,

53 tweets,

13 min read

Read on Twitter

Elmer Terminal Q2 Tesla Earnings Preview, entitled:

Never Bet Against Elon™️

or,

I Promise I'm Not A Bull But We Should All Try To Think Like One Sometimes

or,

Please Don't Put Me On The BlockList This Is Just a Mental Exercise

0.1/many

$tsla $tslaq

Never Bet Against Elon™️

or,

I Promise I'm Not A Bull But We Should All Try To Think Like One Sometimes

or,

Please Don't Put Me On The BlockList This Is Just a Mental Exercise

0.1/many

$tsla $tslaq

A few days ago I wrote an initial take on the deliveries report. In that thread I suggested that I thought that the god-king would be able to build a decent story (for his lemmings and the slightly less lemming Baggie Gifs of the world) to eat up:

0.2/

0.2/

My expectations of a positive reaction (in SP) were a bit off (thankfully). Despite rumors to the contrary, I still wish nothing but failure upon the god-king and nothing but destruction upon the $tsla SP. $tslaq might as well be tatted on my face bros.

0.3/

0.3/

That being said, it's important to not out-lemming the lemmings so you gotta take a step back and 1) think about what can go wrong with the $tslaq thesis and 2) try to think like elon himself i/r/t how can one polish a turd (not even a turd, more like a can of wet catfood).

0.4/

0.4/

So of course I'm talking about Q2 results.

Which I think will be much better than the current $tslaq consensus and probably in-line with analyst estimates (pasted below; i'm a lowly peasant using Yahoo finance so I don't know if Factset has more recent numbers.).

0.5/

Which I think will be much better than the current $tslaq consensus and probably in-line with analyst estimates (pasted below; i'm a lowly peasant using Yahoo finance so I don't know if Factset has more recent numbers.).

0.5/

...because this thread is going to contain some what ifs for the bull case, I'll also try to keep all of my $tslaq goons from hitting block out of frustration by pointing out the bear case/base case mitigating points. Again, this is a thought exercise more than a prediction.

0.6

0.6

...and as always PLEASE feel free to point out mistakes and rebut as appropriate. This is a sharing and learning experience that kimbal would be proud of.

OK enough preamble lets get into it. Thoughts may jump around, apologies in advance.

0.7/

OK enough preamble lets get into it. Thoughts may jump around, apologies in advance.

0.7/

POSITIVE POTENTIAL DEVELOPMENT 1:

ASP may not be as bad as some think.

