,

46 tweets,

11 min read

Read on Twitter

@CentralBankJA is starting their “Conversation On Improving Access To Finance For MSMEs”

#Jamaica #financialinclusion

#Jamaica #financialinclusion

This is the handout for attendees and it has some sobering statistics about #Jamaica but it also shows the opportunity for the unbanked and underbanked

Reliance on cash remains high

- 65% of wage earners receive their wages in cash

- 23% of account holders do not make any deposits of withdrawals into their accounts

- 65% of wage earners receive their wages in cash

- 23% of account holders do not make any deposits of withdrawals into their accounts

The new Governor of the Bank of Jamaica @CentralBankJA Tichard Baylee, officially opens the event.

He asks presenters to be brief and will not call names but indicates that whoever is laughing knows who is being spoken about (Hint: Milverton Reynolds, Head of the @DBJamaica )

He asks presenters to be brief and will not call names but indicates that whoever is laughing knows who is being spoken about (Hint: Milverton Reynolds, Head of the @DBJamaica )

Speaking about the BOJ policy rate, “For this year alone we have dropped that rate by 125 basis points” and that is a signal for financial institutions to lower their rates but the small and medium-sized enterprises have not been seeing the benefits fast enough - Byles

Byles says that the Jamaica Bankers Association has been very supportive of financial inclusion.

The IMF has also been very supportive and encouraging of the efforts - Byles

The IMF has also been very supportive and encouraging of the efforts - Byles

Dr. Uma Ramakrishnan, the Mission Chief for Jamaica at The IMF has been to Jamaica 31 times in the last 4 years!

Byles says that no one has been to Jamaica more often than her.

She has a favourite jerk spot too.

Byles says that no one has been to Jamaica more often than her.

She has a favourite jerk spot too.

Other challenges:

Households lack suitable and accessible savings, affordable insurance and retirement products - Only 30% of Jamaicans save through a regulated financial institution 😳

#financialinclusion

Households lack suitable and accessible savings, affordable insurance and retirement products - Only 30% of Jamaicans save through a regulated financial institution 😳

#financialinclusion

“The excess demand for SME credit in Jamaica is about US$2 billion...the current supply is about US$415 million” - Dr. Uma Ramakrishnan

MASSIVE gap that needs to be filled

MASSIVE gap that needs to be filled

“By regional standards, Jamaica’s access to finance numbers are behind the region” and globally - Some 18%

If one where to close this gap...if that were to be met...the Credit To GDP ratio would increase by about 13% and that is without including the Informal Sector.”

Including the Informal Sector would add another 7%

Including the Informal Sector would add another 7%

Closing the gap and bringing more people in the formal economy would add 0.5% GDP growth...in a country with 1% growth.

That’s significant.

Dr. Uma adds that bringing Crime down to global averages would add another 0.5%, That’s how big financial inclusion is

That’s significant.

Dr. Uma adds that bringing Crime down to global averages would add another 0.5%, That’s how big financial inclusion is

She is from India so she brings up examples from India because she believes that they are very similar in terms of access to credit issues.

Instead of credit scores, etc, India lenders have shifted to look at a wider range of items, not even just transaction history.

Instead of credit scores, etc, India lenders have shifted to look at a wider range of items, not even just transaction history.

Big part of India’s financial inclusion is the identification card introduced, similar to Jamaica’s NIDS, that has everything on it and makes it easy for Indians to transact online and access credit.

Says it’s food for thought.

Says it’s food for thought.

Monique Gibbs, Chief Technical Director, Ministry of Industry, Commerce, Agriculture and Fisheries (MICAF) keeps it super brief!

Highlights working with SMEs on things like digital marketing and using technology to grow

Highlights working with SMEs on things like digital marketing and using technology to grow

Jerome Smalling, President of Jamaica Bankers Association speaks about supporting the MSME push but highlights the importance of financial literacy.

He says that too many SMEs are not properly financially literate. Also highlights recordkeeping and being tax compliant

He says that too many SMEs are not properly financially literate. Also highlights recordkeeping and being tax compliant

They want to break it down to very simple language.

