,

23 tweets,

11 min read

Read on Twitter

JMP in print at the Journal of Finance!

*takes deep breath*

Let me tell you about my job market paper

*takes deep breath*

Let me tell you about my job market paper

We think about the financial crisis as a sequence of "runs." There was a run on Northern Rock, and in wholesale markets like repo.

But there was also a run by the *bank * on the borrower in the adjustable-rate mortgage market.

Wait, how can a bank run on the borrower?

But there was also a run by the *bank * on the borrower in the adjustable-rate mortgage market.

Wait, how can a bank run on the borrower?

First, some background on these contracts.

Pre-crisis, borrowers would commonly get adjustable-rate mortgage (ARM) contracts which had fixed initial periods of 2, 3, or 5 years; after which they "reset" so payments are benchmarked against the floating market rate.

Pre-crisis, borrowers would commonly get adjustable-rate mortgage (ARM) contracts which had fixed initial periods of 2, 3, or 5 years; after which they "reset" so payments are benchmarked against the floating market rate.

In the boom, people found it unaffordable to make payments on your standard 30-year fixed rate mortgage.

But they were able to make those introductory teaser payments. Eventually, even that got expensive and they had to get Option ARMs (more on this soon).

But they were able to make those introductory teaser payments. Eventually, even that got expensive and they had to get Option ARMs (more on this soon).

So you have your two or three year ARM, and when reset comes you refinance into another similar product

Instead of a 30-year mortgage, it's more of a sequence of short-term borrowing from the bank, which can deny you credit when interest rates are high and house prices are low

Instead of a 30-year mortgage, it's more of a sequence of short-term borrowing from the bank, which can deny you credit when interest rates are high and house prices are low

Which is what happened. Policymakers were extremely concerned at the time that these ARM resets would trigger higher payments, defaults, and resulting cascading effects in the market; and this was a contributing factor behind lowering interest rates

Cool, but how are we going to identify any of this?

Well, were going to take advantage of the fact that there is no one "interest rate." This advertisement for a HELOC I walked pass the other day, for instance, specifies the Prime Rate.

Well, were going to take advantage of the fact that there is no one "interest rate." This advertisement for a HELOC I walked pass the other day, for instance, specifies the Prime Rate.

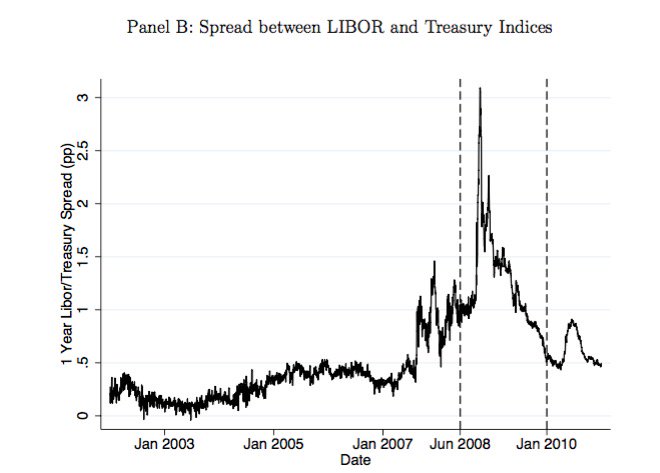

So your ARM could be tied to LIBOR or Treasury rates. Seen as basically identical before the crisis, this spread blew up during this crisis. This means that borrowers resetting at a disadvantageous time could pay $1000s more than similar borrowers resetting at the *same time*

Another pre-computer feature of ARMs is the "lookback period." To determine your payment after the reset, you "look back" 15, 30, 45 days and take the *exact* interest rate *that day* to be set for the next 6-12 months. So when interest rates move around, variation in payments

What this gives us is something very rare in finance -- cross sectional variation in interest rates! Which you generally don't have, basically by definition.

But here, otherwise identical borrowers are paying *different amounts*

But here, otherwise identical borrowers are paying *different amounts*

Okay, but what determines which of these indices you get? one might ask (and, in fact, dozens of people did).

Lookback in particular is pretty random; for LIBOR v. Treasury it was often a function of LIBOR preferences by institutional investors. We're going to control for the index type or lookback type, and use the *spread* between similar mortgages to get tight variation

Then I did an out of sample test. Did my parents, who have an ARM, know their index (no)? This is what borrowers see:

If you ask people, only 1/4 people report their index to be something that could even possibly be true. Rest are things like "CPI", "the interest rate" etc

If you ask people, only 1/4 people report their index to be something that could even possibly be true. Rest are things like "CPI", "the interest rate" etc

What's new here is that their *neighbors* also default more often if the person next door has experienced an interest rate shock. What's going on here?

When borrowers have higher exogenous payments, they default more often. That's not super surprising maybe.

When borrowers have higher exogenous payments, they default more often. That's not super surprising maybe.

Well, it's not a *direct* price effect. The default of a home triggers a foreclosure fire sale which is a ~30-50% discount. But neighboring homes drop maybe 1-3% in value.

And the *neighbors* are defaulting on just the mortgage, not other debt, in a small neighborhood around the home

Part of this is a peer effect: social norms towards debt repayments change when someone defaults in their neighborhood.

Happened where my parents live: negative equity neighbor strategically defaulted, and people talked about it

Happened where my parents live: negative equity neighbor strategically defaulted, and people talked about it

Part of it is the refinancing channel. Refinancing *plummets* in areas that have more foreclosures.

Why? I think because appraisals often use the neighboring foreclosed sale as a comp when comparing prices. So new credit plummets.

Why? I think because appraisals often use the neighboring foreclosed sale as a comp when comparing prices. So new credit plummets.

To recap:

- Subprime borrowing was rolled-over series of ARMs

- Credit shuts down, triggering a "run" forcing borrower to pay higher rate

- Borrower default -> drop in prices amplified through foreclosures being in the comp set

- Neighbors default

- World looks like this:

- Subprime borrowing was rolled-over series of ARMs

- Credit shuts down, triggering a "run" forcing borrower to pay higher rate

- Borrower default -> drop in prices amplified through foreclosures being in the comp set

- Neighbors default

- World looks like this:

With @ChrisHansman we've looked at the LIBOR-Treasury spread impact on Option ARMs. Here, there is a cool experiment because interest shocks accrue directly to the *balance* allowing us to estimate moral hazard (strategic default) and adverse selection

chansman.github.io/GuptaHansman.p…

chansman.github.io/GuptaHansman.p…

And I'm also super thrilled other people have taken this up in other ways. Christos Makridis and Michael Ohlrogge have a paper on the effect of ARM shocks on local employment, lending, and uncertainty

And @SashaIndarte has a great JMP in which she uses LIBOR-Treasury shocks to separate cash flow shocks from strategic factors in bankruptcy filing, in conjunction with a state border discontinuity in bankruptcy exemption levels

Thanks to everyone for supporting me along the way, and to you for reading.

And now, I get to never ever talk about this paper ever again.

And now, I get to never ever talk about this paper ever again.