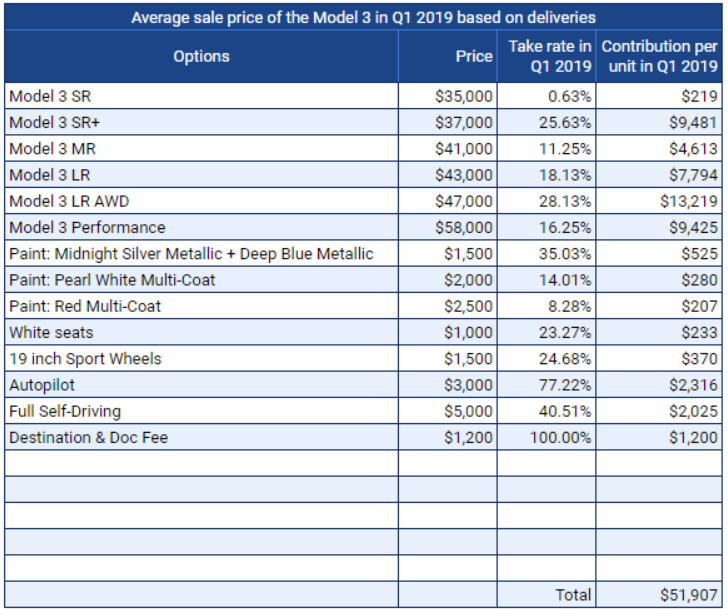

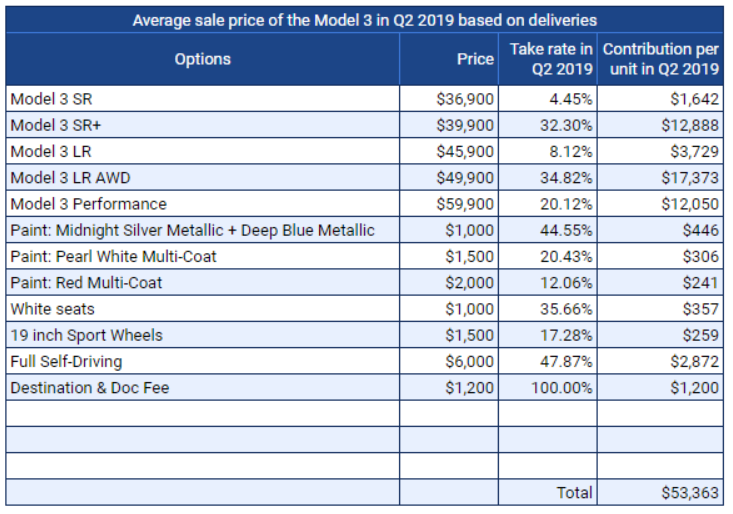

As noted earlier today, @TroyTeslike's Model 3 order tracker indicates that Model 3 ASP **INCREASED** from Q1 to Q2.

This is primarily due to mix and FSD uptake.

$tsla $tslaq

1a/

ASP may not be as bad as some think.

As noted earlier today, @TroyTeslike's Model 3 order tracker indicates that Model 3 ASP **INCREASED** from Q1 to Q2.

This is primarily due to mix and FSD uptake.

$tsla $tslaq

1a/

FSD uptake shouldn't do much to affect reported revenue in Q2 as long as $tsla doesn't change rev rec policies substantially in Q2. As of Q1, nearly all of that revenue was still being deferred.

But that's a big honeypot that can be tapped should Elon ever want to.

1b/

But that's a big honeypot that can be tapped should Elon ever want to.

1b/

Mix improvement (or, if you want to take a middle road, stabilization) makes sense to me IMO. As noted in the earlier thread, bad-good-best is probably the oldest sales/marketing strategy in the book.

Removal of MR and LR RWD means more LR AWD and P purchases.

1c/

Removal of MR and LR RWD means more LR AWD and P purchases.

1c/

Additionally (and you'll have to believe me on this, it's late and i'm too lazy to dig up links), anecdotally (but also as demonstrated by S unit decline), IMO a lot of would-be USED or even NEW S buyers are trading down to P3D... simply a better value.

$tsla $tslaq

1d/

$tsla $tslaq

1d/

Further (and troy's trackers for this aren't as active), I'd expect S/X pricing to be a bit stronger than some $tslaq may expect.

S is a dog, no doubt about that. I myself was posting plenty of screenshots of LRs going for $7x,000 until they sold out.

1e/

S is a dog, no doubt about that. I myself was posting plenty of screenshots of LRs going for $7x,000 until they sold out.

1e/

However, X pricing didnt really seem to be discounted (and unit sales of that model appear to be much stronger).

Both models' ASPs will be hurt by the free luda promo that $tsla ran this quarter, and S was heavily discounted, but overall I don't expect a total cratering.

1f/

Both models' ASPs will be hurt by the free luda promo that $tsla ran this quarter, and S was heavily discounted, but overall I don't expect a total cratering.

1f/

FurtherMORE,

as I was doing some miscellaneous reading earlier today,

I noticed this clause in the Q1 investor letter.

Could be the god-king babbling.

But if its bona fide, even 1,000 or so delayed S/X P's pushed from Q1 into Q2 will do much to help ASPs.

1g/

as I was doing some miscellaneous reading earlier today,

I noticed this clause in the Q1 investor letter.

Could be the god-king babbling.