Majority of PR Budget is around financial literacy for SMEs.

Working to break the financial language right down. The people are not economic and finance degree holders so bankers must bridge the gap with language.

Majority of PR Budget is around financial literacy for SMEs.

Working to break the financial language right down. The people are not economic and finance degree holders so bankers must bridge the gap with language.

Keith Duncan, CEO of @JMMBGROUP among other things begins to speak.

Acknowledges Dr. Uma and her team for their work over the last 4 years.

Says it’s been “totally consultative” and meeting with all stakeholders across the society.

Very “data driven”

Acknowledges Dr. Uma and her team for their work over the last 4 years.

Says it’s been “totally consultative” and meeting with all stakeholders across the society.

Very “data driven”

Duncan is representing the @thePSOJ and points out that members have said to bankers that they will lend money to employees to buy cars but won’t lend to the business to grow.

The bankers said that the businesses weren’t providing the data to adjudicate creditworthiness.

The bankers said that the businesses weren’t providing the data to adjudicate creditworthiness.

Duncan says that you can’t lend to an SME in the same way that you lend to a large corporate.

For decades, the Govt. was crowding out private borrowers from the market and banks just focused on lending to Govt and large corporates.

Now the changes must take place and its slow because “they weren’t prepared” for lending to SMEs.

Now the changes must take place and its slow because “they weren’t prepared” for lending to SMEs.

Jamaica has had many reforms since 2010 to help, including credit bureau act and so forth.

There has not been takeup but that is where the opportunity is in Jamaica.

There has not been takeup but that is where the opportunity is in Jamaica.

Duncan lists 10 thins that need to happen to see increased support for SMEs to be able to access to financing, much of it on the banker side but includes training for the SMEs.

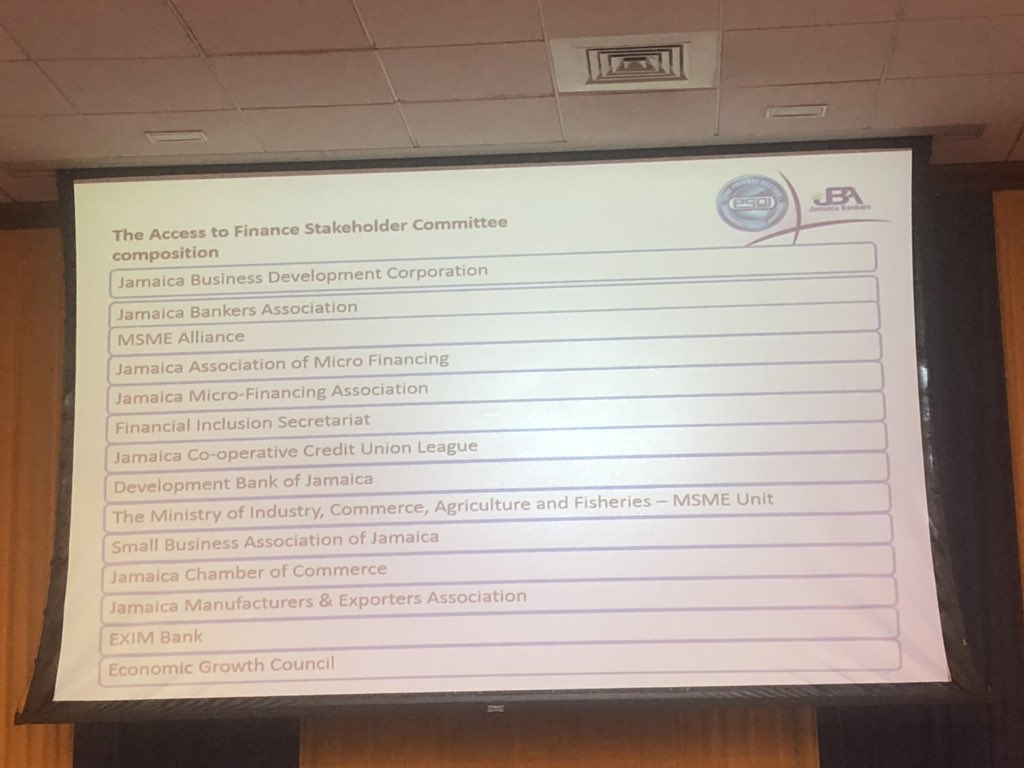

This is the Access to Finance Stakeholder Committee composition for #Jamaica

“We all came together and said that we want to shift this”

“We all came together and said that we want to shift this”

A workshop was conducted in July of this year with bankers, SMEs, Business Development Orgs and special guests.

