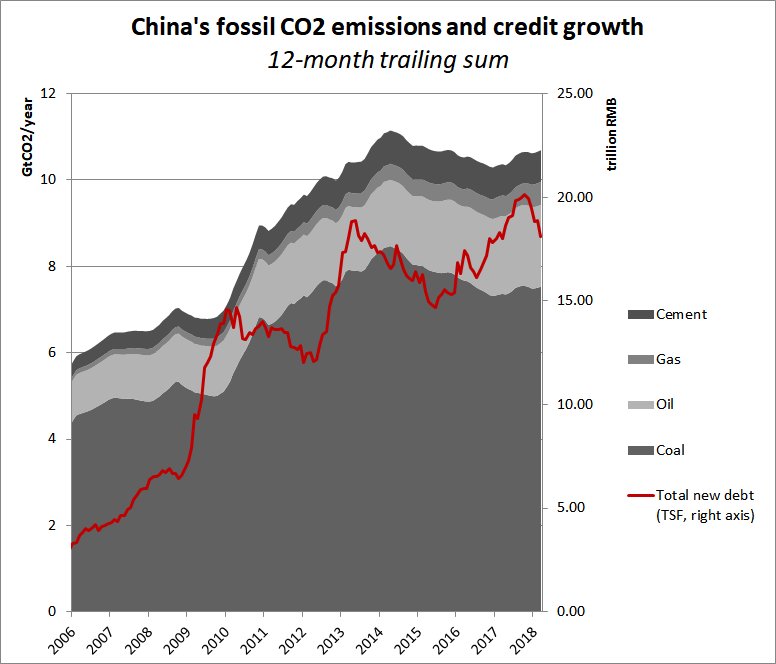

After the global financial crisis, investment in China is increasingly a way to maintain industry and construction volumes and local government revenues, not driven by need for new real estate, infrastructure or industrial capacity.

The 2013-2016 fall in Chinese emissions was real. It resulted from an attempt to withdraw stimulus under the slogan of “New Normal”.

The resulting slowdown was faster and more painful than expected, and revealed how strongly the system is dependent on growing capital spending and increasing debt. With the Party Congress approaching, there was no space for this painful process - another wave of stimulus ensued.

Every Party Congress has been preceded by an investment boom to prop up GDP before performance evaluations and promotions of party cadres. However, we'd hoped that with more attention on financial deleveraging and “high-quality” growth, there would be less incentive to do this.

The share of investment in GDP stopped falling last year, showing how economic rebalancing took a step backwards

Now, with the Party Congress and the Two Sessions behind, this year is the window to resume economic rebalancing. Credit growth seems to have peaked in late 2017, which will likely start weighing on construction and industrial activity later this year.

How the government responds will be a strong indication of the outlook for rebalancing the economy.

Some experts understand this dynamic: “as the economy undergoes structural changes, investment in infrastructure is set to decline, leaving fewer drivers for significant increases in carbon emissions in the future” -Jiang Kejun, Energy Research Institute

chinadialogue.net/article/show/s…

chinadialogue.net/article/show/s…

Zhou Dadi, former head of Energy Research Institute: "Currently, a lot of investment is inappropriate and blind. Energy-intensive industries are still expanding … This triggered a rebound in coal consumption." ideacarbon.org/archives/50738

Zhou Dadi: "China’s development so far has been based on this kind of [blind] expansion, but now it needs new drivers. From the perspective of housing construction and infrastructure construction, it is reasonable to achieve peak emissions by 2025."

ideacarbon.org/archives/50738

ideacarbon.org/archives/50738

55% of carbon market stakeholders interviewed for “2017 China Carbon Pricing Survey” think China’s CO2 emissions will peak before 2025.

ideacarbon.org/archives/50738

ideacarbon.org/archives/50738

There are also clear signs the Chinese government is prepared to target an earlier peak:

To recap: China’s CO2 emissions are dominated by industry, and demand for energy intensive industry is predominantly driven by fixed asset investment. Maintaining current levels of “investment” will lead to increasingly obvious problem of wasted and non-productive investment.

The fall in emissions 2013-2016 showed what happens when debt is curtailed. China’s emissions will only stay high as long as the state channels resources into marginally productive construction and other activity needed to maintain absurdly high levels of steel, cement etc demand

Maintaining clean energy growth while modernizing the country’s economic structure holds major potential for peaking and declining emissions fast. None of this is a given but it is a very real possibility.

Yes we are in an emergency. Only way to have hope of averting a full-on climate catastrophe is for global emissions to not only plateau but start falling, fast. China is by far not the only reason this is not happening - very few countries are pulling their weight.

EU CO2 emissions went up in 2017 while reductions slowed down in the U.S. We need to do a lot better. Over.