But if its bona fide, even 1,000 or so delayed S/X P's pushed from Q1 into Q2 will do much to help ASPs.

1g/

"alright enough FUD elmer"

mitigating points on potential good ASP:

1) on-the-ground data in the US appears to show a weaker 3 mix than is reported in Troy's sheet. Many more SR+ (and also, prob a ton of those into CA since that was the moneycar in terms of incentives).

1h/

mitigating points on potential good ASP:

1) on-the-ground data in the US appears to show a weaker 3 mix than is reported in Troy's sheet. Many more SR+ (and also, prob a ton of those into CA since that was the moneycar in terms of incentives).

1h/

1a) that could very well make sense as Troy's tracker likely captures more enthusiasts than normies. For example, I'd highly doubt that 8% of the 77k Model 3's sold in Q2 were of the mostly off-menu LR RWD flavor. So, take Troy's data as an upper bound, perhaps.

1i/

1i/

Additionally, S/X ASP could be weaker than this bull case, especially internationally. As noted earlier, I definitely saw a lot of great S deals through mid-quarter as they were selling through old stock. Who knows what they did to sell S/X in chiyna.

1j/

MOVING ON...

1j/

MOVING ON...

So *COST* is the other side of the equation. I'll look at this from a couple different angles. But (obviously) this feeds into GM and net income as well, so I want to lay a couple thoughts out there.

2a/

2a/

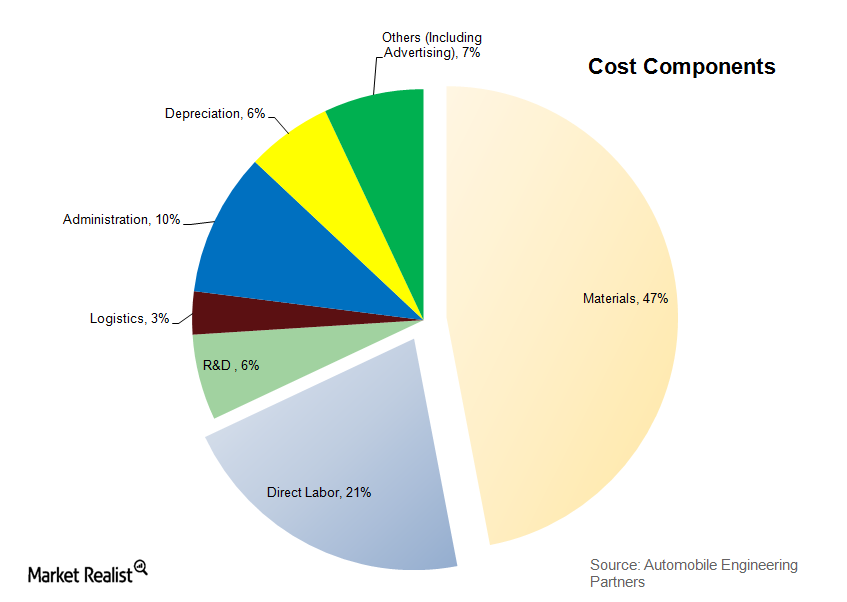

First, lets trigger myself and the rest of the accountants on here by taking it all back to managerial accounting.

(As my managerial accounting professor said, in his opinion, the failure of managers to understand managerial accounting led to unnecessary US outsourcing).

2a.5/

(As my managerial accounting professor said, in his opinion, the failure of managers to understand managerial accounting led to unnecessary US outsourcing).

2a.5/

To the uninitiated, the funnest part of managerial accounting is fixed vs. variable cost analysis.

I'm not going to get highly quantitative; I'd would rather keep this at a high level.

Attached is a chart on auto industry costs from marketrealist.com/2015/02/raw-ma…

2b/

I'm not going to get highly quantitative; I'd would rather keep this at a high level.

Attached is a chart on auto industry costs from marketrealist.com/2015/02/raw-ma…

2b/

This blog post is from 2015, and clearly doesnt relate to EVs or Tesla, but it's at least a jumping off point.