They did surveys to get feedback and suggestions.

They did surveys to get feedback and suggestions.

Key is “designed to accommodate the cultural and educational realities of where we live and who is being targeted”

This is for Jamaica

This is for Jamaica

They have not updated on the progress since July 3rd and so Jamaicans, as usual, are quick to say something is a waste of time.

The Work Streams that they are focused on...

Simplifying and standardising firms and requirements will go a LONG way to help

The financial institutions need to “bank the SMEs profitably”

Banking a $500M loan for a large corporate can have a smaller spread and still be profitable.

Banking a $2M loan for an SME requires efficiency in order to be profitable. The banks need to make things scalable for smaller loans - Duncan

Banking a $2M loan for an SME requires efficiency in order to be profitable. The banks need to make things scalable for smaller loans - Duncan

They are also designing a “process to embed BOJ Guidance Notes faster into ecosystem” because “when you get a 250 page document and everyone reads it differently” then they need to know what to do - Duncan

The workstreams kick off next week with all the bankers that have signed up.

Separate workshops for Credit Unions and MFIs since those are more micro loans and slightly different.

Separate workshops for Credit Unions and MFIs since those are more micro loans and slightly different.

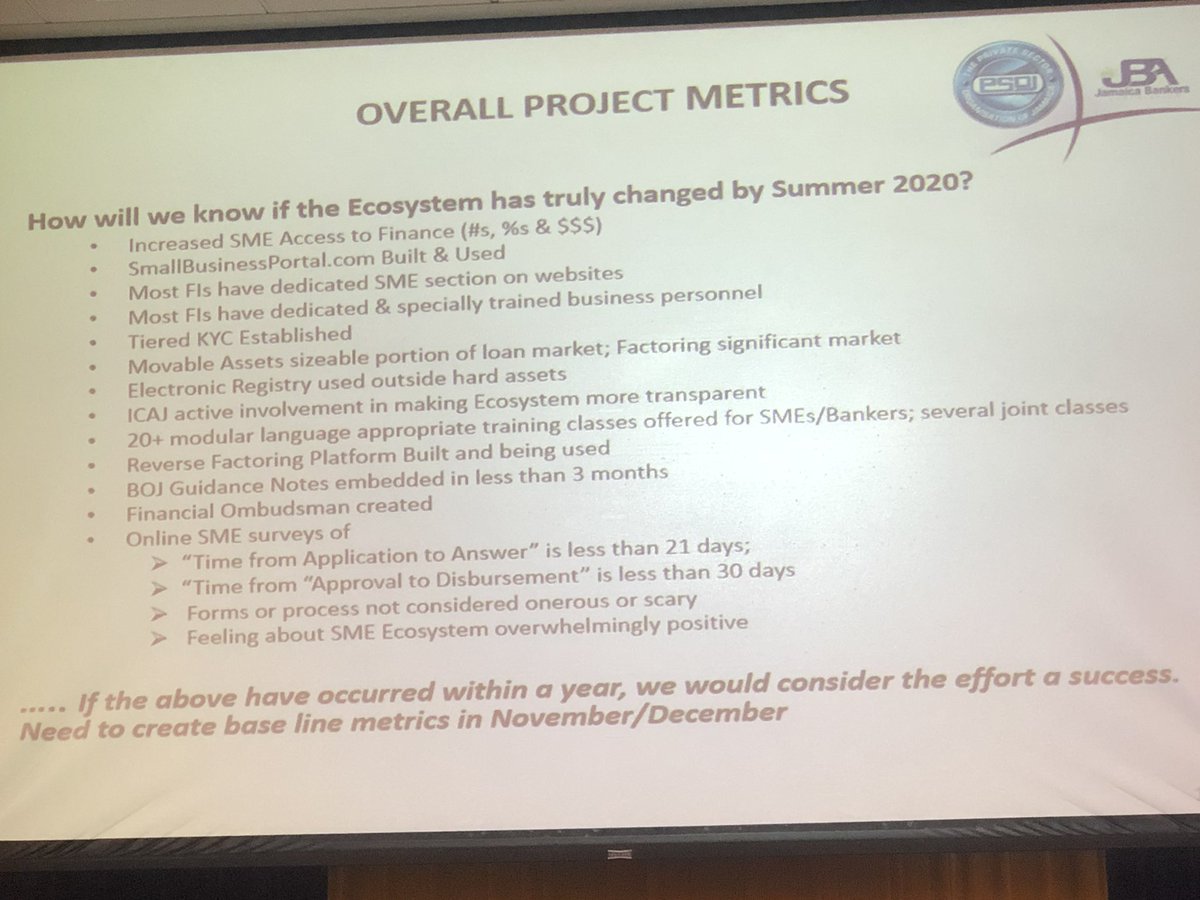

Overall Project Metrics

This is how they will be judging success of the first phase by Summer 2020

#financialinclusion #Jamaica

This is how they will be judging success of the first phase by Summer 2020

#financialinclusion #Jamaica

They are trying to get time from approval to disbursement to less than 30 days by Summer 2020

Milverton Reynolds, Managing Director of the @DBJamaica starts his presentation and is focusing on the re-introduction of a product next month that “we believe will have a significant impact on SMEs accessing financing”

Back in 2010, they put in place a Credit Enhancement Facility.

A fund was setup with J$250 million with maximum guarantees of J$15 million or 50% of the loan. Smaller loans could get 80% guarantee.

J$3.3 billion in guarantees to date and fund grown to over J$430 million

A fund was setup with J$250 million with maximum guarantees of J$15 million or 50% of the loan. Smaller loans could get 80% guarantee.

