THREAD: This morning, Trump's CMS Administrator, Seema Verma, posted a press release claiming that Trump Admin actions have "caused rates to drop for the first time." This is...stretching things, to put it mildly. 1/

acasignups.net/18/10/11/sigh-…

acasignups.net/18/10/11/sigh-…

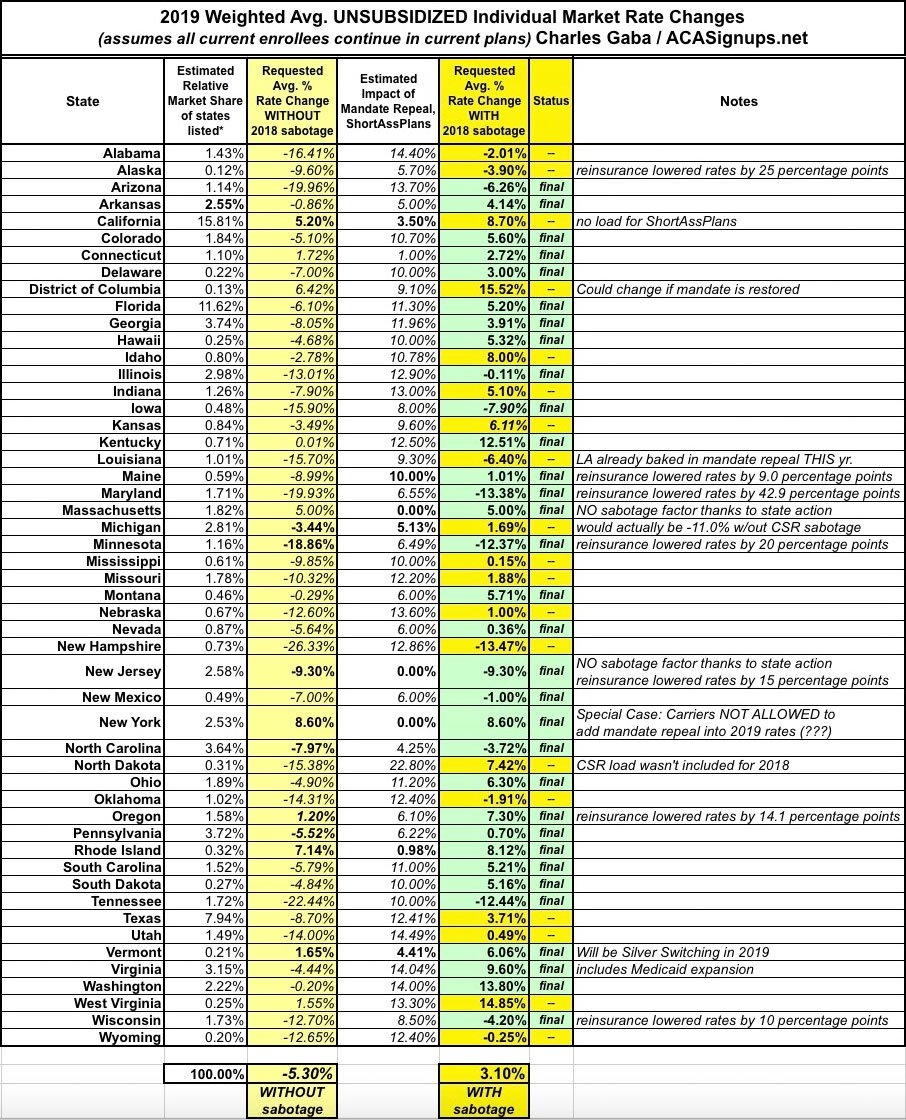

2/ FIRST, the "1.5% drop" @SeemaCMS refers to only applies to on-exchange plans, only includes 39 states, and only applies to the benchmark plans. When you include all 50 states, all plans at all metal levels and off-exchange enrollees, it's +3.1%.

acasignups.net/rate-hikes/2019

acasignups.net/rate-hikes/2019

3/ SECOND, it's true that even +3.1% is still a lot smaller than prior years...which is why you have to look at WHY premiums increased so much for 2018 LAST year. About 60% of that ~27% increase was due SPECIFICALLY to Trump Admin actions: CSR cut-off + other assorted factors:

4/ (the actual average ended up being around 27% instead of the 29.5% shown in that pie chart, which was based on carrier estimates and other data at the time, but it was still pretty close to the mark.)

