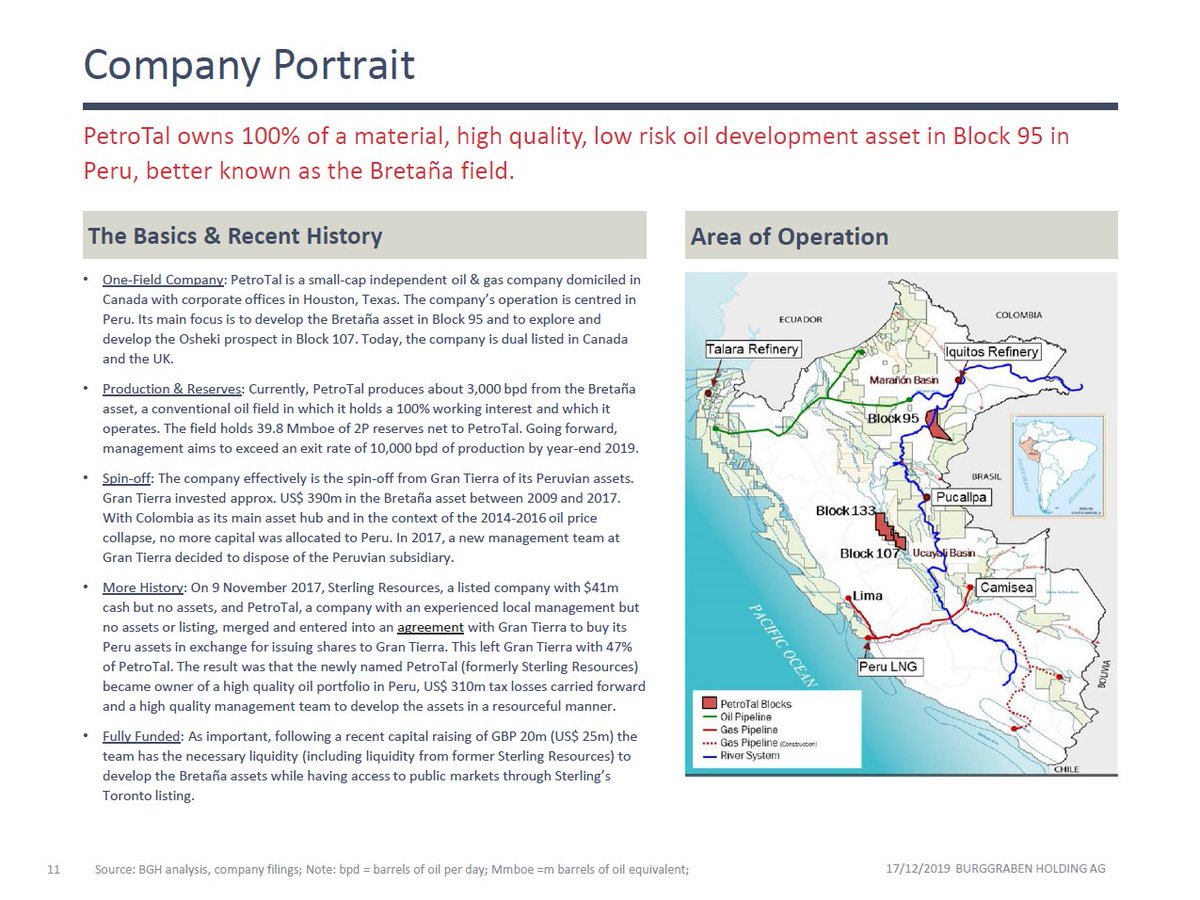

Spin Off: In 2017, Sterling, a listed company with $41m cash but no assets, and PetroTal, a company with a credible mgmt but no assets or listing, merged and entered into a agreement with Gran Tierra to buy its Peruvian assets in exchange for issuing shares to Gran Tierra. #GTE

Production: PetroTal produces 9,000 medium-heavy bpd from the Bretaña, a conventional sandstone reservoir in which it holds 100% working interest and which it operates. The field holds 39.8 Mmbbl of Proved and Probable Reserves (2P) net to PetroTal.

Unit Cost: Fully developed, Bretaña will produce at lifting cost of US$10/bbl (US$ 12/bbl incl. G&A). Over the life of the field, we forecast Bretaña to generate US$28/barrel of pre-tax free cash flow at a Brent price deck of $65/barrel.

Sunk Cost: Gran Tierra invested $390m into Bretaña’s development. This is important for an investor: Firstly, PetroTal became owner of a quality oil asset that was geologically de-risked. Secondly, it provided PetroTal with a tax asset of US$ 310m as at 31 December 2018.

Fully Funded: Due to the merger with Sterling Resources and following a capital raise of GBP 20m (US$ 25m) in May 2019, PetroTal has the necessary funding to develop the Bretaña asset. As at June 2019, the company has zero debt and a pro-forma liquidity US$ 58m.

Reserves: A geologist’s way to estimate how much oil a field may yield is to assume a recovery factor on the fields Original Oil in Place (OOIP). Bretaña’s 2P reserve assumption is for 330 Mmbbl OOIP and a recovery factor of 12% for Netherland, Sewell & Co.

Recovery Factor: Based on in-country analogue fields, the 12% recovery factor used by the CPR seems conservative. The selected fields had a total of 2.5 billion of Original Oil in Place (OOIP) and produced 665 Mmbbl crude oil for a weighted average recovery factor of 27%.

More OOIP? Data from 2 HZ completed wells suggest IP Rates of >6,000 barrels per day & 13% more net pay - a measure of the economically producible hydrocarbon thickness of a reservoir. On that basis, Bretaña may well have 45 Mmbbl more OOIP or a total of 380 Mmbbl.

Reserve Upside: Combining more OOIP & higher RF, Bretaña may well have 91 MMbbl reserves or 2x more oil to be sold! Early days, but paying attention to data & applying common sense does help buying low & ahead of the crowd, especially if base case outcome is just fine, too!

Valuation: Our Core-NAV of CAD0.9/share suggests 113% upside from today’s price of CAD 0.43/share at Brent of $65. Modelling 24% RF on 380 Mmbbl OOIP will add CAD 1.8/share to our Core-NAV for a total upside of 4.3x today’s share price. Mind you though to do your own homework.

Peers: PetroTal certainly screens cheap on a relative basis and when compared with its LatAm peers with similar country risk and netbacks.

Here is the higher recovery factor NAV table...

Risk: Upside has risk. In our view far less though than buying fashionable “disruptor”. At PetroTal, risks are mundane. They mainly revolve around execution - not reservoir - and can be addressed every single day by a competent management team.

Due Diligence: we visited all relevant authorities, the team in Lima, the field in the Amazonian & met with board members. We studied countless country, asset and research reports & spoke with high calibre industry analysts. The synthesis of our work is outlined in this paper.

Water Coning: For instance, understand that a high water cut over time will be your "friend" in Peru (which is not the case for conventional fields in the North Sea for instance). Here some info on how to manage water coning...

Transport: Or some information on transport and barging capacity, info you will not find easily anywhere else...

Here some info on the status quo of the national pipeline which remains a risk factor for a seamless execution...

While other risks are addressed by the most competent team preemtively, such as the risk of operational downtime due to ESP failure...

If you care to read the full 130 page document, send me a request on alexander.stahel@burggraben.ch. But again, this cannot be a shortcut for you to do your own homework. Good luck.

Sharing is caring.

Sharing is caring.

Our work is now also online on Seeking Alpha and has been selected as an Editor's Pick. Enjoy

seekingalpha.com/article/431295…

seekingalpha.com/article/431295…