,

15 tweets,

4 min read

Read on Twitter

ICYMI: I was on WDYM yesterday discussing some potentially major changes to how we look at and think about labor markets and inflation

Some big points that are highlighted from my piece:

1. Canada’s labor market appears to be historically tight. Not true in the US. Nevertheless, no signs of inflation acceleration in Canada. We really should’ve seen something sustained by now at least

medium.com/@skanda_97974/…

1. Canada’s labor market appears to be historically tight. Not true in the US. Nevertheless, no signs of inflation acceleration in Canada. We really should’ve seen something sustained by now at least

medium.com/@skanda_97974/…

This simplistic visualization highlights the problem with using the unemployment rate. The household survey struggles to distinguish between who’s unemployed and who’s not participating in the labor force

The unemployment rate relies on that distinction being well-measured. It is not.

For that reason alone, we should be using employment rates, which are simply employment divided by population (no labor force participation distinction needed)

For that reason alone, we should be using employment rates, which are simply employment divided by population (no labor force participation distinction needed)

Of course, with employment rates, a demographic adjustment is more necessary. But totally feasible. Prime-age employment rates show why US is not historically tight like Canada:

Canada is a better example of pushing the boundary on labor mkt tightness. Their headline unemployment rate is at the historic lows. Their prime age employment rate is at the historic highs (has been for two years!)

Show me the price acceleration!

Show me the wage acceleration!

Is there a fixed limit on labor utilization in the context of price stability? Honestly, we’ll never know because so much of this ends up being unfalsifiable...you can always claim that equilibrium paepop was higher than you previously anticipated

But when you make persistent one-sided errors...

When your model fails to be useful neither at the more well-traveled points nor the more extreme ones...

When your model fails to be useful neither at the more well-traveled points nor the more extreme ones...

I think we should be thinking less about a fixed cap on labor utilization. Start thinking more about the speed limit to achieving a tighter labor market, and less about a sticky constraint on the level itself

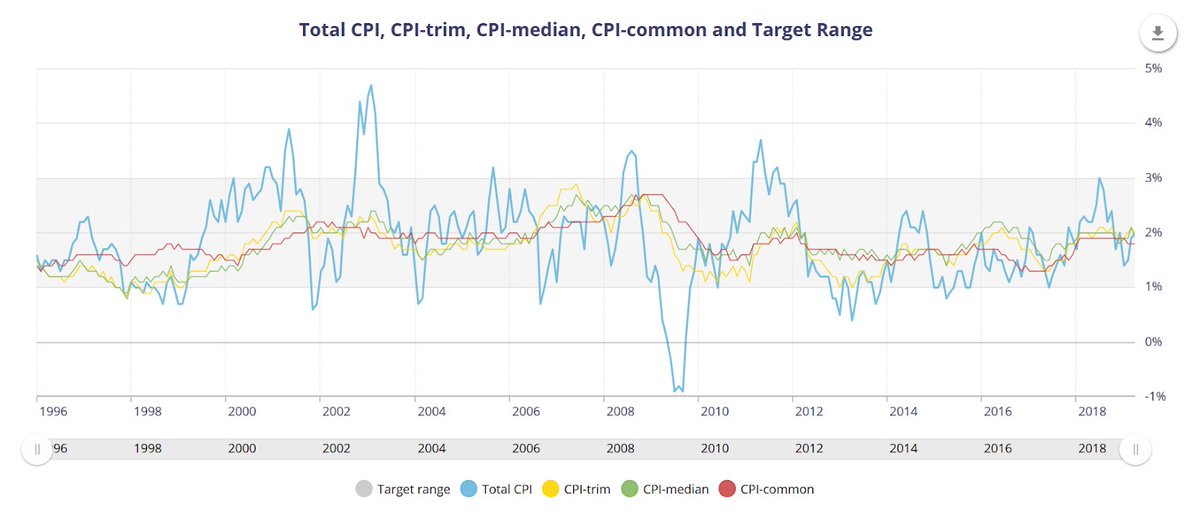

There are a lot of well meaning Phillips Curve believers (Krugman, Yellen) who rightly point out that inflation tends to fall sharply after the unemployment rate rises. It is true that both capture cyclical dynamics and policymakers should care

But many of the bulky cyclical segments of inflation are actually more correlated to the change in labor utilization than the level itself. No model explains everything but food for thought (more analysis to be done)

Some folks who have an especially dim view of active policymaking like to dunk on Phillips Curve believers with evidence like this.

But let’s not forget the other side:

Monpol over the last 10yrs has shown more ability to support labor markets than affect inflation itself!

But let’s not forget the other side:

Monpol over the last 10yrs has shown more ability to support labor markets than affect inflation itself!

The tradeoff we are told from the beginning of econ 101 is just not empirically robust. Two drivers:

1. Simplistic tradeoff b/w employment and inflation

2. Emphasis on longer-run monetary neutrality (supposedly only employment can be affected in short run, prices in long run)

1. Simplistic tradeoff b/w employment and inflation

2. Emphasis on longer-run monetary neutrality (supposedly only employment can be affected in short run, prices in long run)