5/ In ADDITION to Trump cutting off CSR reimbursement payments (which caused 2018 premiums to ⬆️ around 14 points), he also slashed the marketing budget for HCgov by 90%, slashed the ACA navigator/assistance budget by 40%, ordered the IRS not to enforce the individual mandate...

7/ ...resulted in the carriers jacking up their rates even MORE to cover their asses in a worst-case scenario. In the end, I estimate around 17 points of the 27% avg. rate increase was SPECIFICALLY due to 2017 Trump/GOP actions. That's around $80/month per unsubsidized enrollee.

8/ Put another way, while *subsidized* enrollees actually ended up doing BETTER this year as a result of all the insanity, *unsubsidized* enrollees are being hit with an additional $950 in premium expenses this year due to #ACASabotage...APIECE.

9/ That's 2018. What about 2019? Well, avg. rates are only increasing around 3.1% on avg. next year (about $19/mo, or $228 for the year) *as compared to this year*...but they WOULD be DROPPING (or dropping more than they are, in some states) if not for ADDITIONAL #ACASabotage:

10/ THIS year's stunts include the GOP's repeal of the #ACA mandate penalty (perhaps 7-8 points) as well as Trump's executive order to flood the market with #ShortAssPlans (aka #JunkPlans) (perhaps 1-2 points). Combined, that's an additional 8-9% rate hike on average.

11/ You're likely asking how avg. premiums can only be increasing 3% if #ACASabotage can be causing an 8% increase? Part of the answer is, ironically, the #ACA itself. Remember, under the ACA, carriers have to spend at least 80% of their premium revenue on actual medical claims.

12/ In other words, if a carrier ends up making more than a 20% gross margin, they have to PAY THE BALANCE BACK in the form of rebates the following year. This is the #ACA's Medical Loss Ratio rule (MLR), and several billion $ have already been refunded over the years.

13/ The whole idea of the 80/20 MLR is to prevent price gouging--and in this case, it's working perfectly. While MOST of the damage projected by last year's insanity proved to be accurate, the #ACA resisted Trump's efforts pretty well, with "only" a 5% enrollment drop, etc.

14/ As a result, most of the carriers turned out to have *overestimated* how ugly 2018 would be...which means that, due to the ACA's MLR rule (combined w/state-level regulatory decisions), many carriers are either DROPPING 2019 prices or, at worst, only raising them nominally.

15/ HOWEVER, it's important to understand that those price drops (or minor increases) are SEPARATE from other factors, which are ALSO baked in. Some carriers *lowered* rates by, 15% to comply w/MLR...but then *raised* them by 8-9% to account for #MandateRepeal + #ShortAssPlans.

16/ As a result, a carrier might end up *lowering* their 2019 premiums by 6% instead of 15%...which means that unsubsidized enrollees are *still* paying hundreds of dollars more due to #ACASabotage even if the premium itself is lower year over year.