J$3.3 billion in guarantees to date and fund grown to over J$430 million

@DBJamaica got a World Bank consultant to help figure out how could they have a greater impact.

Leverage in other jurisdictions were 10 times for similar funds but Jamaica was significantly lower.

They now have a new and improved CEF that has been approved starting October

Leverage in other jurisdictions were 10 times for similar funds but Jamaica was significantly lower.

They now have a new and improved CEF that has been approved starting October

Maximum size doubles to J$30 million and 80% guarantee.

Smaller loans will benefit from 90% guarantee.

J$3.4 billion additional added to fund and leverage now 6 times so will be able to provide guanratees of up to J$25 billion for SME loans.

Well done @DBJamaica

Smaller loans will benefit from 90% guarantee.

J$3.4 billion additional added to fund and leverage now 6 times so will be able to provide guanratees of up to J$25 billion for SME loans.

Well done @DBJamaica

Introducing an electronic platform so SMEs no longer need to apply via paper forms.

Pressure in place and launches next month.

Currently, Approved Financial Institutions must apply for guarantees for loans individually.

Making changes...

Pressure in place and launches next month.

Currently, Approved Financial Institutions must apply for guarantees for loans individually.

Making changes...

Reynolds says that an example is JMMB applying for J$1 billion of guarantees and then be able to go on the system and apply for the guarantee of a specific loan and have it approved from their bulk approval.

Q&A time...

Allowed 2 questions and 2 follow-up questions

Allowed 2 questions and 2 follow-up questions

First question focuses on the psychosocial aspects of educating people in vulnerable communities.

Duncan says that this is focused on Small and Medium, not Micro, but they “need to meet the client where they are”

Duncan says that this is focused on Small and Medium, not Micro, but they “need to meet the client where they are”

SMEs also need to take some responsibility as well because it SME financing is not a handout - Duncan

I asked my 2 questions about mobile banking and asking our new BOJ Governor to work on making launching these simpler as well as asking the JBA to spend real money on R&D including AI/ML to help with credit scoring and risk models