The takeaways that I'd like to bring your attention to are the relatively large pieces of the pie that are at least semi-fixed in nature: labor and overhead.

2c/

The takeaways that I'd like to bring your attention to are the relatively large pieces of the pie that are at least semi-fixed in nature: labor and overhead.

2c/

Why does this matter?

Because, when you go from making 63k Model 3's in Q1 to 73k Model 3's in Q2, fixed costs per car decline by ~15% (all else equal), which is going to provide a nice healthy margin boost to Tesla.

$tsla $tslaq

2d/

Because, when you go from making 63k Model 3's in Q1 to 73k Model 3's in Q2, fixed costs per car decline by ~15% (all else equal), which is going to provide a nice healthy margin boost to Tesla.

$tsla $tslaq

2d/

Also, I would wager that $tsla's labor costs per car are MUCH MUCH higher than industry averages.

I've seen lots of charts floating around on this but hard to find one; the attached is from a google image search behind a paywalled article from early 2019.

2e/

I've seen lots of charts floating around on this but hard to find one; the attached is from a google image search behind a paywalled article from early 2019.

2e/

That's representative enough to get the point across. If in the original pie chart labor is 20% of a car's cost, it's likely far more than that for Tesla (either direct labor in GM or overhead perhaps in SG&A). More cars = less allocated costs per car... periodt.

2f/

2f/

Oh man I've got max tweets in this thread so Twitter is making me break it up.

Enjoy this part 1 while I compose Part 2 (and 3 and 420?)

We shall resume at 2g, will try to figure out the best way to do this.

$tsla $tslaq

Enjoy this part 1 while I compose Part 2 (and 3 and 420?)

We shall resume at 2g, will try to figure out the best way to do this.

$tsla $tslaq

OK we're back.

Where were we?

Oh ya talking about labor costs.

ABOUT THOSE LABOR COSTS:

Lets not forget that America's #1 hypergrowth carmaker laid off ~4,000 people in January.

$tsla $tslaq

(ELMER 2Q ER THREAD CONTINUED)

2g/

Where were we?

Oh ya talking about labor costs.

ABOUT THOSE LABOR COSTS:

Lets not forget that America's #1 hypergrowth carmaker laid off ~4,000 people in January.

$tsla $tslaq

(ELMER 2Q ER THREAD CONTINUED)

2g/

That workforce reduction was *not* reflected in Q1 (still had expenses in native categories + restructuring expense).

Lets say the average all-in comp exp of those 4k laid off workers was $75k/yr (mostly plant, some white collar).

That's $300m/yr, $75k Q.

needle moving.

2h/

Lets say the average all-in comp exp of those 4k laid off workers was $75k/yr (mostly plant, some white collar).

That's $300m/yr, $75k Q.

needle moving.

2h/

Additionally, after in Mid-Q1 Tesla reduced hours on the S/X lines (teslarati.com/tesla-model-s-…), they further reduced shifts this quarter. (bizjournals.com/sanjose/news/2…)

That saves a lot of direct labor expense (which may happen not via layoffs but less OT).

$tslas $tslaq

2i/

That saves a lot of direct labor expense (which may happen not via layoffs but less OT).

$tslas $tslaq

2i/

The tweet escapes me, but our new Ska on-the-ground replacement remarked that the productivity exhibited by Tesla in Q2, esp. in regards to the Model 3, was unprecedented. They finally seem to have cleared some bottle neck. Generally speaking, that means lower costs.

2j/

2j/

And here's the big black box: material costs.

For this we'll return to The Miracle of Q3™️

Elon was building cars in a tent and repairing them in the desert, for a product line at ~60% of the ASP of the prior one, yet GM jumped 400 basis points. why?

2k/

For this we'll return to The Miracle of Q3™️

Elon was building cars in a tent and repairing them in the desert, for a product line at ~60% of the ASP of the prior one, yet GM jumped 400 basis points. why?

