,

12 tweets,

4 min read

Read on Twitter

The U.S. faces one fundamental problem in a currency war with China: right now, the market wants to push the yuan weaker, and the more the U.S. escalates, the more the market will test the PBOC ...

ft.com/content/9d24c1…

ft.com/content/9d24c1…

a bit more color ...

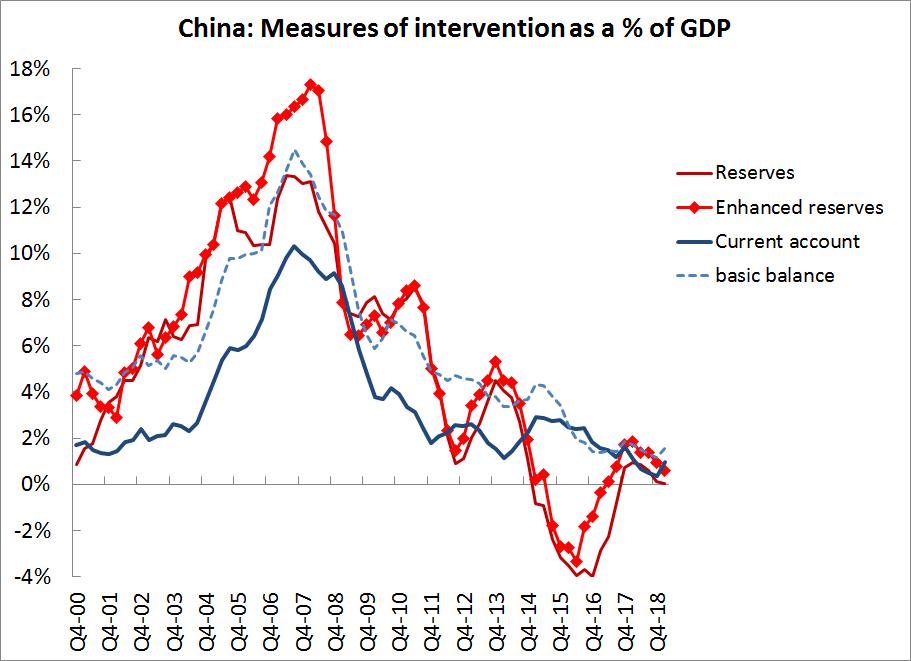

China clearly met the current criteria for manipulation from 2003 to 2013 ...

but it hasn't been consistently intervening to block appreciation over the last five years.

China clearly met the current criteria for manipulation from 2003 to 2013 ...

but it hasn't been consistently intervening to block appreciation over the last five years.

The Treasury though is operating under a different theory of the case, namely that China should be as aggressive in resisting pressure on its currency to depreciate (now) as it was in resisting pressure for appreciation during the China shock years.

home.treasury.gov/news/press-rel…

home.treasury.gov/news/press-rel…

The Treasury's statement makes it clear that it is working under the definition of manipulation provided by the 1988 omnibus trade act, not the more recent Bennet amendment (China only meets one of the three Bennet criteria).

(background in link)

cfr.org/blog/china-man…

(background in link)

cfr.org/blog/china-man…

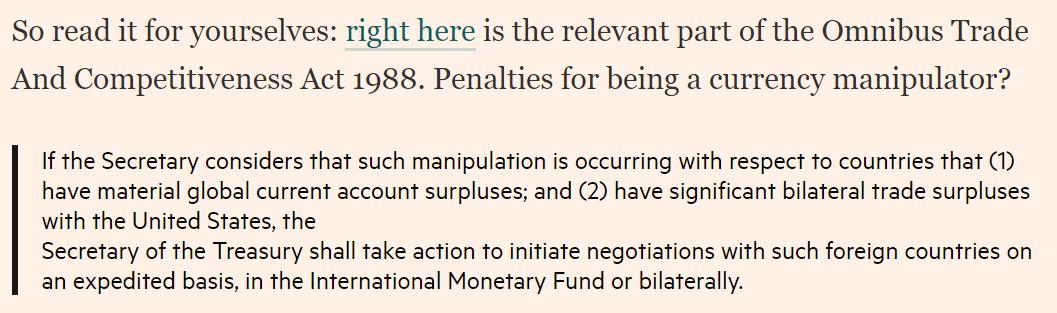

Here is the key provision of the 1988 act. My guess is that the Treasury will rely on the

"or gaining unfair competitive advantage in international trade" provision

"or gaining unfair competitive advantage in international trade" provision

By statute the Treasury has to consult with the IMF. But it is unlikely the IMF will provide the Treasury much (if any) cover. It gave China a clean bill of health in its recent external sector report.

imf.org/~/media/Files/…

imf.org/~/media/Files/…

Here is the catch: The 1988 Omnibus Trade and Competitiveness Act defines the crime of manipulation generously, but it doesn't actually provide a meaningful sanction for manipulation

see Alan Beattie way back when

ft.com/content/9dd058…

see Alan Beattie way back when

ft.com/content/9dd058…

I am sure China is deeply worried about the threat of expedited negotiations, either on a bilateral basis or through the IMF ....

But the real sanction associated with a designation of manipulation in my view has never been the threat of negotiations. It has been that the U.S. would use other legal authority available to the President to craft a real sanction, or seek legislation to provide a sanction ...

the real challenge for the Trump administration is coming up with a sanction beyond what it has already put on the table. An across the board 10% tariff (or 25% tariff) would by any reasonable definition be a major sanction, but it is hard to threaten what you are already doing

That leaves intervention through the Exchange Stabilization Fund (the Treasury's pot of money for fx intervention) -- the US would in essence threaten to buy the yuan that it thinks China should be buying right now ...

That's all for now.

There is a lot of legal detail in my 2016 blog on the legal authority available to the Treasury for a designation, and I think it has stood the test of time

cfr.org/blog/china-man…

There is a lot of legal detail in my 2016 blog on the legal authority available to the Treasury for a designation, and I think it has stood the test of time

cfr.org/blog/china-man…