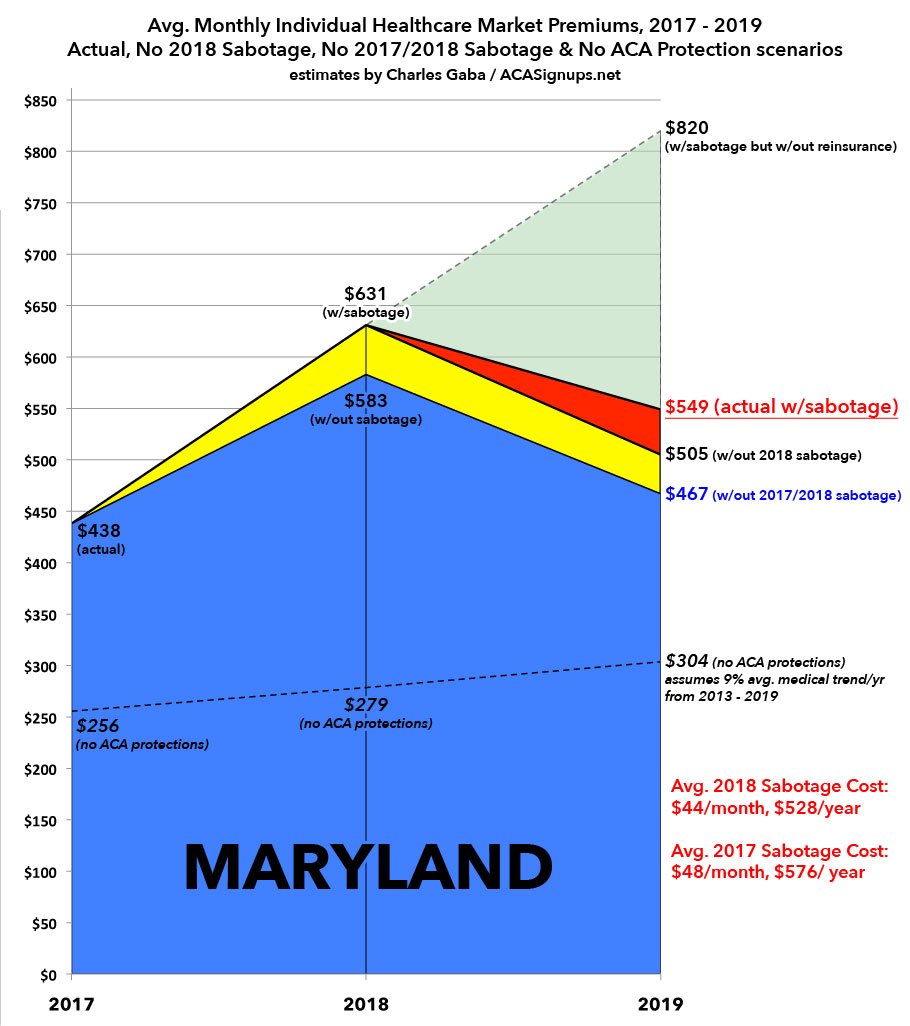

17/ HERE'S WHAT THAT LOOKS LIKE IN PRACTICE:

BLUE: Avg. unsubsidized premiums in a no-sabotage world.

YELLOW: Avg. premiums with LAST year's #ACASabotage (CSR cut-off/etc)

RED: Avg. premiums with THIS year's sabotage (mandate repeal/#ShortAssPlans):

acasignups.net/18/10/11/sigh-…

BLUE: Avg. unsubsidized premiums in a no-sabotage world.

YELLOW: Avg. premiums with LAST year's #ACASabotage (CSR cut-off/etc)

RED: Avg. premiums with THIS year's sabotage (mandate repeal/#ShortAssPlans):

acasignups.net/18/10/11/sigh-…

18/ This chart varies widely by state, of course; in some states the yellow & red sections are huge, in others they're small. In a few states (MA & NJ) there's no red section at all, because they have their own mandate & don't allow #ShortAssPlans.

19/ OK, but what about states like Wisconsin and Maryland, which have implemented robust reinsurance programs? Well, reinsurance is a fantastic idea which I (and other HC wonks) have been pushing hard for awhile now. HOWEVER, again, reinsurance is SEPARATE from #ACASabotage.

20/ Here's the most robust reinsurance program to be launched this year, in Maryland...they were looking at a 30% rate hike next year, but thanks to their reinsurance program being especially generous, unsubsidized rates are instead DROPPING about 13%.:

acasignups.net/18/09/21/updat…

acasignups.net/18/09/21/updat…

21/ Also notice that neither last year's nor this year's #ACASabotage ended up having too much impact on Maryland (relatively speaking). Rates went up a lot this year, but only a small chunk of it was due to CSR cut-off/etc. As for 2019...

22/ Maryland wisely reinstated restrictions on #ShortAssPlans, which means mandate repeal is the only significant factor there next year. Even so, that's still over $500 per unsubsidized enrollee, plus another $570 or so from last year...over $1,000 apiece. Ouch.

23/ The point is that while reinsurance is a great thing, it could be done IN ADDITION to reinstating the mandate, cracking down on #ShortAssPlans and so forth for *additional* savings.

24/ Oh, one more thing: While Trumpster Seema Verma did sign off on these reinsurance programs...the framework for doing so is ALREADY PART OF THE #ACA ITSELF. Which means that even the few *positive* things she's doing are simply *using Obamacare to improve Obamacare*. /END

Oh, one more thing…this week happens to be the 5th Anniversary of ACASignups.net. If you’d like to help keep it going for *another* 5 years, please consider supporting it here, thank you!