2k/

The answer, somewhat not that hard to figure out at the time but clearer after Q1 squabbling, as pana. Seems like they gave them a sweetheart deal in Q3/4 and then were sour in Q1 when Model 3 volumes fell off a cliff (or other issues arose).

2l/

2l/

I've looked at enough manufacturing companies in my various careers to know that rebates are a yuge part of the game.

Whats to say that a big concession/rebate/etc wasn't triggered in Q3 (leading to yuge margin improvement, >20% for Model 3), lost in Q1, and back now?

2m/

Whats to say that a big concession/rebate/etc wasn't triggered in Q3 (leading to yuge margin improvement, >20% for Model 3), lost in Q1, and back now?

2m/

Point being, price/mix isn't as great in Q2 as it was in Q3/Q4, but volume is also a huge driver of GM/profitability. Volume goes up, costs go down. You can't explain that.

I'd expect that auto GM clocks in at at least 20% this quarter. @DeanSheikh1 wanna bet?

2n/ NEW TOPIC

I'd expect that auto GM clocks in at at least 20% this quarter. @DeanSheikh1 wanna bet?

2n/ NEW TOPIC

OTHER COST MATTERS (section 3)

we at $tslaq love to laugh at the lemmings suffering but there's a reason for the madness.

Tesla, despite just raising $2b, is pinching every penny right now.

Is it bc they're short on cash? no.

It's because god-king wants to burn shorts.

3a/

we at $tslaq love to laugh at the lemmings suffering but there's a reason for the madness.

Tesla, despite just raising $2b, is pinching every penny right now.

Is it bc they're short on cash? no.

It's because god-king wants to burn shorts.

3a/

Again, I apologize for being a bit lazy this late into the evening, but please accept my anecdotes as accurate... the hours i've put into message board trawling deserve some respekt.

3a.5/

3a.5/

In Q2, we have seen Tesla:

1) start making people pay for diagnosis of issues during warranty period. ~$1-200 a pop.

2) Refuse to replace yellowing S/X screens.

3) hit the credit cards of people who are supposed to have unlimited supercharging

4) not improve parts waits.

3b.1/

1) start making people pay for diagnosis of issues during warranty period. ~$1-200 a pop.

2) Refuse to replace yellowing S/X screens.

3) hit the credit cards of people who are supposed to have unlimited supercharging

4) not improve parts waits.

3b.1/

5) BASICALLY TURN OFF THE PHONE LINES and either make people try to chat online or go through email. These people are buying in some cases $120k cars and it's impossible to talk to a live human on the phone. Even roadside assistance is at times useless.

3b.2/

3b.2/

There's only one reason to do this.

It's because the god-king thought that profitability may be possible.

I have no idea if they're close.

But so much nickle and diming (when cash is relatively flush) means that the focus finally *IS* on accounting profits.

3b.3/

It's because the god-king thought that profitability may be possible.

I have no idea if they're close.

But so much nickle and diming (when cash is relatively flush) means that the focus finally *IS* on accounting profits.

3b.3/

So, whether it's destroying goodwill in a 6 year, 3-car cust. relationship, or getting an extra $15 from someone's credit card, or perhaps some more massaging of the numbers, just expect (as you likely already did) that the god-king pulled out all the stops in Q2.

$tslaq

3b.4/

$tslaq

3b.4/

i feel like twitter is gonna cut me off soon so i'm going to break up this thread once more for some closing thoughts

end of 3/getting to the end

end of 3/getting to the end

AND THE CONCLUSION (this part will be shorter) to the Elmer Terminal Q2 preview thread:

$tsla $tslaq

4.0/

$tsla $tslaq

4.0/

taking it all back to where my (not actually bullish but just not perma-bearish) thesis began, the story:

I think @elonmusk f'd up in a big way in his lil cute quarterly deliveries release.

$tsla $tslaq

4a/

I think @elonmusk f'd up in a big way in his lil cute quarterly deliveries release.

$tsla $tslaq

4a/

the god-king-genius-rocket-lander introduced a new metric into the $tsla universe that he should not have: backlog.

if any analysts are dumb enough to follow me on twitter, or smart enough have realized this on your own, PLEASE ask about this on the CC.

$tslaq

4b/

if any analysts are dumb enough to follow me on twitter, or smart enough have realized this on your own, PLEASE ask about this on the CC.

$tslaq

4b/

Why is this such a dumb thing for @elonmusk to have done?

because there's no way that the number is impressive.

If we're talking S/X/3 orders, (imo) the number is probably like what, 10 or 15k absolute max? cool, 1 month of orders bro.

If that number gets stated, LOL.

4c/

because there's no way that the number is impressive.

If we're talking S/X/3 orders, (imo) the number is probably like what, 10 or 15k absolute max? cool, 1 month of orders bro.

If that number gets stated, LOL.

4c/

If instead, when asked about it, the god-king says something absurd like 50k or 75k or w/e, and it includes Y/Semi/Solar Roof/website merch store/etc, he'll get laughed at (if anyone cares to drill down).

So, in the immaculate Q pt 2, that's one big mistake to harm story.

4d/

So, in the immaculate Q pt 2, that's one big mistake to harm story.

4d/

POINT 5:

Tesla has always been a contrarian's play.

Who were the bulls who *REALLY* made money?

The ones who bet on a balding @elonmusk talkin crazy stuff about EVs taking over the world in 2012. he looked destined to fail but (kinda) came through.

5a/

Tesla has always been a contrarian's play.

Who were the bulls who *REALLY* made money?

The ones who bet on a balding @elonmusk talkin crazy stuff about EVs taking over the world in 2012. he looked destined to fail but (kinda) came through.

5a/

Who were the bears who *REALLY* made money?

Those who shorted 1) after @elonmusk committed the most egregious securities fraud in history and 2) after the magic Q3 deliveries print.

So what does that mean for today?

5b/

Those who shorted 1) after @elonmusk committed the most egregious securities fraud in history and 2) after the magic Q3 deliveries print.

So what does that mean for today?

5b/

Going into the q2 print,

Analysts are largely still negative.

$tslaq is highly negative.

( $tsla bulls of course still are extremely rose-glassed for both near-term results and The Story).

But if we/analysts are expecting the worst, that means there's upside potential.

5c/

Analysts are largely still negative.

$tslaq is highly negative.

( $tsla bulls of course still are extremely rose-glassed for both near-term results and The Story).

But if we/analysts are expecting the worst, that means there's upside potential.

5c/

ALRIGHT, FINALLY THE FINAL SUMMARY.

POINT 0: This is a thought exercise of what could go right for god-king.

Point 1: ASPs may be better than $tslaq expects.

Point 2: Efficiencies from higher volume.

Point 3: other cost cuts signal desperate profit drive.

(continued)

FIN 1/3

POINT 0: This is a thought exercise of what could go right for god-king.

Point 1: ASPs may be better than $tslaq expects.

Point 2: Efficiencies from higher volume.

Point 3: other cost cuts signal desperate profit drive.

(continued)

FIN 1/3

Point 4: just me shiddin on Elon a lil

Point 5: the overall bearishness of the $tsla/ $tslaq environment right now worries me a bit and is really the motivating factor for me to throw this bullish spaghetti at the wall.

FIN 2/3

Point 5: the overall bearishness of the $tsla/ $tslaq environment right now worries me a bit and is really the motivating factor for me to throw this bullish spaghetti at the wall.

FIN 2/3

as noted earlier, please do not question my intentions - I do not wish success upon the taxpayer-fund-sucking, false-promise-making, overvalued-at-any-price brainchild of the god-king. But from career experience & normie obs, I just wanted to say some things.

$tsla $tslaq

DUN

$tsla $tslaq

DUN

this should have said that those fixed cost **pieces** decline by 15%, not the entire cost of the car. oopsies.

75m/q*